Robo-advice portfolios boosted by themes and factors, Quantifeed analysis shows

Gaudi Schneider

Returns from the17matic robo-advice portfolios can be boosted by using quantitative screens, without increasing risk for investors, according to a new white paper by Quantifeed.

The leading provider of B2B digital wealth management solutions in Asia Pacific, Quantifeed, today released the paper Designing thematic indices with a quantitative factor. It outlines an improved methodology for global thematic index construction, which features in its portfolios for financial institutions servicing the mass affluent segment in the Asia Pacific region.

Gaudi Schneider, Quantifeed’s Senior Quantitative Strategist and author of the white paper, says there are two distinct approaches to building indices: thematic indices, based on investment themes; and factor indices, based on empirical research of past investment returns. While the former approach is based on a forward-looking growth story for a niche industry, the latter uses quantitative variables, such as volatility, yield, size and momentum.

“The thematic and factor approaches to building indices have their own individual advantages for digital wealth management services. However, at Quantifeed we believe that through a calculated combination of both, financial institutions can deliver a much better risk-adjusted performance,” says Mr. Schneider.

“Mass affluent consumers in Asia Pacific who are receiving wealth management online can truly benefit from a quantitative overlay to their portfolios.

“Financial institutions, on the other hand, can also capture the opportunity of digital wealth management services not only by servicing this segment of clients remotely, but also by delivering to them an enhanced portfolio performance,” he added.

Mr. Schneider explains that one way of introducing a factor to a given thematic portfolio is to apply weights to securities based on a specific variable, for example, volatility, instead of the standard weights based on market capitalization.

“Low volatility stocks have been shown to outperform higher volatility stocks over extended periods of time,” he says. “Taking advantage of this phenomenon can be achieved by giving stocks with low volatility a greater weight in the portfolio. We call this inverse volatility weighted,” he explains.

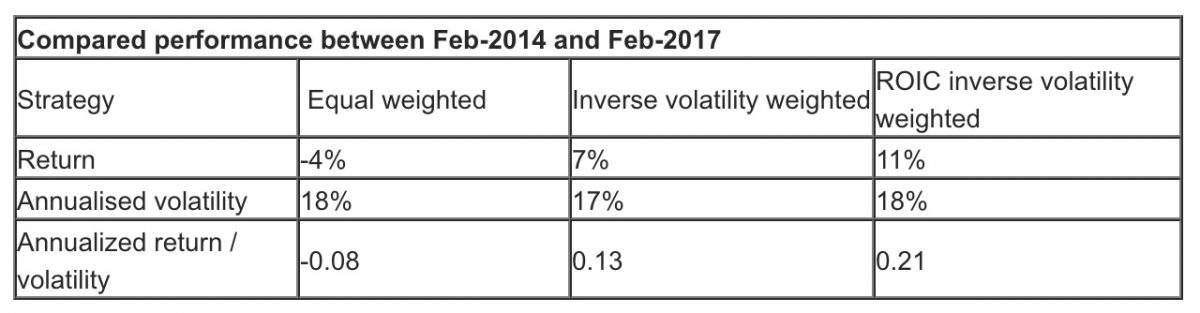

To illustrate the effect that a factor can have on a thematic index, Quantifeed looked at a group of stocks of U.S. listed companies that are active in the design of robots and automation services. By applying the inverse volatility weighting (IVW) quantitative factor to this group of stocks, Quantifeed’s model outperformed the original index by 11 percentage points over a three-year period between February 2014 and February 2017. While the original version of the index declines by 4% during this period, the version with the quantitative overlay rose by 7% during the same period. (See table)

To enhance performance further, Quantifeed’s analysts applied an additional quantitative factor but into the stock selection process. The additional screen included the fundamental measurement of Return-on-Invested-Capital (ROIC), considered by the analysts as an appropriate criterion for the robotics industry, which usually requires large investments in research, factories or machinery.

The results of the ROIC inverse volatility weighted index showed this time a 11% return during the three-year period, leading to an outperformance of 15 percentage points over the original index. (See table)

In neither of these cases did the factorized portfolios gain in volatility versus the original index.

A copy of the whitepaper can be found here: http://www.quantifeed.com/wp-content/uploads/2017/03/Quantifeed-White-Paper_14Mar17.pdf