The emerging middle class and its implications for global investment

How will the growth of the middle class in emerging markets like China shape the investment environment over coming decades?

In our recent article Young tiger stalks ageing dragon we compared and contrasted India and China in terms of their economic and social development. What was clear from that paper was the exceptional rates of economic growth achieved by both nations over the recent past.

A product of that growth is the emergence of a more affluent middle class within each society. If you add an equally rapidly advancing Indonesia, you have three emerging nations, all with expanding middle classes, with an aggregate population of almost 3 billion, or ~40% of the people on this planet. The growth of the middle class in these three mighty countries will have profound implications for global business opportunities and investment for decades to come.

In this paper, Greg Goodsell, Global Equity Strategist at 4D Infrastructure, looks at how the middle class is expanding, especially in emerging markets, and how this will shape the investment environment over coming decades.

The growth of the middle class[1], especially in emerging markets (EM), is a very important ongoing investment theme. This is because, as individual wealth increases in a country – as reflected by a growing middle class – consumption patterns tend to change towards more services/experience based spending (such as healthcare and travel). Given the potential size of the middle class in EMs this change in spending patterns will have profound implications for global business opportunities and investment for decades to come.

In this paper, we look to bring together some recent research on the growth of the middle class to establish a construct of how the broad global society could look in 10, 20 or 30+ years. We then look to address the question of what that new paradigm might mean for global investment.

1. Sustained economic growth ultimately drives individual wealth creation

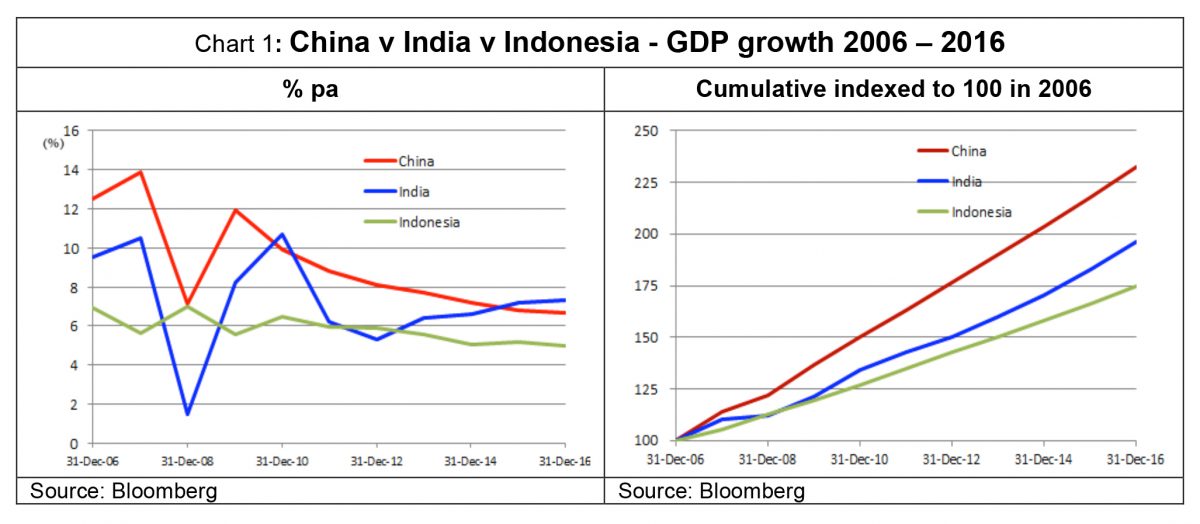

China, India and Indonesia are three of the world’s four most populous nations. All three have experienced strong GDP growth (see Chart 1) which has led to huge economic expansion.

This economic growth has also lead to growth in GDP/capita – a broad measure of individual wealth. While all three countries are coming from very low starting points in terms of personal wealth, a long period of sustained economic growth is beginning to have an impact, with each country’s GDP/capita more than doubling over the past 10 years (see Chart 2 below). A middle class has been established and is growing.

