Overview

The UK referendum on European Union membership has introduced political and economic uncertainty across Europe. It is unclear what the UK relationship with Europe will be in future, and when the eventual EU Brexit deal will be concluded. But uncertain times like this are very good for active managers. Volatility creates opportunity.

Equity markets recovered surprisingly well after the vote. Further interest rate cuts are likely, as is further quantitative easing (already seen in the UK) – these are favourable for equities and other real assets. However, whilst monetary policy keeps borrowing costs low, it does not solve the problem of excessive debt, and monetary policy has failed to stimulate meaningful economic growth. We expect continuing low economic growth and, even though markets are calm at present, an increase in volatility.

It is important not to lose perspective, but to rely on the fundamental task of picking high-quality stocks. It is business as usual for our European equities team –volatility will provide us with good opportunities in both larger and smaller companies. As Winston Churchill said: “Never let a good crisis go to waste!”

Brexit

In the UK leading economic indicators dipped after Brexit, with weak recent PMI data across manufacturing and services providing the Bank of England with the evidence it needed for looser monetary policy. While the recent ‘stress test’ of European banks was not as negative as feared, it highlighted the weak state of many banks, with Italian banks in particular facing a capital shortfall.

Many other headwinds facing Europe are political: a presidential re-election in Austria, a referendum in Hungary, Brexit negotiations, US presidential elections, French presidential elections next year and German federal elections in 2017.

But it is not all bad: central banks have signalled action to support markets and we anticipate more fiscal policy stimulus. UK corporate earnings and the economy have been supported by a weaker sterling. European banks are in better shape than at the time of the global financial crisis, and in Italy Prime Minister Renzi has staked his political future on a reform referendum in October, so a market friendly recapitalisation of Italian banks is likely.

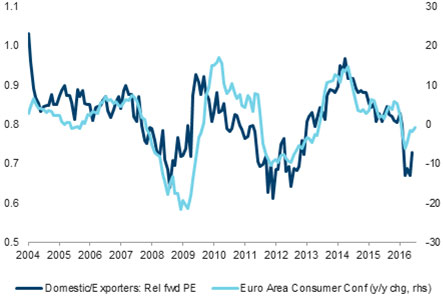

In terms of economic forecasts, we expect UK GDP growth of 1.25% in 2016 and 0.5% in 2017. A technical recession is possible in late 2016 / early 2017 as investment contracts, although this is not our core view. Inflation is forecast to rise to 2.5% in 2017 due to the weak pound. Following firm PMIs/economic data from the Euro Area in the aftermath of the referendum, we have marked up slightly our GDP forecasts to in 2016 to 1.4% from 1.1% previously. In 2017, growth of around 0.9% seems likely. The region should avoid recession even though domestically-focused Europe area stocks are effectively pricing one in (Figure 1).

Figure 1: European stocks forward price-earnings ratios and consumer confidence

Source: Barclays Research, DataStream, MSCI, as at August 2016

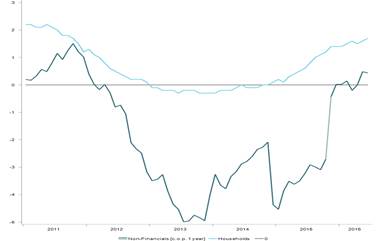

The risks to our forecasts in the UK relate to weaker consumer confidence and lower business investment. In Europe, Brexit should prompt structural reforms and more accommodative fiscal policy, but the recent economic recovery has been driven by falling unemployment, rising consumer confidence and better credit demand (see Figure 2). Domestic businesses would be hurt by any setbacks in these metrics.

Figure 2: Euro Area Loan Growth to Corporates and Households

Source: Bloomberg, Macrobond, Columbia Threadneedle Investments, as at August 2016.

Equity valuations are still reasonable, with a near 4% dividend yield: well above the yield on other equity and bond markets. Europe is cheaper than the US on a price-earnings basis and has underperformed that market.

Volatility creates opportunity

Political uncertainty, coupled with unresolved economic stresses, will probably lead to some volatility, but long-term investors know that what can feel like an emergency in the short-term may not hold much significance some years later, so a focus on good-quality stock picking makes good sense. Time in the market is more important than timing the market.

So it is business as usual for us. Our approach focuses on investment in high-quality, long-term compounders rather than economically sensitive stocks.

Smaller companies

Smaller company stocks can be more volatile than their larger peers and this has been borne out by recent market moves. Smaller companies tend to be less diversified and with smaller balance sheets, and they tend to be more domestically oriented.

These factors have all worked against smaller company valuations, as can be seen in Figure 3, below.

Figure 3: European smaller companies valuations are attractive

Source: Bloomberg, Columbia Threadneedle Investments, as at 3 Aug 2016.

However, as in any period of volatility this impact on smaller company valuations creates opportunities for us. We spend our time picking high quality, niche-oriented growth companies and the recent market gyrations give us a chance to buy unloved or unrecognised stocks with great long-term potential.

by Philip Dicken, Head of European Equities

———-