Leading global asset manager, Eaton Vance believes that numerous weak spots highlighted by the IMF reinforce the importance for investors of fundamental country analysis for emerging markets.

The manager says: The IMF’s annual meeting over the weekend took place against a backdrop of sluggish global growth, with concern about “tail risks” emanating from developed economies, largely over the uncertainty posed by elections, monetary policy and protectionism.

The meeting coincided with the semi-annual release of the IMF’s World Economic Outlook, which pegged the world’s growth for 2016 at 3.1%, and 3.4% for 2017 – downticks of 0.1% for both figures from April.

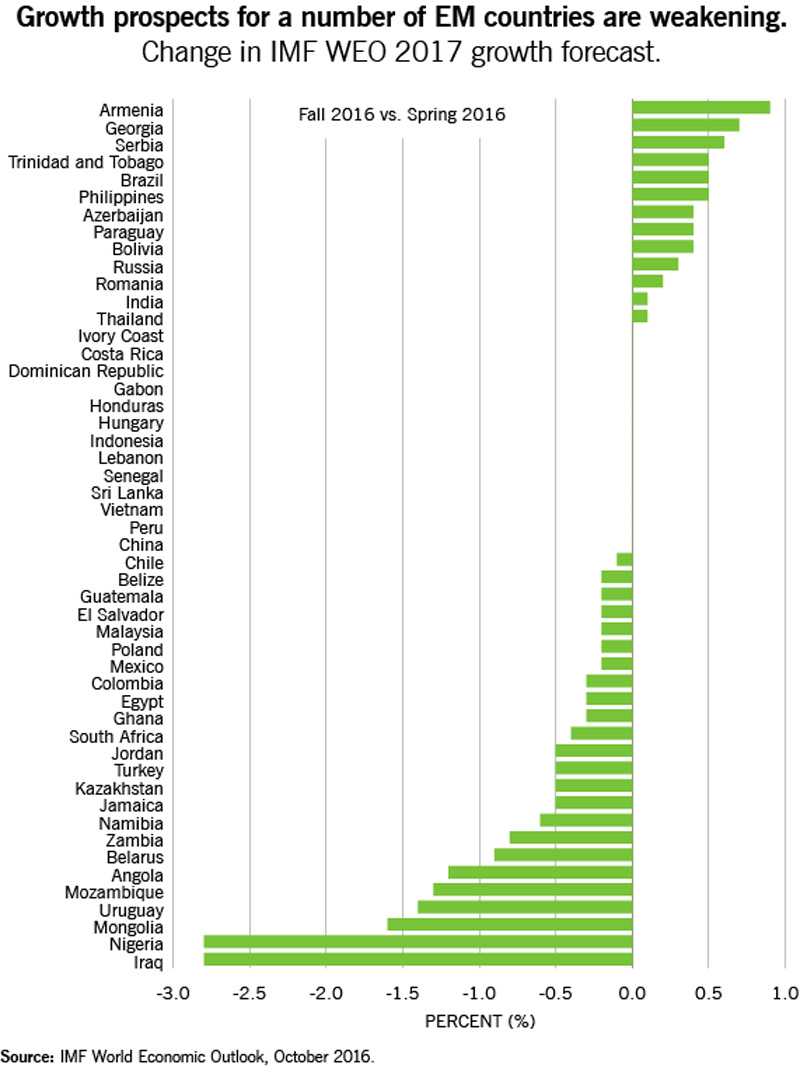

The forecasts for emerging market (EM) and developing countries were also mediocre – 4.2% for 2016 (up 0.1%) and 4.6% for 2017 (no change). There were a number of downward revisions (see chart below) that masked some bright spots in Georgia and Serbia, which both had upgrades higher than 0.5%.

Georgia is implementing ambitious corporate tax reform and is enjoying high foreign direct investment as it builds its role as a transport hub.

Serbia’s extensive IMF-supported reforms to move the economy away from the old communist system are beginning to bear fruit.

- More typical were the EM downgrades:

South Africa’s reduced forecast of 0.4% stemmed from a continuation of low commodities prices, dysfunctional politics and corruption. - Nigeria had a whopping 2.8% downward revision to the country’s 2017 growth forecast, to set it at a mere 0.6%. Nigeria has been hobbled by its dismal response to lower commodity prices, overvalued currency, capital controls and import restrictions. These have damaged growth prospects that were among the promising on the continent just a short time ago.

Amongst attendees, the mood on EM was relatively balanced – not exuberant, but not overly pessimistic. The prospect of the European Central bank tapering its accommodative policy was regarded as unlikely, and policymakers were generally relaxed on the implications for EM if the Fed hikes rates.

Discussion of China was surprisingly limited. There were bearish views on Turkey and South America, but a more optimistic tone for Latin America. Despite the mix of views, overall interest in EM remained high, with record investor attendance, including 900+ people registered for one popular investor conference.