After launching a global supply war, which led to the price of global oil collapsing in late 2014, Saudi Arabia now appears to be signalling a change of policy.

OPEC Secretary General, Mohammed Barkindo, has indicated that he expects a deal to cut production to come from the OPEC meeting scheduled for the end of November. Critically, Russia will also participate at the meeting, with the implication being that Russia would also be part of any production deal. The US presidency is also a key factor, with president-elect Trump’s unfolding policies potentially influencing oil markets in their own way.

Our commodity expert in New York, Daniel Forgie, and one of our Senior Portfolio Managers in London, discuss the new policy and what may be behind the change in position.

Executive Summary

- Both Saudi Arabia and Russia appear to be shifting towards an agreement on production After running production at high levels for over a year we believe that there are now a number of factors which explain this, and which makes us more confident that an agreement will be made.

- A target of 5m b/d was originally quoted, but OPEC production has since increased substantially to 34m b/d as production in both Nigeria and Libya has recovered strongly.

- With the level of oversupply in global oil markets declining sharply in 2017, an agreement, if struck and adhered too, would firmly underpin oil Prices remain capped by US shale, though, and are unlikely to breach $60 on a sustained basis.

Saudi: Why Now?

Investors are currently speculating why Saudi Arabia may be about to agree to a deal. Rather than any single factor, it seems probable that there are a number of reasons for the change:

1. Saudi has been running production too hard for too long

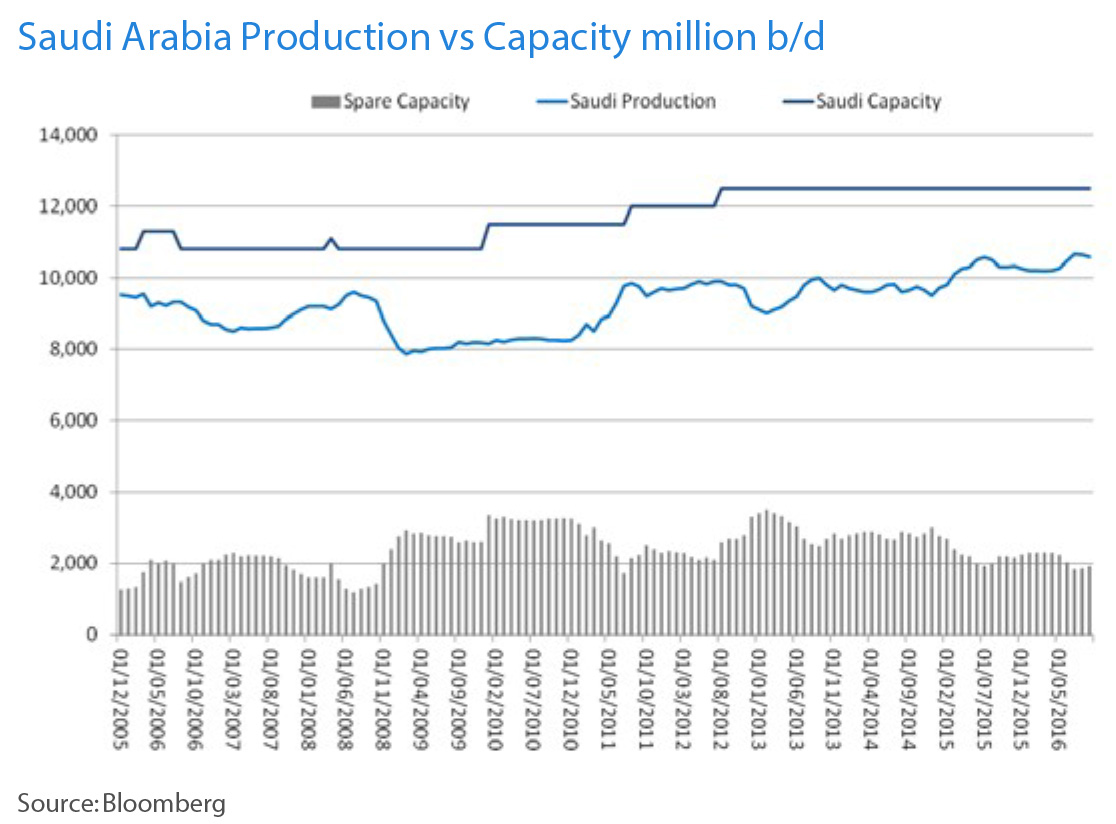

In 2009, Saudi Arabia invested heavily to expand its production capacity, from just less than 11m b/d to 12.5m b/d. By ramping up production, though, its estimated spare capacity has declined to under 2m b/d. Some commentators believe that the effective capacity is actually below 12.5m b/d, which may mean the situation is even tighter.

