Smart Defaults: why trustees dumping MySuper members in one investment bucket is no longer good enough in this digital age

What would happen if you as a professional financial adviser placed all your clients in the same investment, regardless of amount involved or remaining human capital, for up to the next 45 years?

Surely your colleagues and peers wouldn’t let you do it! You would lose credibility, face inquiries, lose accreditation and have to leave the industry or worse.

But did you know on the other side of the regulatory fence, in the superannuation space regulated by APRA not ASIC, this is common practice. In fact, circa 80% of working Australian’s or around $500 Billion is invested in this way through MySuper, because members have not told their trustee which investment option to use.

From an advisory business perspective, this is a very important issue. Even if only 1% extra of those MySuper members per year are nudged to become engaged and see a financial planner, then your industry will expand rapidly. That is one way to overcome robo advisers and improve competition.

As reported on 20 March 2017, ASIC’s Greg Medcraft sees need to tackle advice ‘oligopoly’ in Australia and expand competition. If the advice sector (retail, independent, at NFP funds) is to have increased competition, it really does need to take into account a channel to the $500bn, 80% of workforce in MySuper.

Furthermore fixing this single investment bucket approach, for these MySuper members, by more effectively using their remaining investment horizon and retirement lifestyle prospects, will reduce pressure for further changes to the Superannuation System. If the retirement prospects of this 80%, most of who will end up on the part Age Pension can be lifted, the impending national retirement funding gap can be reduced, pressure for continually increasing taxes and placing restrictions on those with higher super balances (your typical client) will be lower.

So good reasons to read this article, understand Smart Defaults, spread the word and shout loudly plus often from the sidelines. There are numerous ways to be involved, right now.

Are Super Funds applying different standards to engaged and disengaged members?

Super funds expend enormous time and energy assisting members who have made an investment choice and are engaged (circa 20%), via their website information, calculators and advice models (Limited, General or Personal) to use the funds investment options (Australian Shares, Balanced, Cash etc.) based on their retirement lifestyle prospects and age.

But at the same time, for the disengaged MySuper members (circa 80%), those who have not made an investment option choice, most trustees funds do nothing. They just dump everyone in the same investment option bucket. This is despite knowing enough about disengaged members to do more for them than is currently the case. (For example, funds know the projected retirement balances or incomes of members, and are now placing them on members’ annual statements.)

To be fair, approximately 1/3rd of funds have moved since 2013 to an age based model for these default MySuper members (be that US styled Target Date or European Life-Stage). This approach blindly reduces risk (e.g. Balanced down to the Cash option, known as a Glide Path) automatically as members get older – just when a member’s balance is highest. The result is lower risk of loss as retirement approaches, known as sequencing risk, which is important but at the huge cost of poorer average retirement lifestyle prospects and lower starting retirement balances.

So there is a problem. Most industry executives agree that current approaches are highly inefficient. Having 20 year olds in the same investment option as 60 year olds is wrong. So is having a 40 year old projected to retire on the full Age Pension in the same investment option as another 40 year old projected to retire with $1.6M in super.

The problem is important and a solution must be found in order for the super sector to meet its new retirement objective (currently being legislated), plus of course trustees meeting their existing obligations to act in members best interests. The status quo is not going to achieve that outcome, the government knows it, the Productivity Commission is reviewing it with changes likely and APRA is focusing on individual funds and their director trustees.

To be clear, it is not that funds and trustees are deliberately applying double standards. Rather there is a need to find a solution and then be prepared from a governance perspective to accept a changed operating environment and innovate.

Innovation

That innovation is happening. On 15 March, Mine Wealth + Wellbeing CIO David Bell launched a new tool, called MDUF v1, it considers the question: “What is a sensible set of financial preferences for a trustee to assume on behalf of a default fund member?”

On 17 March, in the Adviservoice article Why the industry’s “comfortable retirement” measures are wrong, Millimans Jeff Gebler laments that:

“The personalised nature of each superannuation member’s retirement journey means a one-size-fits-all approach simply cannot deliver the necessary information, products and risk management strategies required to achieve everyone’s desired outcomes. Or, as the Productivity Commission’s recent report into the industry’s competitiveness and efficiency put it, “Indicators which focus on the ‘median’ or the ‘average’ user will not necessarily reflect what is optimal for all or even most members”. Funds need to take a more nuanced approach or a lack of member engagement will be the end result.”

