Australian investors have largely missed out on the 20-year bond rally, preferring instead to invest in cash for their liquid/defensive asset holding. However, they missed out on a major benefit of holding high quality bonds – the negative correlation they provide to equities. This particularly came to light in the GFC when equity prices collapsed and Australian investors had no fixed income exposure to offset the negative returns from equities. In addition, investors in cash/term deposits tend to be more exposed to cash rate cuts.

Weakness in the economy has seen the Reserve Bank of Australia (RBA) slash interest rates over the past few years, leading to a plunge in term deposit rates. Although this has also had the effect of dragging down bond yields and thus making bonds more expensive, we believe they are still likely to outperform cash, particularly if the cash rate keeps falling. Given the current economic environment both globally and domestically, the cash rate is likely to remain lower for longer. As a result, Australian investors may want to reassess their low exposure to fixed income.

Bond yields historically low and likely to remain so for a while

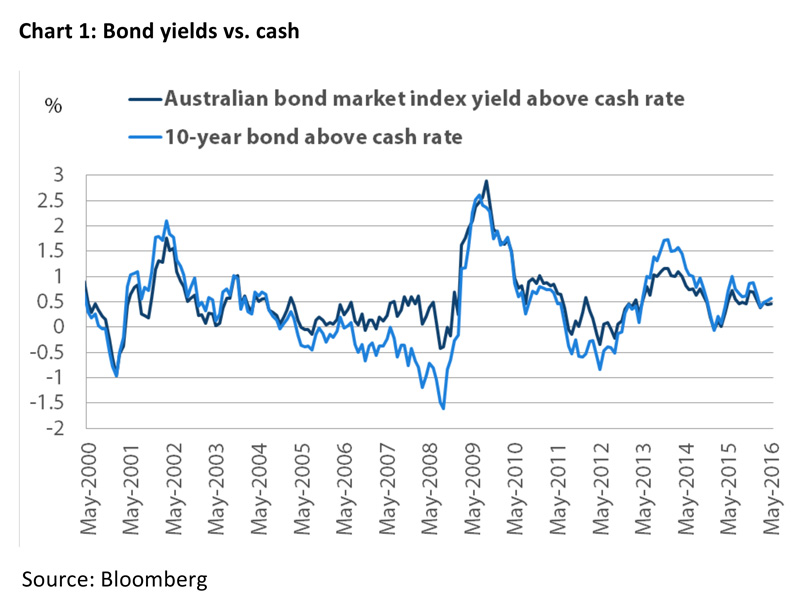

The cash rate fell to 1.75% in May, down from 2.5% in 2014. Australian bonds have followed the cash rate down and are currently sitting just above historical lows in yields. However, as chart 1 shows, despite the fall in bond yields, the Australian bond market (as measured by the Bloomberg AusBond Composite 0+ Yr Index) and the 10-year government bond are currently providing a yield of around 50 basis points (bps) above cash. This looks fair value in historical terms; in contrast, the 2015 rate cuts reduced the spread of bond yields over cash down to zero.