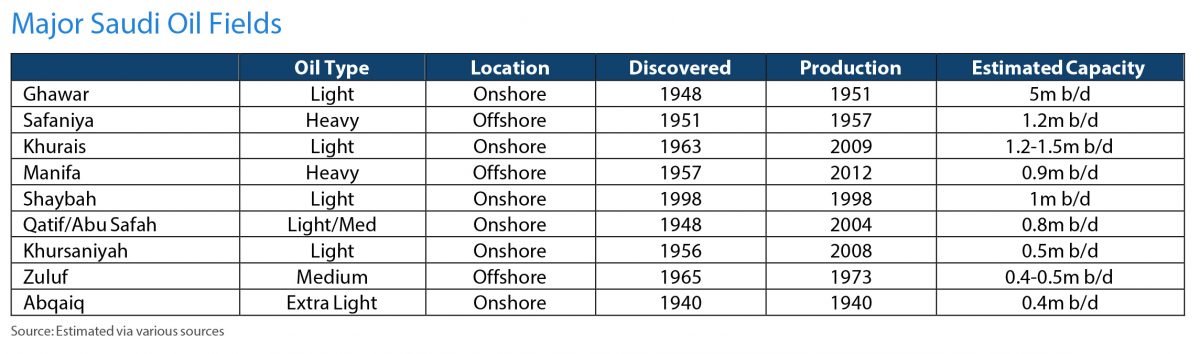

One of the issues that Saudi has to deal with is the fact that much of its production comes from fields that have been in production for decades, with close to 50% of production coming from a single field, Ghawar, which started production in 1951.

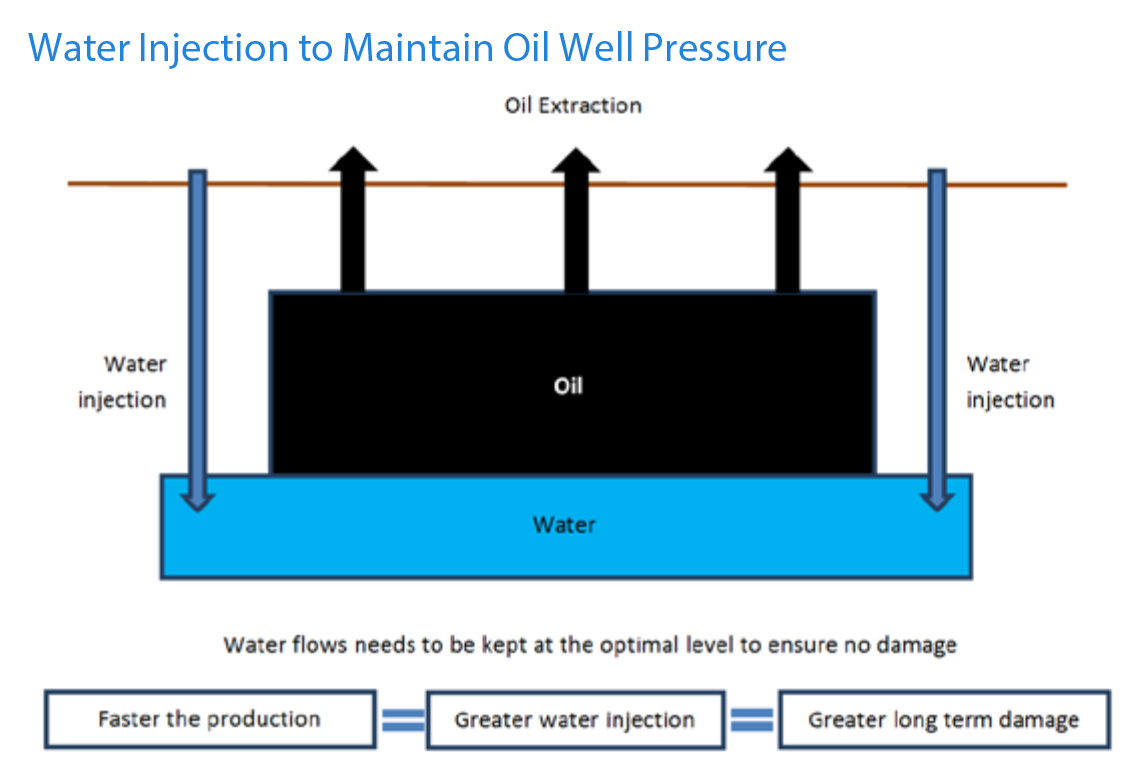

The reason that many of these older fields have been able to operate for so much longer than first thought is due to injecting water below the oil bearing rock, raising the pressure and increasing the flow of oil from wells. Since 2011, Saudi Aramco has also been developing a CO2 injection project at Ghawar that it believes will over time increase total recovery by an additional 10-15%.

Water injection is a complicated technique and faces a number of potential complications. Water can leak into areas it is not supposed to reach, and some water will end up being pumped back out of the oil wells with the oil. This is known as the ‘water cut’, which is the percentage of water that is produced relative to the total liquid produced from an oil well. The higher the level at which production is maintained, the greater the potential problems, and higher the water cut will tend to be. A period of slower production would allow more maintenance and reduce the risks of medium term damage on these older fields.

