Weekly market update – week ending 17 March, 2017

Investment markets and key developments over the past week

Global shares got a boost over the last week from a dovish rate hike from the Fed and relief that the Dutch election saw a rejection of far right Eurosceptics. Reflecting the positive global lead resources shares helped drive the Australian share market higher. Japanese shares slipped though partly in response to a rise in the Yen. The Fed’s dovish hike also saw bond yields and the $US decline which in turn helped commodity prices and the $A.

The Netherlands election highlights yet again that the risk of a Eurozone break up is exaggerated, with Dutch voters turning out in large numbers to support pro-Euro parties. PM Mark Rutte’s Liberal Party won 33 seats in the 150 seat lower house of parliament against Geert Wilders’ Eurosceptic Freedom party only getting 20. While the Liberal Party is down on 41 seats from the 2012 election it will lead negotiations to form a centrist coalition government (which usually takes months) and Rutte will most likely remain PM. This is a blow to the Freedom party which only a few weeks ago looked like it could get more votes than any other party. It’s the third election in the Eurozone in a row since Brexit – Spain, Austria and now the Netherlands – that has seen anti-Euro populists bomb out. The Europeans look to have seen Brexit and Trump and decided that’s not for them! Popular support for the Euro remains high and this is clearly working against populist/nationalist parties and is likely to do so too in the French elections too. This is positive for the Euro and leaves Eurozone shares and peripheral bonds looking attractive.

The Fed hikes but continues to signal that future rate hikes remain conditional on improving growth and inflation and will likely remain gradual. It does not want to do anything to upset the recovery. The median dot plot of Fed officials’ interest rate expectations remained unchanged at three hikes for this year and another three hikes for next year and the Fed continues to expect that future hikes will be “gradual”. This does not mean that the Fed poses no threat. Market expectations still look remarkably complacent and at some point in the next year the focus will shift to the Fed allowing its balance sheet to start running down (by letting bonds roll off as they mature). This all points to a resumption of the bond bear market at some point.

So far share markets are following the pattern of the last twenty years where the initial Fed hike in a tightening cycle causes share market weakness (eg, June 2004, December 2015) but subsequent hikes have little impact as they are seen as consistent with stronger growth and profits, until monetary policy eventually becomes tight. With rates starting much lower and the process being far more gradual this time around we still have a fair way to go before US monetary policy becomes tight enough to threaten the bull market in shares.

Of course the US wasn’t the only country where interest rates were a focus in the last week. The People’s Bank of China increased key money market rates by 0.1% in a continuation of moves seen last month. However, the moves are very minor and look largely to be designed to stop growth from accelerating too far (given the commencement of a large number of infrastructure projects) rather than to slow the economy. The Fed’s move added to the case to move in order to minimise downwards pressure on the Renminbi.

By contrast both the Bank of Japan and Bank of England left monetary policy on hold. In fact the BoJ could be seen as being on autopilot having committed to quantitative easing and keeping the 10 year bond yield at zero until inflation exceeds 2%. So the rest of the world still lags the US by a long way.