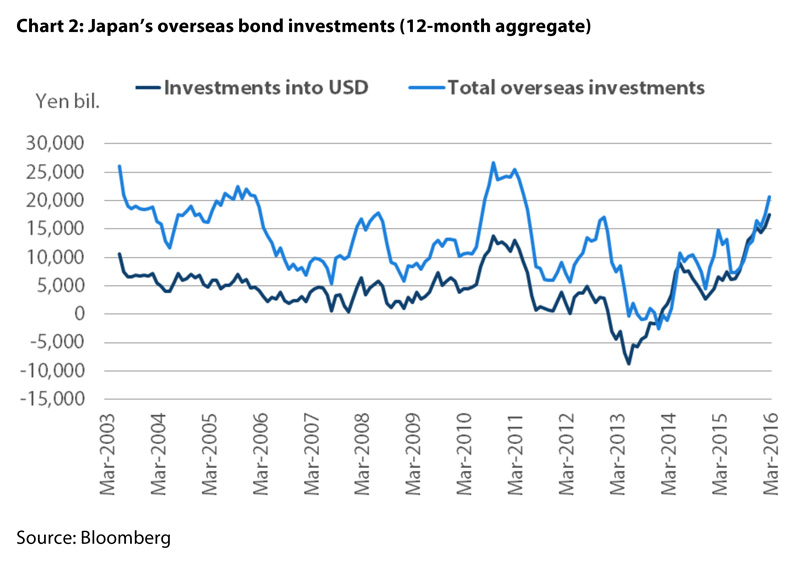

One factor that many investors have been wary of over recent years is the US Federal Reserve (Fed). Many believe that if the Fed tightens rates, as they did in December 2015, it could lead to a rise in global bond rates – and Australia would not be immune. However, negative interest rate policies and quantitative easing (QE) in Europe and Japan are driving global bond markets at the moment more than the Fed. Japanese and German savers are searching for yield in bond markets outside of their home countries and particularly in the US (see chart 2). This is keeping a lid on US and global bond rates and raises the question of whether the Fed still has the same control as it once did over the US Treasury market.

What will happen to the Australian cash rate?

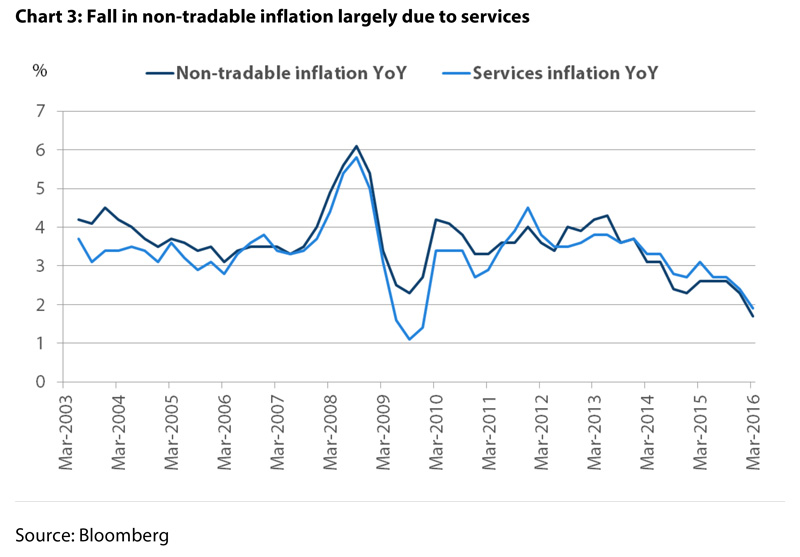

The rate cut in May was largely due to a surprise fall in inflation, particularly in the non-tradable components of the index, which reflects domestically created inflation and is not subject to the vagaries of currency movements (see chart 3). Domestic inflation is mainly driven by wages and we are seeing historically low growth rates, implying that we could see further falls in inflation from domestic sources. This was compounded by the fact that the Australian dollar had strengthened prior to the rate cut due to a speculative rebound in the iron ore price and the fact a more dovish Fed had led to a weaker US dollar.

Since the May cut, iron ore prices have fallen and the Fed’s more hawkish rhetoric has fuelled the US dollar, allowing the Australian dollar to depreciate. This may relieve some of the pressure on the RBA to cut again quickly and we expect that the bank will wait until August when they will get the next read on the inflation picture and to see if the Fed further assists a decline in the US dollar by raising rates in the interim. Even so, it is unlikely the RBA will remove its easing bias and we don’t expect the market to stop pricing in further rate cuts. With rising concerns around settlement issues on multi-unit developments and the fall in total hours worked, we believe another rate cut is likely even if the Fed tightens and/or non-tradable CPI growth stabilises.

Bonds may be expensive, but are still likely to outperform cash

Australian bond rates are currently quite low, but so is the cash rate and bonds are providing a historically fair value for investors compared with cash investments. There is a risk of another ‘Bund tantrum’, when German Bunds sold off for no apparent reason in 2015, or the US Treasury market could react negatively to the Fed if it raises rates. However, these are likely to be short-term events that could actually provide investors with a good opportunity to buy bonds at higher rates. The fact is that Australian bonds remain well priced to cash and since we believe that the official cash rate is highly likely to move lower, this provides an extra incentive to consider a fixed income allocation over a cash allocation.

By Roger Bridges, Global Rates & Currencies Strategist, Nikko AM

———