The industry association ASFA CEO Martin Fahy warned publicly at their 2016 annual conference in his first major address since taking the role that:

“the superannuation industry is at high risk of being disrupted by the fintech sector. On top of that, 20% of people under 29 have indicated they are looking to change superannuation funds in the next 12 months. We need to lift what we deliver to fund members, how we engage with them, and how we engage with government. People want to embrace the system, and we need to help them do that.”

“If we’re going to be successful, we have to engage on our members’ terms. If we don’t, we will be disrupted. Fintech is currently focusing on banking and payments, but the large pool of superannuation money is not going unnoticed. We are next on the menu.”

He more recently stated “… we need to engage deeply with the messiness of the superannuation value chain. We need open architecture to trump regulatory standards and where a smart teenager in a college dorm might just disrupt super, hopefully from within.”

Innovation may be disruptive, but often it occurs in a collaborative manner and is necessary particularly when the operating environment changes. By definition, it involves a changed mindset – to do the same thing/think the same way, use the same consultants/gatekeepers produces the same outcome/solutions.

This is just as true in finance as elsewhere. For example, conventional investment strategies generally seek to strike a balance between risk and return (the ‘risk/return trade-off’). That is there is a binary choice between risk and return – more risk for more return – less risk for less return. So look no further, do a loop, go back to the start, don’t find a solution – keep the status quo. Right! No wrong the operating environment has changed.

The new retirement objective dictates that a third dimension, time to retirement be added, such that the choice is no longer binary. Instead, more risk can be taken earlier in a working life for some members, less so for others. Plus at the same time lower risk taken later in a working life as retirement approaches, for some members but not others.

It is often suggested with MySuper default members that trustees don’t know enough about the members to tailor or stream retirement outcomes. It is argued that their assets outside super, multiple accounts and personal expectations are unknown to the trustee and hence taking no action to act is fine.

Let’s be clear, in a digital world, with big data analytics and tailoring occurring in many industries, this is no longer acceptable in the super sector. Consider the medical industry for example, they tailored medicines first by category of observable symptoms, then tested and retried ever more tailored solutions. We now have medicines tailored down, in the case of cancer, to individual genes.

Perhaps some super executives and their advisers are not caught by group think on these issues but rather prefer the status quo – where disengaged members remain unassisted because to inform them may involve admitting they’ve been short-changed in the past. They’ve put their trust in the hands of Trustees to manage their investment strategy, but now discover they haven’t accumulated enough for a comfortable retirement. That comfortable retirement level is of course largely personal, defined in members minds based on expectations driven by past information.

Surely it is better to nudge these members into action and engagement now. Provide them time to adjust to the news, contribute more and use the power of compounding. Taking the first step is critical; trustees’ waiting for ever more information is a recipe for ultimate failure against both the new retirement objective and the trustee director’s fiduciary obligation to act.

After all it is not as though they are financial advisers; no personal information required here – just an obligation to set the investment strategy for the fund as a whole, by investment option and to act in members best interests (collectively).

But what action are trustees and their investment strategy committees going to take?

The Productivity Commission in its recently released report noted Smart Defaults and the role they are set to play in the industry achieving efficient retirement outcomes – so not a bad place to start looking.

Further in the 26 October 2016 academic CIFR submission to the Commissions 2nd inquiry on default fund selection it was noted:

“Member heterogeneity makes it important to accommodate the ability to tailor and foster the development of smarter defaults. The potential for sub-optimal outcomes increases under ‘one-size-fits-all’ defaults in the presence of heterogeneity. The implication for the review of default arrangements is that care should be taken to engender the scope and incentive for tailoring, including fostering the development of smarter defaults.

In addition, recognising that members are different, many funds are looking for ways to enhance their capability to tailor to members. A key conclusion of the CIFR MySuper research is that there is a need for smarter defaults to address member heterogeneity, especially given that many members accept the default they are offered as a matter of trust.”

This changed mindset will operationally involve two groups – trustee member services and investment teams – working together in a way that traditionally hasn’t occurred, in order to solve in a new way an old problem.