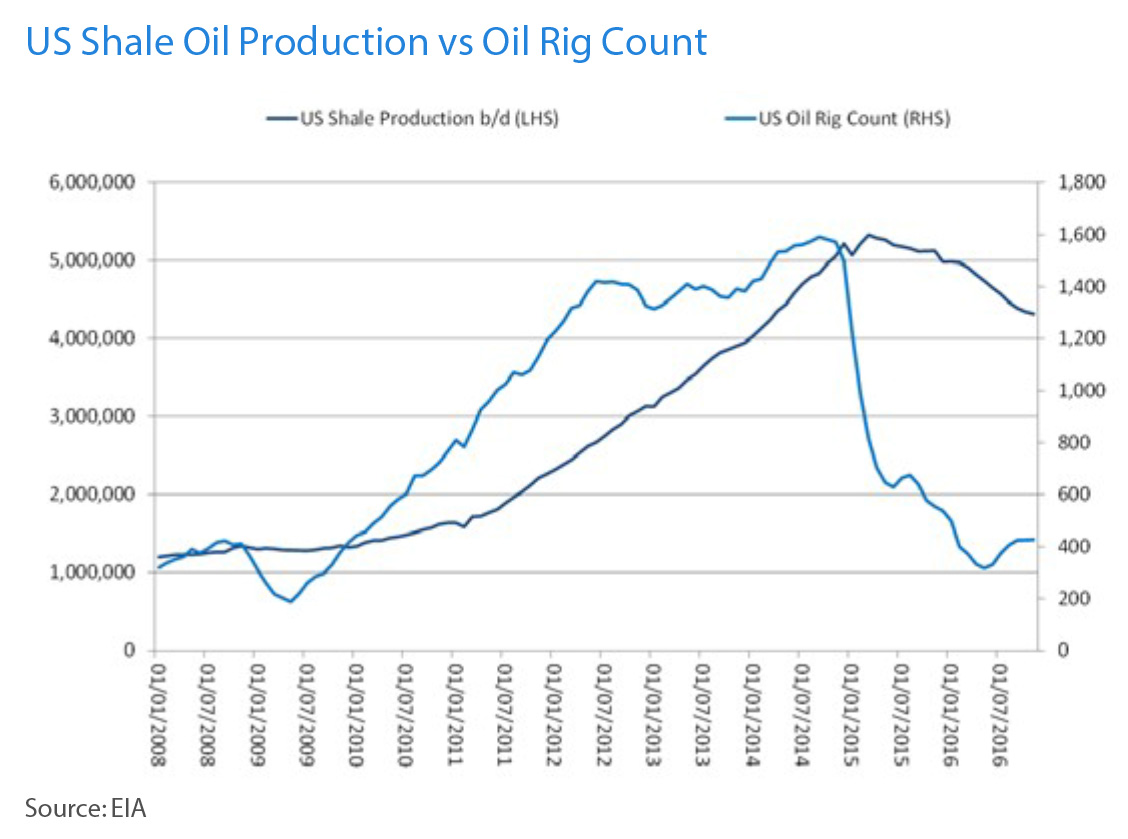

2. Saudis are more confident that US shale oil needs higher prices than previously thought for meaningful production increases

Data from the US Energy Information Administration (EIA) shows that US shale oil production peaked in March 2015 at 5.33m b/d, and it now forecasts that by November production will have declined by over 1m b/d. Only firms operating in the Permian basin, which has the lowest costs, have been able to increase production, with other areas still in decline.

The US rig count has started to pick up as prices have risen to $50 a barrel, but US production is still declining in aggregate, even at these prices.

3. The Saudis need a higher oil price for revenue purposes

Despite an austere 2016 budget, Saudi Arabia is still expected to record a budget deficit of 326bn Riyals ($87bn), down from 367bn Riyals in 2015. This represents a budget deficit in excess of 10% of GDP, which needs to be financed partially by asset sales and partially by borrowing. This entailed Saudi Arabia bringing a record $17.5bn bond issue to market in October.

The IMF estimates that under the 2016 budget, the Kingdom’s fiscal breakeven price for oil drops to $66.7 a barrel, down from

$94.8 in 2015. With global demand and supply more in balance in 2016, a production cut should be more effective than before, and could allow prices to be sustained above $50 a barrel. This would reduce the pressure on Saudi’s deficit and, over time, continued growth in global oil demand, combined with the sharp fall in global investment, should sustain higher prices even if US shale oil production starts to grow once again.

The answer to ‘why now’ is probably due to all three of these issues rather than focused on a single one, but, it also means that a production cut at the November OPEC meeting could be more of a necessity than a choice. All three of these factors are also relevant to Russia, which has also been running at a high level of production in order to boost revenues. Russia also has a number of oil fields which have been in production for decades.

Pre-meeting talks in Vienna, however, resulted in both Iran and Iraq insisting that they be exempt from any cuts, and twelve hours of negotiations provided no agreement. Iran wants to increase its production from 3.8m b/d to 4.2m b/d which is the same level as its production before sanctions were introduced. Iraq, faced with rising military costs from its battle with Islamic State, is looking to have its production level frozen at 4.7m b/d. Even if both Saudi Arabia and Russia now want to reduce production a compromise with these two countries will be key to the final deal.

———