One of the great investment debates centres on whether you should be a value or a growth investor. We believe there’s more than enough evidence to support the view that value investing has delivered superior returns over the long term. Chart 1 shows the performance on the S&P 500 Value and Growth indices over the past 40 years, where value has clearly outperformed growth.

This hasn’t been true for the past few years though – since the GFC, growth stocks have outperformed value stocks. This was very apparent in 2015, where despite the ASX200 returning less than 3% for the year many small- and mid-cap growth stocks delivered eye watering returns; the two poster boys being Blackmores and Bellamy’s, who delivered 534% and 715% respectively.

In this paper we look at the extent of that performance differential between value and growth, why it has happened and why 2017 could be the year that value reasserts its superiority.

Cheap – and staying cheap

Since the GFC, value-oriented equity strategies have underperformed their growth counterparts – not just in Australia but around the world. Rather than revert to the mean, cheap stocks have exhibited a frustrating pattern of staying cheap. Meanwhile, almost any company delivering growth (seemingly regardless of whether it’s organic or purchased) has experienced significant multiple expansion.

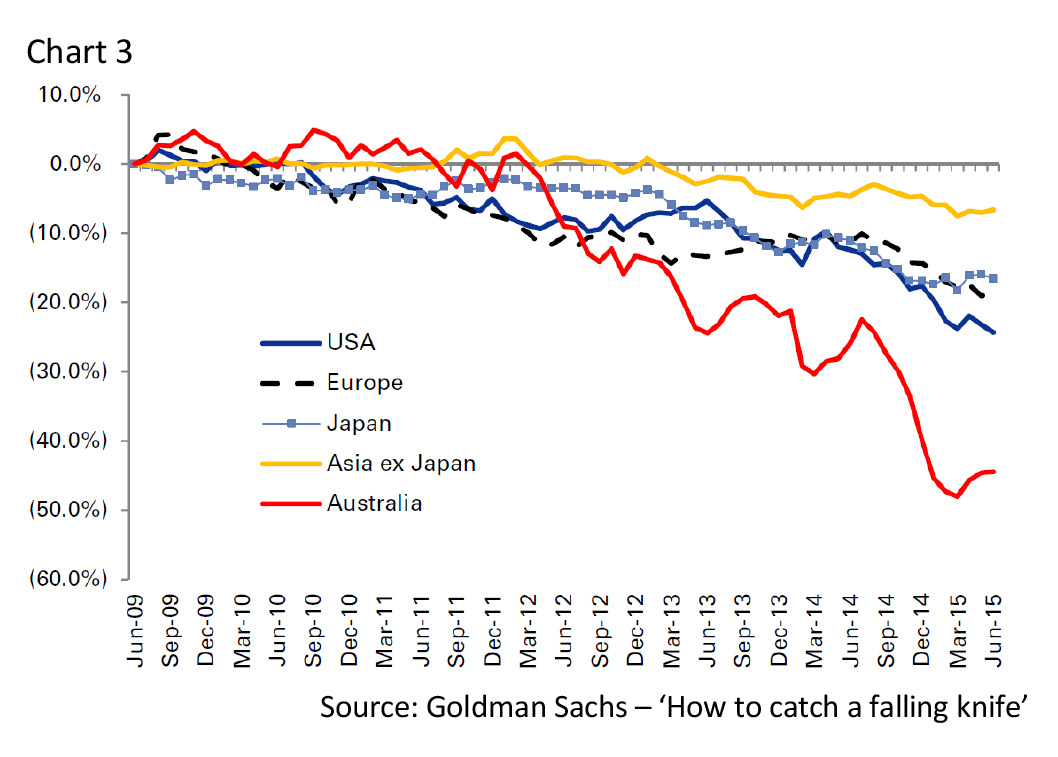

As Chart 2 illustrates, since 2008, the MCSI World Value Index has generally seen underperformance relative to its growth peer. Value underperformance has been particularly marked in Australia where value has lagged growth by more than 40% since 2009, as depicted in data from GS in Chart 3. In short the ASX has gone from one of the best markets for value investing to the worst.

Why has value struggled?

So what’s behind the recent underperformance of value – a strategy which has historically provided a good result for Australian equity investors? Studies have suggested that periods of outperformance for value strategies are tied to market, interest rate and economic cycles:

- In terms of market cycles, history suggests that the best period for value is when the market peaks and pulls back from expensive levels. In these conditions, higher priced growth stocks tend to be in trouble and investors flock to the defensiveness offered by cheaper valuations.

- As for economics, it has been observed that the ideal time for value is when profits start to rise. At this point, growth becomes the abundant commodity, while value looks scarcer. A rising tide lifts all boats – but as value stocks are cheaper, their performance tends to be superior.