Many of us know that these teams often operate in silos. That on the investment team side they believe it is easier to replicate through derivatives and overlays any outcome desired by the member team. Problem is that this investment approach involves complexity, including actuaries and assumptions, which members just don’t get or trust. It also ignores the member heterogeneity efficiency gains alluded to above and the required trustee business strategy to appeal to members. Without new members, regardless of a funds size, net contributions will turn negative and ultimately the investment team’s role turns to selling rather than buying assets.

So successful funds need to attract (MySuper) members, nudge engagement and build trust with clear effective statements. Taking the easy path doesn’t work. What’s needed is a flexible approach to tailoring members by the existing investment options.

Smart Defaults

In this digital age, why don’t trustees and executives implement tailored investment options for their disengaged MySuper Members? Is it that they currently lack the incentive to be innovative?

So what is this new method that’s being referred to as the next generation Smart Default?

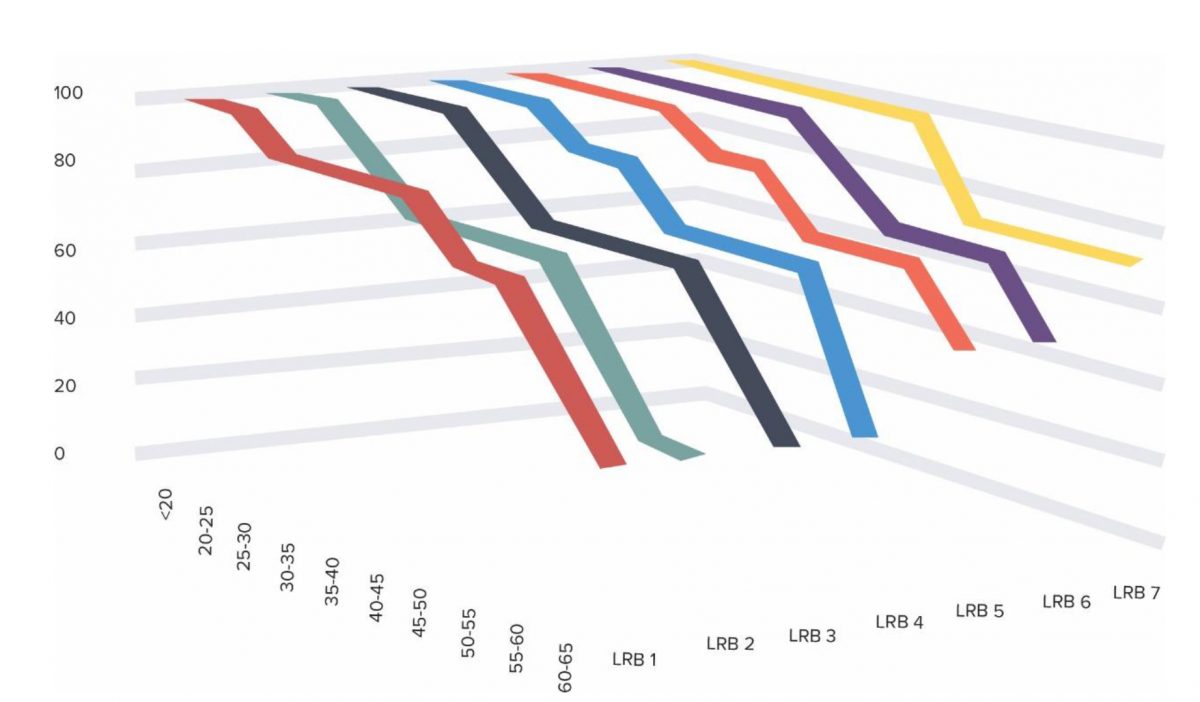

An example is called Trustee Tailored Super. It tailors default members into different streams (lifestyle retirement bands), based on their projected retirement balance (or its derivative retirement income). Then for each of those streams automatically provides different investment options (Glide Paths) based on a members’ age.

It is depicted in the following graph. For example all members with a projected retirement balance, under say $50,000 are placed on the red glide path (LRB1), following that path those aged up to age 25 years are in 100% growth assets (Australian Shares Option), then between 25-45 they step down to 90% growth assets (Aggressive Option) etc. A different glide path applies to LRB2 etc.

