Investment markets and key developments over the past week

Despite ongoing global growth fears and mixed earnings news, share markets in the US, Japan and Australia gained over the last week with a fall in the Yen helping Japanese shares and the recent RBA rate cut continuing to help Australian shares. However, European shares fell slightly and Chinese shares remained under pressure. Bond yields were little changed, the $US edged up slightly and commodity prices were mixed with oil up but metals down.

Another Greek blow up looks unlikely for this summer. Renewed Grexit fears helped set off share market turbulence around mid-last year (and mid-2010, mid-2011 and mid-2012) but the same looks unlikely this time around. With Greece agreeing various reforms on pensions, taxes and contingent spending cuts it looks likely to pass the first review of its latest aid program. European creditors are now starting to discuss debt relief based around longer maturities and lower interest rates. There is a way to go, but at this stage it looks like another Grexit scare won’t be back in the headlines this year.

Impeachment trial of Brazilian President Rousseff only the beginning. While Brazil’s Senate vote to commence an impeachment trial of Dilma Rousseff was greeted positively by the Brazilian share market, Brazil has a long way to go to get back on track. Vice-president Michel Temer who is now acting president is unlikely to change economic policy significantly, the trial will likely take months, then the outcome can be challenged and even if President Rousseff is ultimately removed it should be recognised that it won’t necessarily do anything to solve Brazil’s fundamental problem. A new election would help but that could be some time away and it’s not clear that it will result in a government focussed on undertaking the necessary economic and political reforms to get Brazil’s economy back in shape. In other words Brazil’s problems are much bigger than Rousseff – they have just been exposed by the commodity slump.

Lowering Australia’s inflation target would be madness. Back around 2007-08 when inflation had pushed above 4% (both headline and underlying) some commentators were seriously arguing that the RBA cannot fight rising global commodity prices and so should just raise its inflation target. Now were hearing that with inflation below target the RBA should just lower its target with some using the same argument about falling global commodity prices. This is nonsense. The whole point of having an inflation target is to anchor inflation expectation around the target. If it is just raised or lowered each time it looks like being seriously breached due to commodity price movements or whatever then those expectations – which workers use to demand wages gains, companies use in setting wages increases and prices and which help drive future inflation – will simply move up or down depending on which way the target is changed. This is why it took so long to get inflation back under control in the 1970s and 1980s and why Japan has struggled to end deflation over the last two decades. The RBA should simply ignore such calls.

Major global economic events and implications

US data was a little stronger with small business optimism up in April and strong readings for job openings and hiring suggesting that the labour market is strong and the slowing in payrolls seen in March may be an aberration. That said unemployment claims have edged up over the last couple of weeks, although the rise over the last week may be due to special factors as it was driven by just New York.

Eurozone industrial production fell but German factory orders rose.

Japan’s leading economic indicator rose in March, but various economic confidence indicators fell not helped by the Kumamoto earthquake and underlying wages growth remained soft.

Chinese CPI inflation was unchanged at 2.3% year on year in April, with non-food inflation remaining low at just 1.1% yoy. There was good news though with producer price deflation continuing to recede from -4.3% yoy to -3.4% yoy. This is a good sign. Meanwhile Chinese export and import growth slowed back a bit in April but the decline in underlying foreign exchange reserves continued to slow suggesting that capital outflows are continuing to slow as a degree of stability has returned to the Renminbi (albeit this partly dependent on what the $US does).

Indian economic data disappointed with weaker than expected industrial production and higher inflation.