- Lastly, all things equal high interest rates are good for value – as higher P/E growth stocks, like longer duration bonds, are penalised more as the discount rate rises.

Put simply – a long drawn-out rally, with low rates, little fear but with little conviction, is about as poor a scenario for value as could be imagined. The post-GFC world has been a perfect storm for value strategies globally. Let’s delve more deeply into why.

Mean reversion

Some analysts – notably Credit Suisse – say one factor is simple mean reversion. In the early days of GFC-inspired monetary easing, value did outperform. With risk being taken out of the market and the prospect of a return to economic growth it made sense to buy the cheapest stocks likely to benefit from those conditions. Over time though the gap between the valuations of growth and value stocks have narrowed – making growth and momentum plays more attractive.

“Growth at any price” in a low returns environment

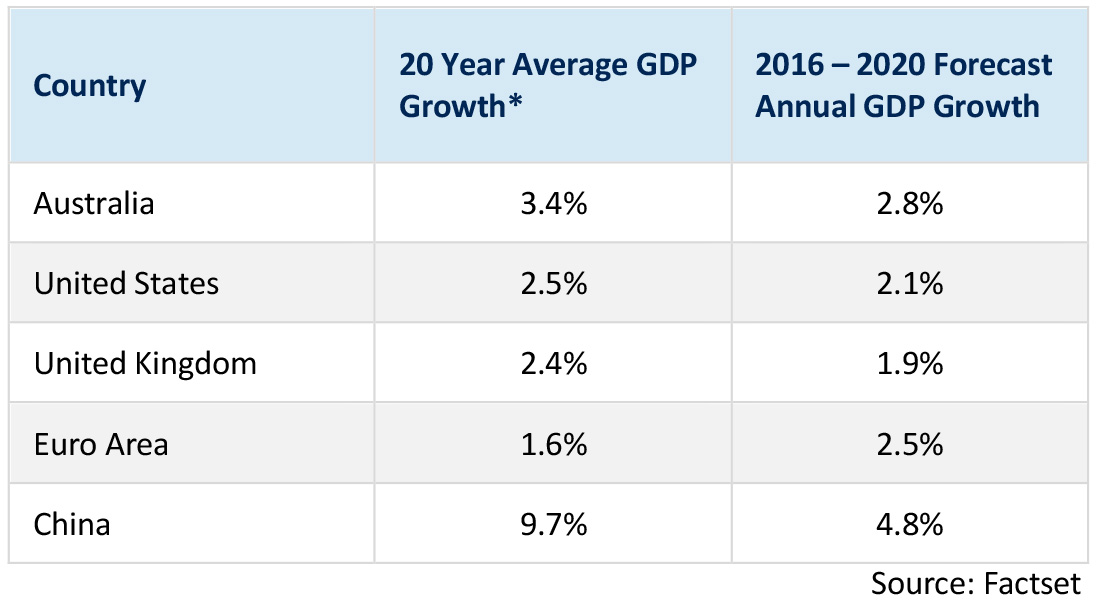

Since the GFC the level of growth in Australia and globally has been extremely low, and appears poised to stay that way for the foreseeable future (see table below). Very few companies or industries are enjoying rapid growth, so it makes little sense to reach too far and take too much risk by paying a large multiple for a stock. However, value investing appears to have been replaced by a preference for “growth at any price” (GAAP), with investors willing to pay very high multiples for any stock delivering growth – almost irrespective of whether that growth is organic or acquired. The problem with GAAP is that a) eventually it will come to an end and b) if too much future growth has been priced in investors can never hope to make a real return to justify the P/E or risk capital losses.

Investors have treated equities like bonds

The post-GFC world has been characterized by low growth and low rates. Bond yields hit all-time lows as investors sought safe haven assets generating an income. Given the suppressed returns investors were receiving from cash, term deposits and bonds, they began turning to equities with strong dividends as a substitute. In Australia, Telstra Corporation Ltd (TLS) is a prime example – since 2011 its share price has doubled, yet earnings have not significantly grown. Investors are treating TLS like a bond because of its long-term, predictable earnings stream and strong yield. Meanwhile anything representing value has been broadly ignored by the market, which goes to explaining why cheap stocks are staying cheap.