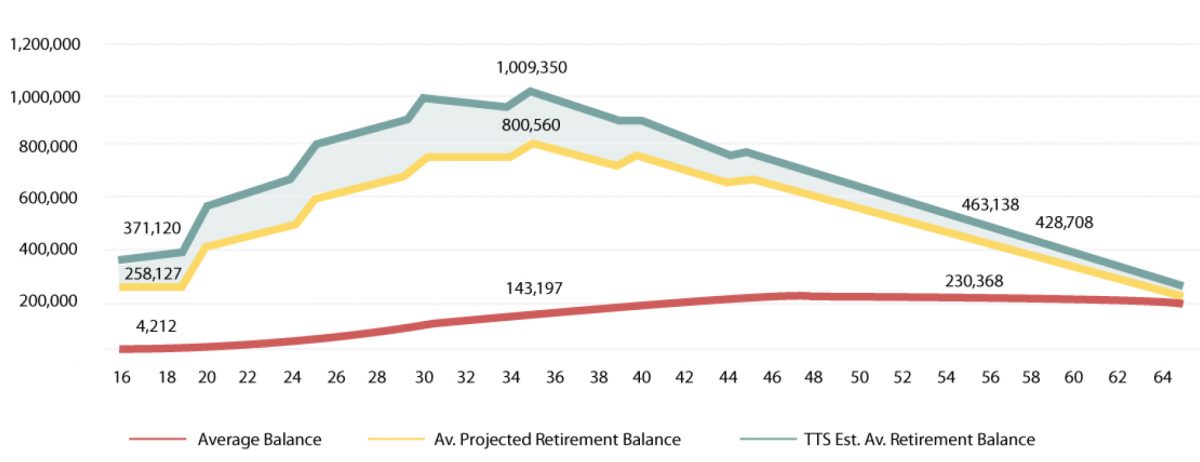

This Smart Default approach is more effective. By tailoring it can leave some MySuper members in higher return investment options for longer, while managing down the risk of loss as retirement approaches for others. Recent and ongoing testing, using funds own MySuper member data and their published investment option return and loss ratios, shows this can achieve an average 1% real per year improvement.As with the familiar ‘Compare the Pair’ adverts, this produces a bigger nest-egg, with an average 35+% improvement in retirement balances over a lifetime. This is depicted in the following graphic, with the improvement being the green shaded area.

As with the familiar ‘Compare the Pair’ adverts, this produces a bigger nest-egg, with an average 35+% improvement in retirement balances over a lifetime. This is depicted in the following graphic, with the improvement being the green shaded area.The numbers on the graph indicate average current balance ($143,197 at age 35 years), average current projected retirement balance ($800,560 per annual statement) and the average projected Smart Default Retirement Balance ($1,009,350).

The numbers on the graph indicate average current balance ($143,197 at age 35 years), average current projected retirement balance ($800,560 per annual statement) and the average projected Smart Default Retirement Balance ($1,009,350).

Furthermore this is a collation, member by member, using the funds own published returns per investment option. It can also be shown as average per lifestyle retirement band (LRB) or for different ages, including those approaching retirement.

Operationally the processes and techniques used replicate current practices and structures.

The same investment options, the same projected retirement balance (or income) as used on member annual statements (new Financial System Inquiry outcome), and bulk automatic investment option switching consistent with age based life-cycling switches (on major birthdays).

So surprise, surprise it’s not that there isn’t a way to use digital and big data technics to improve outcomes, just has occurred in numerous other industries (e.g. tailored medicines).

Class Actions

You would have thought, now that Smart Defaults are a known and with such significant benefits at stake that it is only a matter of time before disgruntled MySuper members take a class action against trustees for not acting.

As pointed out in a 24th February 2017 article Lawyers warn super funds to expect class actions, in instances of operational failure, members have a right to recover their money. This is despite the law recognising a tolerance for investment strategy losses from the development of complex intermediated structures.

“What is not acceptable is risk in the operational process,” Cbus Super general manager, investments legal, Michael Guilday said. “That is where there will be significant opportunity to attack super funds and their structures.”

