An investment bond gives you certainty and simplicity in estate planning.

Clients spend a lifetime saving and building their wealth, however without an effective estate planning solution, families can face dire consequences on death.

These consequences may include:

- distribution to the wrong beneficiaries

- high legal fees

- lengthy delays in accessing estate proceeds

- erosion of wealth due to taxation implications

- confusion and stress

These consequences can occur when estate protection and planning is considered as the last phase after investment decisions have been made. Estate planning should be considered simultaneously, early in the financial planning process.

Getting this phase right can get your clients assets, in the right hands, at the right time.

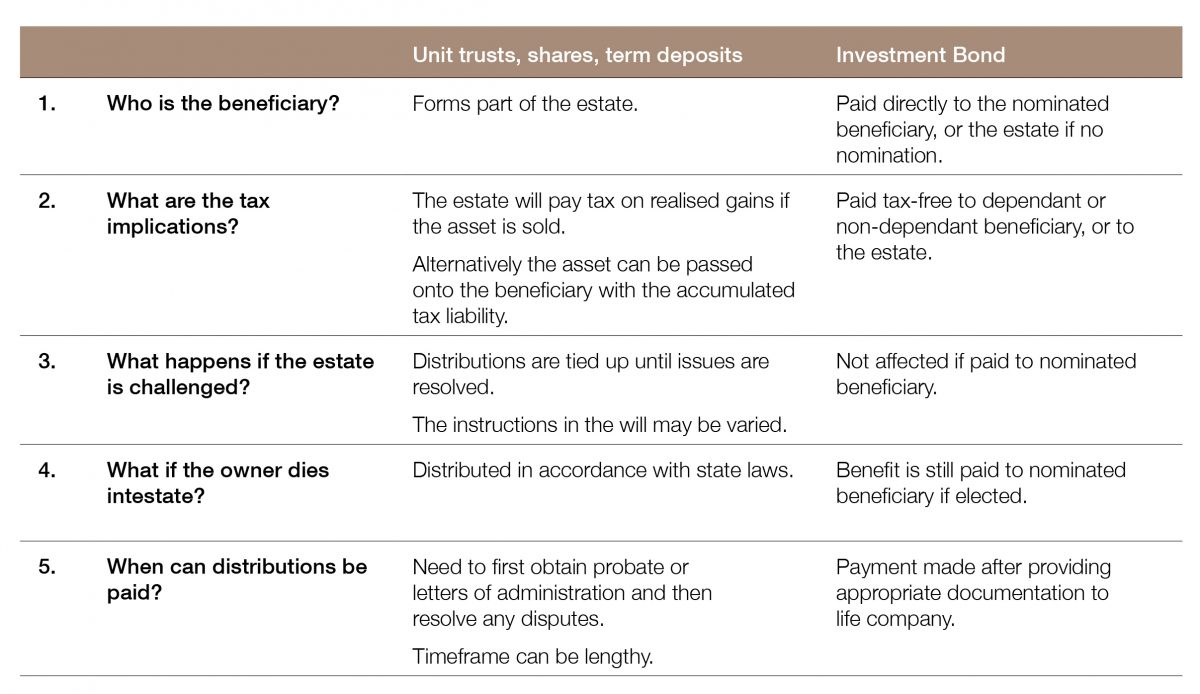

Avoid potential issues with wills and estates

An investment bond may provide greater simplicity and control over death benefits than other investment products such as unit trusts, shares or term deposits.

Upon death, most investment products form part of the estate and may be caught up in any actions taken against the estate. It is also left to the executor to make decisions about the distribution in accordance with the terms of the will.

These actions usually cannot be undertaken until probate or letters of administration are obtained. So the whole process can take months or even years if the estate is complicated or being disputed.

Once distributions are made, tax may be payable by either the estate (if assets are sold) or the beneficiary when assets received in-specie from the estate are subsequently sold.