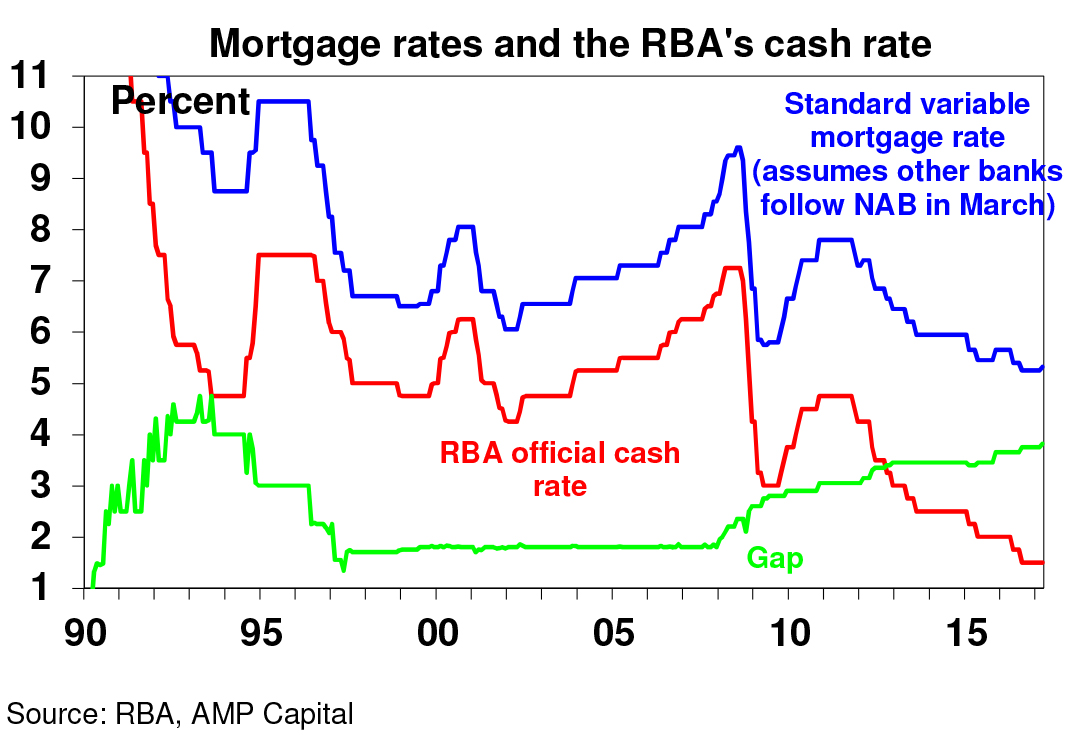

Finally, in Australia the National Australia Bank (maybe hoping to move under cover of the Fed) raised rates for property investors by 0.25% and for owner occupiers by 0.07%. With global funding costs for banks having increased on the back of higher bond yields, out of cycle rate hikes for owner occupiers seemed likely at some point and with NAB moving other banks are likely to follow. But while the move will cause agitation, a 7 basis point hike is unlikely to have much economic impact and like the out of cycle rate hikes seen in November 2015 is likely to be largely ignored by the RBA. That said if banks hike by 25 basis points or more then the RBA may have to consider offsetting it with another cash rate cut. While the NABs move will lead to the usual waffle about whether the RBA still has much influence over lending rates its noteworthy that out of cycle bank moves have been a regular occurrence since the GFC and yet this did not stop mortgage rates falling to record lows in response to RBA rate cuts. Changes in the cash rate remain the main driver of bank mortgage rates.

Major global economic events and implication

Most US data remains strong with small business confidence and regional business conditions indicators remaining robust, the NAHB’s home builders’ conditions index rising to its highest since 2005, housing starts up more than expected and labour market indicators remaining strong. Retail sales were softish though. Core inflation also remained stuck around 2.2% year on year, the same level it’s been around for the last year. Not enough for the Fed to speed up here.

While President Trump’s budget proposals with massive spending cuts to pay for increased defence spending have caused much excitement, Congress drives the budget and will ultimately settle on a massively watered down compromise.

Chinese economic activity data for January/February indicated that solid growth momentum has continued into this year with industrial production and investment accelerating and real retail sales growth remaining strong.

Australian economic events and implications

In Australia two things happened over the last week. First, RBA Assistant Governor Bullock added to the message that more macro prudential measures could be on the way to cool down the Sydney and Melbourne property markets. This could include tougher interest rate tests and a reduction in the 10% growth cap for loans to property investors. Threats to the Sydney and Melbourne property markets are steadily building: state and Federal governments are shifting into gear to improve affordability; another round of macro-prudential measures looks on the way; the banks are starting to raise rates for owner occupiers out of cycle; all at a time when the supply of units is surging; and prices are ridiculous.

Second, economic data was mixed. Business conditions and confidence slipped but remain high according to the NAB business survey. Consumer confidence edged up but remains around average. Jobs fell in February but full time employment rose and leading jobs indicators point to solid jobs growth ahead. A rise in labour underutilisation to 14.6% (ie unemployment plus underemployment) is a concern though.

Five reasons why the RBA won’t hike this year: growth is still sub-par; labour underutilisation remains very high; underlying inflation is at risk of staying below target for longer; banks are raising lending rates out of cycle; and the $A has been going the wrong way. Another round of macro prudential controls to slow housing gives the RBA flexibility on this front. Our view remains no hike until second half 2018.

What to watch over the next week?

In the US, a speech by Fed Chair Yellen (Thursday) will be watched for any more guidance regarding the outlook for monetary policy. On the data front expect to see continued gains in home prices (Wednesday) but a fall back in existing home sales (also Wednesday) and new home sales (Thursday) after strong gains in January, February durable goods orders to show ongoing improvement and the March manufacturing conditions PMI (all Friday) to remain strong.

Eurozone business conditions PMIs for March (Friday) are also likely to remain at strong levels.

In Australia, the minutes from the last RBA Board meeting (Tuesday) are likely to confirm the RBA is comfortably on hold. But most interest will be around comments in relation to lending standards. Speeches by the RBA’s Ellis and Debelle will also be watched for any clues regarding rates and new macro prudential requirements. Expect ABS data to confirm a solid +2% gain in December quarter home prices (Tuesday).

Outlook for markets

Shares remain vulnerable to a short term pull back as investor sentiment towards them is very bullish and a lot of good news has been factored in – but there is a risk that any pullback may not come until seasonal weakness kicks in around May. However, we see share markets trending higher over the next 12 months helped by okay valuations, continuing easy global monetary conditions, fiscal stimulus in the US, some acceleration in global growth and rising profits.

Still low yields and capital losses from a gradual rise in bond yields are likely to see low returns from bonds. They look to be starting their bear market again after a pause in the rise in yields since December.

Commercial property and infrastructure are likely to continue benefitting from the ongoing search for yield, but this demand will wane as bond yields trend higher over the medium term.

National residential property price gains are expected to slow to around 3-4% this year, as the heat comes out of Sydney and Melbourne and rising apartment supply hits.

Cash and bank deposits are likely to continue to provide poor returns, with term deposit rates running around 2.5%.

For the past year the $A has been range bound between $US0.72 and $US0.78 and this may continue for some time yet. At some point this year though, the downtrend in the $A from 2011 is likely to resume as the interest rate differential in favour of Australia narrows (as the Fed hikes 3 or 4 times and the RBA remains on hold).

By Shane Oliver, AMP Capital