Global CIO warns: Passive is a crowded trade – regime changes play into the hands of active investors

With markets responding favourably to the rhetoric emanating from the new Trump administration, choosing a passive approach to investing could prove hazardous, according to global equities specialist Ariel Investments.

Speaking at a media briefing in Sydney last week, New York-based Rupal J. Bhansali, Chief Investment Officer, International & Global Equities at Ariel Investments, articulated her position that the Trump agenda includes many factors that an index ignores – from foreign policy to fiscal policy – presenting greater risks for passive investors and greater opportunities for high conviction active managers to generate alpha.

Ms Bhansali said she believes key proposals and executive orders in just the last month, such as changes to ObamaCare, the immigration ban and potential legislation to modify the Dodd-Frank Act, have brought greater uncertainty and volatility for many sectors, countries and asset classes.

Ms Bhansali said she believes active investing has tended to do better in choppy markets fraught with ambiguity.

“Passive investors may find they have been penny wise and pound foolish by unduly focusing on low costs at the expense of higher risks,” she said. Risks of excessive allocations to passive include liquidity risk, valuation risk and market timing risk.

“I think passive has become a very crowded trade of late. Chasing what is in vogue has never been a successful recipe for securing long-term returns but instead often proves to be a precursor to large losses or underperformance.

“In fact, going passive is an active decision in itself – it assumes active managers continue to underperform passive. But we’d argue that the massive changes afoot in political and economic regimes, from the UK to the USA, play into the hands of active managers,” she said.

Horses for courses

Ms Bhansali said the age-old active versus passive argument was less about one approach being superior to the other, but rather an appreciation that each approach outperforms in certain market environments.

“Outperformance of each approach is cyclical, not secular,” she said. “Studies have shown dramatic reversals occur when the active style suffers bottom decile performance versus passive for several years, and vice versa.”

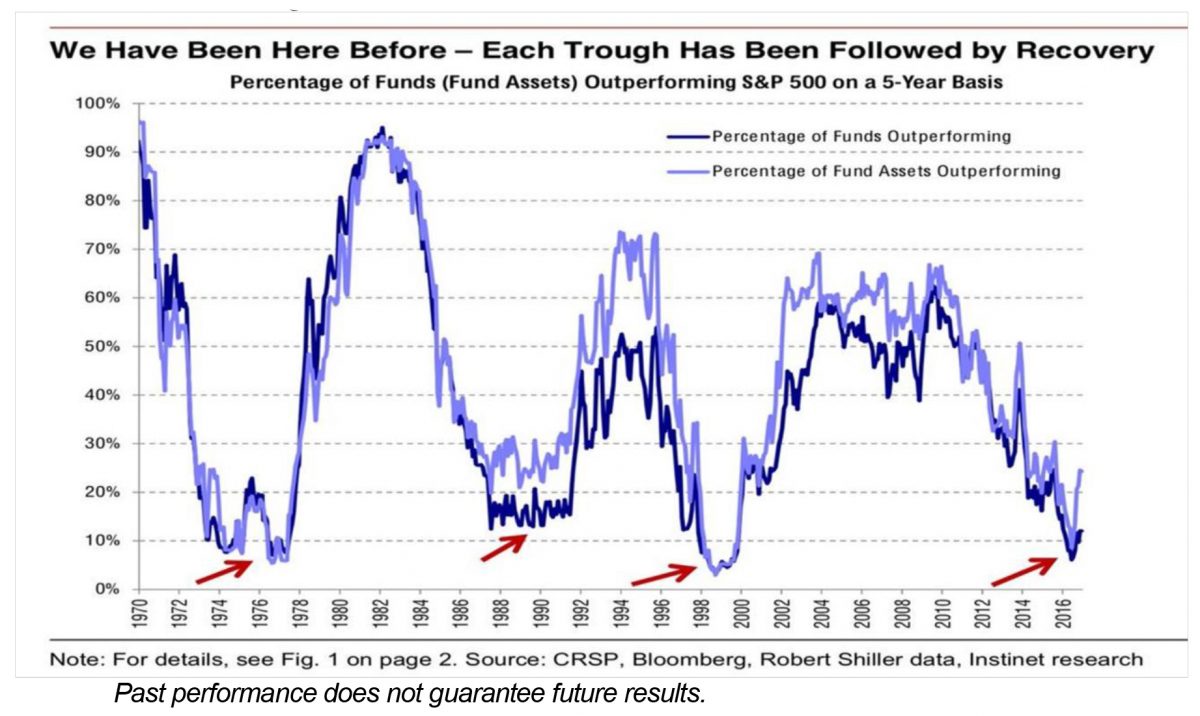

Ms Bhansali pointed to a chart showing the percentage of funds outperforming the S&P 500 on a 5-year basis going back to 1970 – to show how close investors may be to a reversal in favour of active management:

Sector impacts

Ms Bhansali said that by applying a contrarian approach, Ariel continues to find good opportunities in spite of – and sometimes because of – the political uncertainty. She views the healthcare sector as a current favourite with promising potential.

“Pharmaceuticals is a sector that has underperformed the S&P500 by nearly 40%,” Ms Bhansali said. “We think no matter what the results will be for ObamaCare plans or whatever form its successor takes, innovative drugs which save lives will receive their fair economic return. In fact, this myopic focus on near term regulatory risk is ignoring the Silicon Valley-esque innovation going on in drug discovery – whether it is in personalised medicine via combination therapies or game changing concepts such as gene editing.”

She said one such company was Gilead which has come up with a cure to a life-threatening disease Hepatitis C.

“In my view, the stock is cheap as it has been sold off on the back of concerns about sustainability of their Hep C franchise. Pessimism has gone to extreme levels where no credit is given for their promising pipeline. Even ignoring the pipeline, the existing products in the market generate so much cash that it could buy back the entire company in six years at the current rate. It is our largest healthcare holding, as we believe it has very compelling upside potential versus downside risk, further buttressed by a strong net cash balance sheet,” Ms Bhansali said.

Ms Bhansali said another area of opportunity in many global markets are Exchanges which are fee based businesses within the financial sector as opposed to interest rate spread based businesses such as banks.

“Markets have re-rated banks all over the world as beneficiaries of rising interest rates but ignored the benefit of increased interest income on free floats on clearinghouse balances and the increased hedging activity that follows interest rate volatility at Exchanges.

“Chicago Mercantile Exchange and Deutsche Boerse are second order beneficiaries of this development but their stocks have lagged the mainstream financial sector,” she said.