Squire Patton Boggs partner Amanda Banton is quoted as saying, “based on her experience of class actions against Lehman Brothers, Standard and Poor’s, ABN Amro Bank NV and Local Government Financial Services, Banton said courts did not accept ‘market failure’ as a defence”. The court’s rationale was that even though the probability of market failure was low, it was still a key risk that had to be managed. This means investment operations need to be robust.

Banton added that the top reasons she would sue were if funds made investments that did not fit with the mandate, if due diligence wasn’t done on a specific financial product, and if there were conflicts of interests.

Class actions in response to operational failures are already happening in the public securities space, with 21 open class actions in Australia.

It is certainly reasonable to assume that once the first fund adopts a Smart Default, there will be pressure for others to either follow suit or explain their inaction in better fulfilling their fiduciary responsibility to disengaged members.

Governance

That brings us to governance. Why does the superannuation sector lack to the will to try something new, something that hasn’t been road tested overseas beforehand?

Where is the leadership that is readily apparent in our other industries – both big and small – that have entered to digital age?

What happen to Super? Is it structural?

Is it because:

- Funds are so used to ongoing huge contribution inflows that until now they haven’t needed to compete for members?

- Performance and executive KPI’s so far have been based on investment returns not retirement outcomes (the new objective currently being legislated)?

- Trustee directors are generally part time, arrive with mixed skills from their other careers – be that employer related or member representatives, and while genuinely interested in meeting their fiduciary duties (including to act in members best interests), they are reluctant to rock the boat and take personal reputational risk?

- The advisers, the gatekeepers either are embarrassed that they hadn’t thought of Smart Defaults or because these advisers gave up due to the funds being too slow to adopt?

Well the changes being forced on the industry at present, including mergers, are rapidly altering those dynamics and mindsets. As the AFR, Chanticleer reported on 8 December 2016 in their Selfish and reckless trustees resist industry mergers, article:

“One of the most pressing and least talked about issues in the superannuation industry is the need for scores of smaller funds to merge with each other to protect the interests of members.

Unfortunately this much-needed process is being held back by the personal interests and concerns of super fund trustees who do not want to lose their jobs. This selfish and reckless approach to the governance of compulsory savings vehicles is definitely on the radar of the Australian Prudential Regulation Authority.

In November, Rowell told the annual conference of the Association of Superannuation Funds of Australia that APRA was progressively implementing the revised prudential framework for super. She made it clear that APRA expects much more than just compliance with the prudential standards. Rowell said all trustees should be continuing to lift the bar across all areas of their operations and that doing “just enough” was not good enough in terms of meeting community expectations.”

On the other hand, as the Investor Daily, on 29 November 2016 reported, forcing smaller superannuation funds to merge is unlikely to be in the best interests of members.

“The emphasis on increased scale and mergers as the mechanism to deliver efficiency has been a significant distraction to the determination of what actually drives efficiency and inefficiency in both large and small funds,” said Ms. Mastrippolito NESS Super CEO.

“If the goal of a superannuation fund is to be efficient, rather than subject only small funds to scrutiny, it is our recommendation (to the recently closed Productivity Commission review) that all funds be required to publish an efficiency ratio and, where this ratio exceeds an industry benchmark, be required to justify their use of members’ funds.”

“If it is not scale which drives efficiency, the real issue to be addressed is looking beyond scale to what factors actually drive efficiency and what are the practices that detract from providing value to members that should be stamped out,” said Ms Mastrippolito.

So many funds will be forced to change their current approach, get with the digital age particularly in respect of member attraction and retention policies or merge. Maybe this does involve introducing independent professional directors or other executives that haven’t been captured by the status quo.

Industry Consolidation

The operating environment, namely competition, retirement outcomes and governance focus is changing.

- Competition for members is heating up. A recent report (by Third Horizon) shows 22 funds (20% of the MySuper Funds) have declining market shares and net contribution outflows.

- A few mergers have recently occurred, targeting a 0.15% improvement for members and a 10% consolidation is now considered likely given recent public speculation, including on 2 February 2017 by KPMG head of wealth advisory Paul Howes. He said it was time for APRA to start ramping up pressure on fund mergers because a number of small superannuation funds are continuing to bleed money and lose members.