Expensive defensives and the hunt for yield

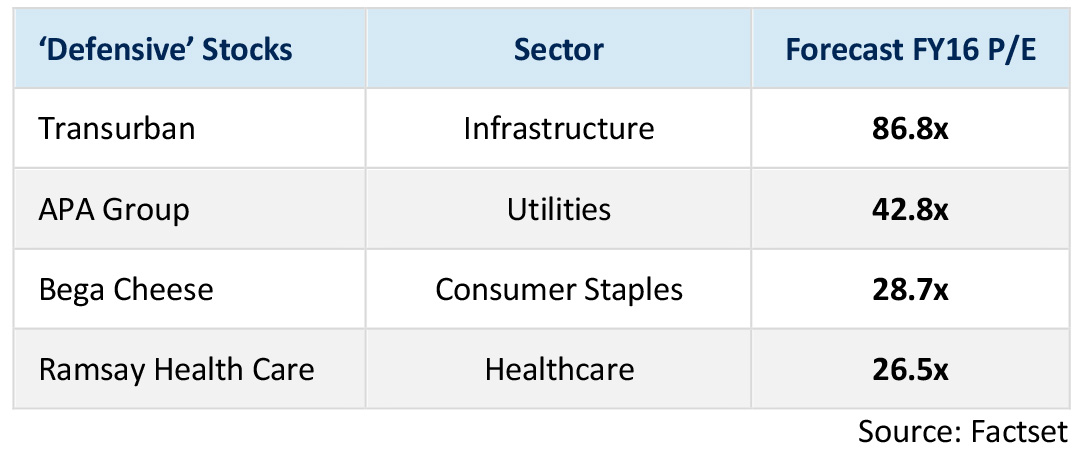

Since 2009 many investors have positioned their equity exposure to be overweight so-called ‘defensive’ stocks, such as:

- Utilities and Infrastructure for their oligopoly features

- Consumer Staples for their reliable future earnings streams

- Healthcare for industry tailwinds – including earnings underpinned by government funding.

While many believe these are safe investments and they have characteristics typically prized by value investors (predictable earnings, large economic moats etc.) post-GFC market trends means some investors are exposing themselves to significant risk by paying inflated valuations for these stocks.

This issue is plainly distinguishable when we look at toll road owner and operator Transurban Group Ltd (TCL). The stock is paying a dividend yield of approximately 4.15% (only 16% franked) which looks relatively attractive when compared to term deposits and bond yields.

However, investors are paying 87x forecast earnings to receive that income. What’s more, the company has in excess of $10 billion in net debt.

With historically low rates around the globe, investors have become fixated with yield – seemingly regardless of what price tag it comes with. The hunt for yield has driven up prices in stocks across various sectors, but we believe these valuations are unsustainable. Nowhere is this thematic most easily observable than in Australian banks. They started to rally in mid-2012, peaked in early-2015 and have since pulled back between 20-40% from their April 2015 highs.

Will 2016 be the return of value investing?

Bank of America Merrill Lynch Global Research has forecast that 2016 will be the year that value investing outperforms growth. BAML is predicting higher interest rates and better growth in profits in 2016, driven by a strengthening US dollar and lower oil prices. Based on their research, a 5% or greater increase in profits has historically been accompanied by value outperforming growth 71% of the time. BAML is forecasting a 5% increase in profits for 2016.

Recent economic data supports BAML’s outlook. In the US, core inflation has continued to tick up since mid-2015, hitting 2.33% in February ’16 – the highest reading in 44 months. Meanwhile US unemployment remains steady at 5% and jobs growth is strong with non-farm payrolls increasing by 242,000 in February. Closer to home the Australian economy grew faster than expected in 4Q ’15, with GDP growing 3% year-on-year and 2.5% for calendar 2015.

The Perpetual Investments equity team believes that equity markets are semi-efficient, and that opportunities exist to add value through the selection of quality, well priced securities. We believe that these can be identified through thorough, fundamental bottom-up in-house research.

Because something is cheap does not necessarily mean it is good value. Benjamin Graham, the founding father of value investing, observed that the greatest losses result not from buying quality at an excessively high price, but rather from buying low quality at a price that seems good value. Some companies are ‘cheap’, but will likely stay cheap due to challenging market dynamics, a weak financial position or inferior management. We have managed to deliver continued relative performance with a value bias by staying disciplined around owning quality companies, and avoiding “value traps”.

The Process in action

Our position in eBay was first bought in 2013. We were attracted to both the ‘Marketplaces’ (mostly ebay.com) business, which is one of only two leading ecommerce platforms in the USA, along with the PayPal business, which is one of the only payment platforms businesses in the world that has scale on both the consumer side (with 169 million active accounts) and the merchant side (with 10 million merchants). This characteristic strengthens PayPal as a payment platform, and is incredibly difficult to replicate. The separation of PayPal from eBay unlocked financial value for investors. When PayPal was part of eBay, we felt the market undervalued the business and underappreciated its quality and growth potential. The separate listing helped remove this bias, which we saw in the strong performance leading up to its separation, and the subsequent price action in both stocks.

Summary

With valuations stretched and investor sentiment diminishing, the scene is set for volatility in equity markets to be ongoing. Importantly, quality stocks tend to outperform amid increased volatility.

———-