Tax Effective Investing outside of superannuation – look no further than investment bonds

Advisers and investors urged to look carefully at options outside of super

Following changes to superannuation legislated in 2016, the Treasurer has been vocal in his view that superannuation should be ‘fit for purpose’. He also acknowledged that ‘a prosperous Australia needs a well-targeted superannuation system that supports and encourages all Australians to save’, but specified that its purpose is to ‘provide income in retirement to substitute or supplement the Age Pension’.

Neil Rogan, General Manager, Investment Bonds Division at Centuria explains why changes to super mean that now may be an appropriate time to educate yourself about tax-effective investment strategies outside of super. It is an appropriate time to take a closer look at how best to structure investments, including super, when it comes to estate planning.

But first, below is a brief summary of the changes most likely to have the biggest impact.

Summary of the major changes

- Transfer balance cap of $1.6 million on retirement balances. Effective from 1 July 2017 an individual will be able to transfer only $1.6 million into retirement phase accounts. For the small number of Australians with a balance of more than $1.6 million in a retirement phase account now, they will need to withdraw the excess balance or revert it to accumulation phase, where it will be subject to 15% earning tax.

- Lower cap on concessional (pre-tax) contributions from $30,000 to $25,000 from 1 July 2017. Higher concessional caps for the over 50s will not exist after July 2017.

- Cut in annual non-concessional (after-tax) contributions cap to $100,000. This is a concession to community and industry anger when the original announcement was the introduction of a lifetime non-concessional (after-tax) contributions cap of $500,000 to take effect immediately. The lifetime $500,000 has now been scrapped and replaced with an annual $100,000 non-concessional cap to take effect from 1 July 2017 with a maximum of $300, 000 bring forward. However, it is only possible to make non-concessional contributions if your super balance is less than $1.6 million.

- Lowering of the income threshold from $300,000 to $250,000 for 30% rather than 15% tax on contributions which means that any Australian with an income of $250,000 pa or more will pay 30%, double the usual tax rate of 15%, on contributions into super.

- Removal of the tax-exemption for transition to retirement pensions (TRIP) means super fund earnings supporting a transition to retirement pension will no longer be tax-exempt.

So what’s the result?

Do you have clients currently using the full concessional contributions cap?

If the changes are passed, clients age 50 or over may need to reduce contributions by $10,000 per year. Clients under age 50 may need to reduce contributions by $5,000 per year. What tax-effective options exist for investment of these amounts?

With only a 30% tax rate applied to earnings, the Centuria Investment Bond provides a tax effective investment option for clients earning over $37,000 per annum, with full access to the investors accumulated investment balance if the client’s circumstances change.

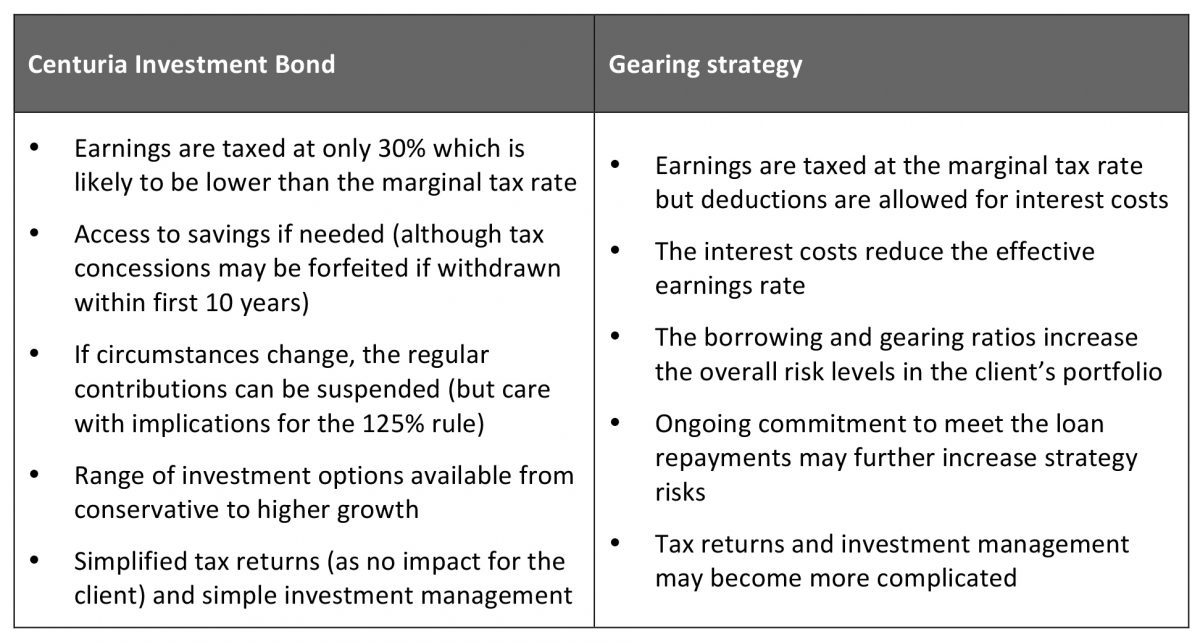

Another tax-effective option is to use the $5,000 or $10,000 a year to make repayments on a loan used for investment purposes. The investment bond is potentially a lower risk strategy than undertaking a gearing strategy.