- APRA has started to apply its legislated MySuper Member Assessment Test (otherwise known as the scale test). On 15 February 2017 APRA’s Helen Rowell stated APRA will force the boards of the nation’s worst superannuation funds out of the industry unless they improve their performance. Underperforming executives and boards will be invited by APRA to discuss their strategy for boosting returns, improving services and lowering costs for members.

- Rowell was also quoted on what is known euphemistically as Principle-Agent capture “At the end of the day I think it all comes back to really honing in and focusing on what’s in the members’ best interests rather than what’s in the interests of the institution itself or the participants in the institution that have gained themselves from it,” Rowell said. Rowell also said default funds and base products should deliver for everyone regardless of the choices they have made.

- ASIC has just started a review of the incentives given to employers by funds to make a fund the default and the Productivity Commission is midway through reviewing both the system for receiving default fund status in industrial awards and MySuper superannuation competitiveness and efficiency.

Competition

That brings us to competition. The hunt by trustees for new differentiated product offerings, that provide member attraction (direct or through default employer status) and retention (from members leaving to another fund or SMSF) strategies, is on.

Reuters on 8 December 2016 reported that Australian fund legalsuper resists ‘pathway to mediocrity’ merger pressure, with Andrew Proebstl, chief executive of the $3 billion fund quoted as stating.

“The problem is that there is a fixation on growth for the sake of growth, which can be a quick pathway to mediocrity. Whether a fund is small, medium or large, it needs to have clarity of purpose and can deliver better value for its members relative to larger super funds.”

Trustees looking for a point of difference – a reason to continue to exist – will find it in their niche member demographic profiles, as has occurred other regulated industries (e.g. credit unions). All the better if these strategies can be readily audited as both outstripping economy of scale merger benefits (circa 0.15%) and more effectively converting contributions into that objective – improved retirement outcomes.

This world of new differentiated product offerings for MySuper trustees is good news for advisers, both those advising members and trustees.

MySuper Member Attraction and Retention Strategies

The member experience graphic below, highlights the role of Smart Defaults in member attraction and retention strategies, plus how it is related to existing member channels (Choice, Age-Only Life-Cycling and One-Size-Fits-All). The green channel on the right describes the experience of members who make their own choices be that selecting an investment option or using a funds or others financial advice models.

Funds expend much of their resources on this element, in addressing the needs of engaged members. In contrast, the needs of disengaged members have been largely ignored, leading to a stark dichotomy compared with the treatment of engaged members.

The red channel describes the standard default offering, which covers around 70% of MySuper members and is reliant on the actions of the trustee. The other 30% of MySuper members are in first generation Age Only Life-cycling (yellow channel) a move that has mainly occurred since 2013 and is a transition step, to further tailoring using Smart Defaults (green channel on right).

These members enter those channels either because their employer has chosen this fund for them (because of its product offering characteristics), due to it being listed in an Industrial Award (method currently under review for change) or because the member has selected the fund but not an Investment Option (e.g. Shares). Regardless effective attraction strategies must deal with this 80% of the membership base – be that via promotion to employers, industrial umpires or direct to employees. Furthermore member retention strategies rely on the same approach.

In other words, it’s time trustees discarded their double standards – offering extensive guidance to choice members about what to do, but not bothering to act in the interest of the remaining 80% MySuper members themselves.

It will require some fund to lead, that fund will most likely be a smaller, more agile fund with more to lose and fewer conflicts. The directors and executive team should be roundly supported and recognised. Perhaps even given an innovation award. In 2016, there was no Superannuation Award for innovation provided by Conexus Financial owing to a paucity of new ideas in the industry.

It is exactly this type of Smart Default enhancement that concentrates on retirement objectives, driven by a competitive environment and open minded governance that is needed and is currently so obviously lacking.

A dynamic and competitive industry, with small and large players, competing to reduce the impending Retirement Funding Shortfall should not be delayed for fear of upsetting currently entrenched special interest groups. The retirement lifestyles of the vast majority fellow citizens are just too important to let that happen. Smart defaults provide the vehicle for Trustees to treat disengaged members in a similar way to engaged members – boosting their prospects of achieving a comfortable retirement lifestyle.

By Douglas Bucknell, GAICD, SA Fin, Managing Director and CEO, Tailored Superannuation Solutions Ltd