Australian economic events and implications

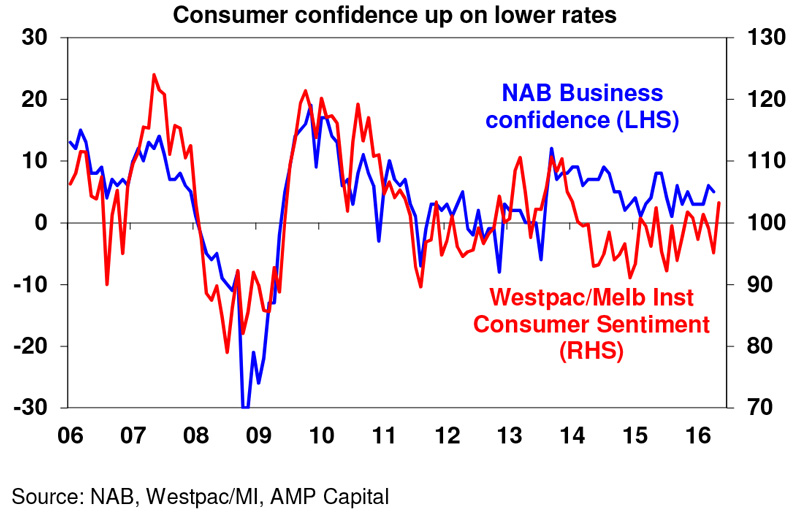

Australian data was a bit light on, but the highlight was a bounce in consumer confidence that took it above average and to its highest since January 2014 – rate cuts work at least in the short term! This doesn’t appear to have been driven by reaction to the Budget (which looks neutral relative to last year), but rather appears to reflect reaction to the RBA’s latest rate cut which is a positive sign. That said consumer sentiment is volatile month to month and remains below levels associated with strong growth.

Meanwhile Australian housing finance was a bit stronger than expected in March driven by loans going to investors to buy new properties. The broad trend is still down but there has been a bit of a bounce in investor loans. Strength here is likely to be limited though given ongoing APRA vigilance. Finally, ANZ job ads slowed a bit again in April, consistent with some moderation in employment growth after last year’s surge.

Reflecting the downside risks to inflation we are now allowing for two more rate cuts from the RBA this year taking the cash rate down to 1.25%.

What to watch over the next week?

In the US, expect to see gains in the NAHB home builders’ conditions index (Monday), housing starts and industrial production (both Tuesday) and existing home sales (Friday). Manufacturing conditions surveys for the New York and Philadelphia regions will give an early guide as to how conditions are tracking in May. While CPI inflation (Tuesday) is likely to show a solid rise reflecting the recent bounce in oil prices core CPI inflation is expected to fall back slightly from 2.2% yoy to 2.1%. The minutes from the Fed’s last meeting (Wednesday) are likely to confirm that the majority view at the Fed is cautious and dovish.

In Australia, the minutes from the RBA’s last meeting (Tuesday) will be a bit dated given the recent Statement on Monetary Policy but no doubt they will be watched for any further clues regarding the interest rate outlook. On the data front expect to see March quarter wages growth (Wednesday) remain low around 2.2% year on year and April labour market data (Thursday) to show weak jobs growth after the solid gain seen in March and a slight bounce in unemployment back to 5.8%.

Outlook for markets

Expect short term share market volatility to remain high. May always seems to be a nervous time as now everyone knows about “sell in May and go away, come back on St Leger’s Day”, global growth remains fragile and uncertainty lingers around the Fed and China. However, beyond near term volatility, we still see shares trending higher this year helped by a combination of relatively attractive valuations, further global monetary easing and continuing moderate global economic growth.

Very low bond yields point to a soft medium term return potential from them, but it’s hard to get bearish in a world of fragile growth, spare capacity and low inflation.

Commercial property and infrastructure are likely to continue benefitting from the ongoing search for yield by investors.

Capital city residential property price gains are expected to slow to around 3% this year, as the heat comes out of Sydney and Melbourne. Prices are likely to continue to fall in Perth and Darwin, but price growth is likely to pick up in Brisbane.

Cash and bank deposits are likely to provide poor returns – getting even poorer!

The ongoing delay in Fed tightening still poses short term upside risks for the $A. However, any short term rebound is likely to be limited and the longer term downtrend looks to be resuming as the interest rate differential in favour of Australia narrows as the RBA continues cutting the cash rate and the Fed eventually resumes hiking, commodity prices remain in a secular downswing and the $A undertakes its usual undershoot of fair value.

By Shane Oliver, AMP Capital