In contrast, the death benefits from an investment bond can be directed to a nominated beneficiary. Investment Proceeds are paid tax-free to dependant and non-dependant beneficiaries regardless of how long the investment has been held.

Building wealth in an investment bond may reduce the risk of disputes over estates and enable the benefits to be paid more quickly.

Investment proceeds are paid tax-free to dependant and non-dependant beneficiaries regardless of how long the investment has been held.

What if a client dies intestate?

A significant number of people die each year in Australia without a valid will.

Reports state 45% of people may not have a valid will.[1] Some simply don’t get around to arranging a will. You may also have clients who experience a change in circumstances (such as divorce or marriage), which may invalidate a will. Errors in executing a will can also cause it to be invalid.

If a client dies intestate, assets that fall into the estate will be distributed according to the relevant state laws.

With an investment bond, if a beneficiary is nominated, the proceeds will be paid directly to the beneficiary or entity regardless of whether a valid will exists or not.

The investment bond edge

The advantages of an investment bond in an estate protection and planning strategy are summarised in the table below.

Other advantages of investment bonds

Investment bonds offer a number of advantages. These advantages compare favourably to alternative products as summarised below:

-

- Flexible investment options

Investment bonds allow clients to access many asset classes and provide a market-linked investment vehicle to help meet investment goals. - No limit on the investment amount

There is no limit on the amount that can be invested to establish an investment bond. Investors can also make subsequent investments up to maximum of 125% of the previous year’s contribution without restarting the ten year period. Investors can choose to start new investment bonds if higher amounts are to be invested. - Flexibility

Investment bonds give investors the flexibility to access funds at any time, which can act as a hedge against the restricted access for superannuation. - Capital gains tax simplicity

Investment bonds provide simplicity as earnings are automatically reinvested in the bond. This means reinvestment dates do not need to be tracked for capital gains tax purposes. Investors can also switch between investment options without triggering personal capital gains tax. - Transfer of ownership

The ownership of the investment bond can be easily assigned or transferred at any time. The original start date is retained for tax purposes. This may not be achieved within a company structure without creating tax liabilities. - Bankruptcy protection

Investment bonds may offer protection from creditors in the case of bankruptcy.

- Flexible investment options

Estate planning – Case study 1 – Complicated family arrangements

It is becoming increasingly common for family arrangements and structures to be complicated, with second and third marriages, step children and non-traditional family structures presenting a range of issues when passing assets from one generation to another.

With an investment bond, investors are able to pass on their assets by nominating a beneficiary, this may be ideal for multiple beneficiaries who are not dependents’.

Let’s take a look at Hilary age 68, Hilary has 4 children from her first marriage, none are financially dependent. Hillary is married to Brian, her second marriage and Brian has 2 non-financially dependent children from his first marriage.

Hilary’s main estate planning concern is leaving non superannuation assets accumulated during her first marriage to her 4 children.

Investment Bonds

Hilary could consider investing her non superannuation assets into an Investment Bond, with her 4 children as nominated beneficiaries. Hilary remains the policy owner and life insured.

If Hilary needs to access the funds during her lifetime she can as policy owner. This ensures that on Hilary’s death, the proceeds of the investment bond are paid to her 4 children and does not form part of her estate and won’t be subject to the costs and delays often associated with obtaining probate.

Estate Planning Case study 2 – Leaving a bequest

Jason was keen to leave a bequest to the Catholic School he attended, his children attended and his grand children attended. Jason wanted this bequest to sit outside of his will and wanted a seamless transfer of assets on his death to pass directly to the school.

Jason invested $100,000 into a Centuria Investment Bond and nominated his old Catholic School as the beneficiary, this ensures on Jason’s death the proceeds of the investment bond are paid directly to his old school and are not subject to the delays associated with obtaining probate.

[1] NSW Trustee & Guardian: Attorney General & Justice, Frequently asked questions on wills, www.tag.nsw.gov.au/wills-faqs.html

———-