A quick comparison of main features of these two strategy options is:

The 125% rule

For clients earning over $37,000 per year (giving them a marginal tax rate over 30%) the investment bond should be held for at least 10 years to maximise the tax concessions.

Each year additional contributions can be made, and as long as the contributions do not exceed 125% of the previous year’s contributions, the ten years is counted from the date the investment was opened for the full balance.

Options for reduced non-concessional contribution cap

Under current rules, clients can contribute non-concessional contributions (NCC) up to $540,000 every three years. Clients will be limited to only $100,000 per annum with a maximum of $300, 000.

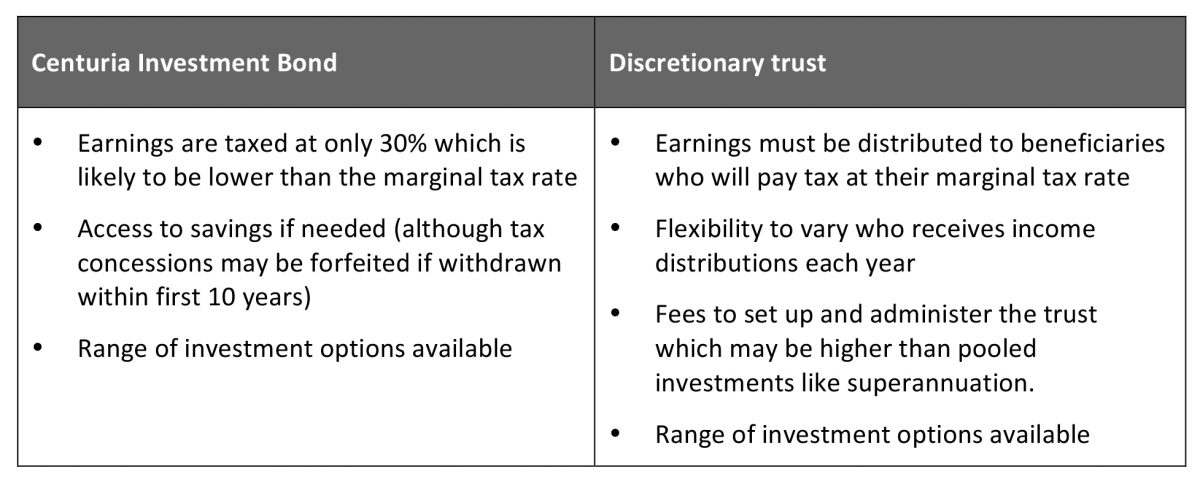

Clients with savings or windfalls (such as inheritances) to invest may need to look for other tax-effective options for accumulating wealth. For clients who earn over $37,000, the Centuria Investment Bond may be an attractive option.

Another alternative may be to use a discretionary trust. In some family situations, these may offer flexibility to vary who is the beneficiary of distributions each year. If the family includes low-income earners, this may provide taxation advantages.

A quick comparison of main features of these two strategy options is:

Comparison checklist

While options to reduce tax payable can help to grow savings more quickly, investment decisions should not be driven by tax alone. The full circumstances of clients should always be considered to understand:

✓ The client investment objectives and timeframes

✓ The risk profile

✓ Risks in the strategy and how the client feels about each risk

✓ Flexibility to deal with unforeseen circumstances

✓ Simplicity and ease of management

✓ Cashflow implications

✓ Taxation outcomes

✓ Impact on Centrelink/Veterans’ Affairs payments

✓ Options and strategies for estate planning

It may now be time to review your client’s estate planning arrangements, particularly where the bulk of your client’s wealth is held in superannuation assets.

Regardless of the recent changes, and the fact that it is inaccessible until the age of 55 or 65 depending on your age, super is still one of the most tax-effective means of investing.

However, the annual cap provisions for non-concessional contributions, along with the transfer balance cap of $1.6 million into retirement phase accounts mean that for higher net worth individuals, the ability to contribute larger lump sums into super in the future has been seriously curtailed.

Tax-effective investment strategies outside of super do exist

Returns from most investments outside of super are taxed at the investor’s marginal tax rate, but there are some structures which are tax-advantaged. Investment bonds, for example, are flexible and simple investment structures that have stood the test of time.

Tax is paid on returns within the bond structure at the company rate of 30%, and are not distributed to the investor, but rather re-invested in the bond. For this reason, investors do not need to declare income from the bond or include it in their tax return. Better still, if they remain invested in the bond for 10 years, all returns are distributed tax free. There is no limit to the amount which can be invested in an investment bond, and additional contributions can be made every year, up to 125% of the previous year’s contribution.

Unlike super, contributions can be made at any time or age, and are not restricted by retirement or work tests.

If funds in the bond remain invested 10 years, no tax is payable, but investment bonds are more flexible than super, in that funds can be accessed at any time. However, depending on when the withdrawal is made, investors may need to pay some tax.