2. But it is still early days in each nation’s evolution of a middle class

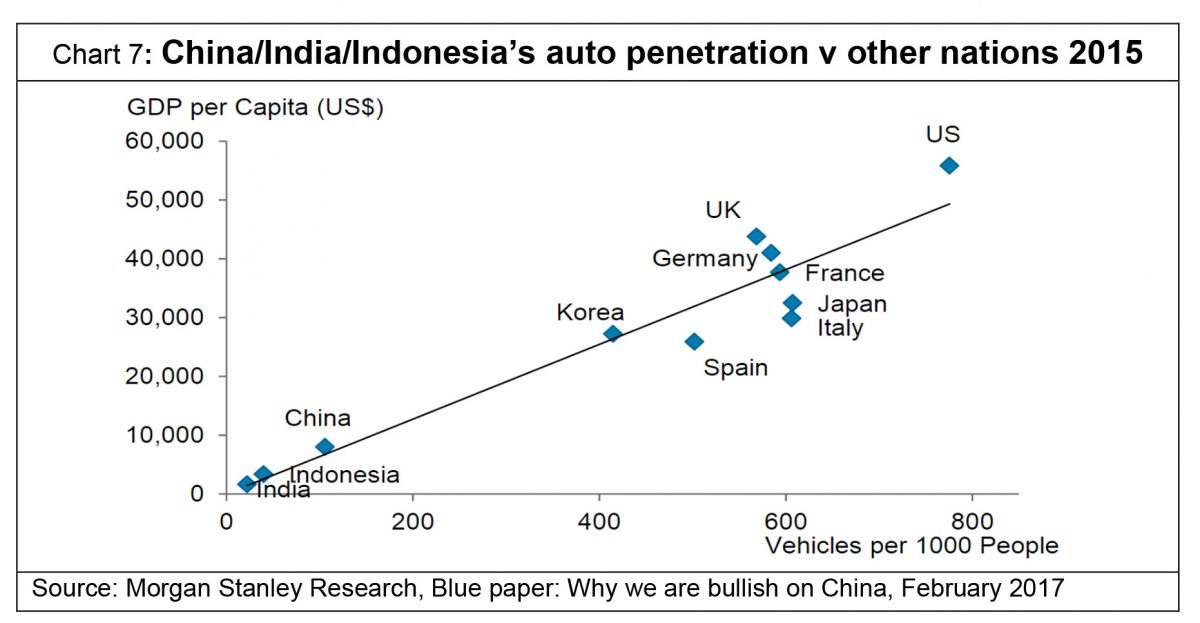

However, even after a decade of sustained GDP growth, China, India and Indonesia are still in the early days of a middle class evolution. This is illustrated in Chart 3 below which shows the relatively low vehicle ownership in each nation. The point here is that the potential for middle class growth in each country remains enormous.

3. What could the Chinese middle class look like in 10 or 20 years’ time?

While the middle class is still evolving in EMs, it is interesting to consider what its profile may look like over coming decades. Focussing on just the main EM – China – some excellent recent research from Morgan Stanley[2] suggests the Chinese middle class consumer could evolve over the next 10 or 20 years to be richer, older, more tech-savvy, and with a significantly different consumption pattern from today (as shown in Chart 4 below).

By 2030, Chinese middle class consumers could have significantly increased disposable income due to ongoing GDP growth, but be older by virtue of China’s deteriorating demographic profile. China’s long standing one-child policy has punched something of a hole in its demographics, which will see a gradual ageing of the population over coming decades.

Increasing internet penetration is a natural adjunct to increased wealth and greater use of computers.

Looking at population wealth segmentation, Morgan Stanley sees China’s society evolving as shown below – income levels increasing, consumption patterns changing.

4. How Chinese consumption could change, and what that would mean for investment?

Growth in the Chinese middle class should lead to increased services and experience driven consumption, with generally less product driven spending as illustrated below.

Overseas and domestic travel to continue to grow

Chart 6 shows that, as disposable income has grown in China, so too has the amount of travel undertaken by Chinese residents, both domestically and overseas. We expect this trend to continue.

Modest level of passports on issue confirms the potential for travel growth

A further reference point for the potential for overseas travel growth is that, at present, just around ~10% of the Chinese population has a passport (and only around ~5% of Indians), and is therefore capable of travelling overseas. This compares with ~50% in the United States or Australia. If incomes continue to grow in China, there are going to be a lot more international Chinese tourists.

Motor vehicle penetration

Chart 7 below shows that there is a natural correlation between growth in GDP per capita and vehicle ownership. China, like India and Indonesia, still has a very low level of vehicle penetration. However, as each nation’s GDP per capita continues to climb, it would be expected that so too will each country’s level of vehicle ownership, so car production can be expected to be strong, as will the demand for new and improved roads.

6. The consequences from this burgeoning middle class for global investment is huge

Clearly, if per capita incomes in China, India and Indonesia et al continue to grow, and a middle class continues to evolve, then global consumption patterns will change. As noted above, these three huge nations account for ~40% of the world’s population so their combined middle class will be a very powerful consumer group. The provision of value adding services, such as IT, education, health and aged care will be in demand. Similarly, travel and recreational services could also gain significant tailwinds, while some more traditional industries such as car production could also boom.

Infrastructure investment, by necessity, will be huge

From an infrastructure investment perspective the potential is enormous. For example, this could include:

- international (and domestic) airports: greatly increased overseas travel leading to demand for new or expanded international airports;

- toll roads: increased motor vehicle penetration will be matched by increased demand for new and enhanced roads, including user-pay toll roads. The data in Chart 7 above tells the potential investment story here: in 2015 China had ~100 cars per 1,000 people, Indonesia ~50 and India ~30. In contrast the US had ~800. As wealth builds, and these numbers increase in EMs, so too will the need for new and better roads;

- port infrastructure: increased import demand will ultimately necessitate enhanced port infrastructure; and

- utility services: more generally, a new more affluent, more demanding middle class will require an improved standard of living across the board which will pressure the basic utility services such as water, electricity, gas and telecommunications to improve their offering.

Governments are cash constrained…. private sector funding essential

Given the budget and balance sheet pressures facing governments around the world, inevitably much of these new and enhanced infrastructure demands will have to be met from private sector funding including the listed and unlisted infrastructure equity markets.

6. But wait… aren’t the middle classes in the US and Germany in decline?

As shown in Chart 8 below, the middle class in both the United States and Germany has been in decline. However, it is important to note that this trend has been underway for some time, and much of the drift out of the middle class has been into the upper-middle and high-income groups.

However, what is significant is that, from an infrastructure perspective, both the US and Germany face huge investment tasks as a result of a long period of under investment in their infrastructure stock.

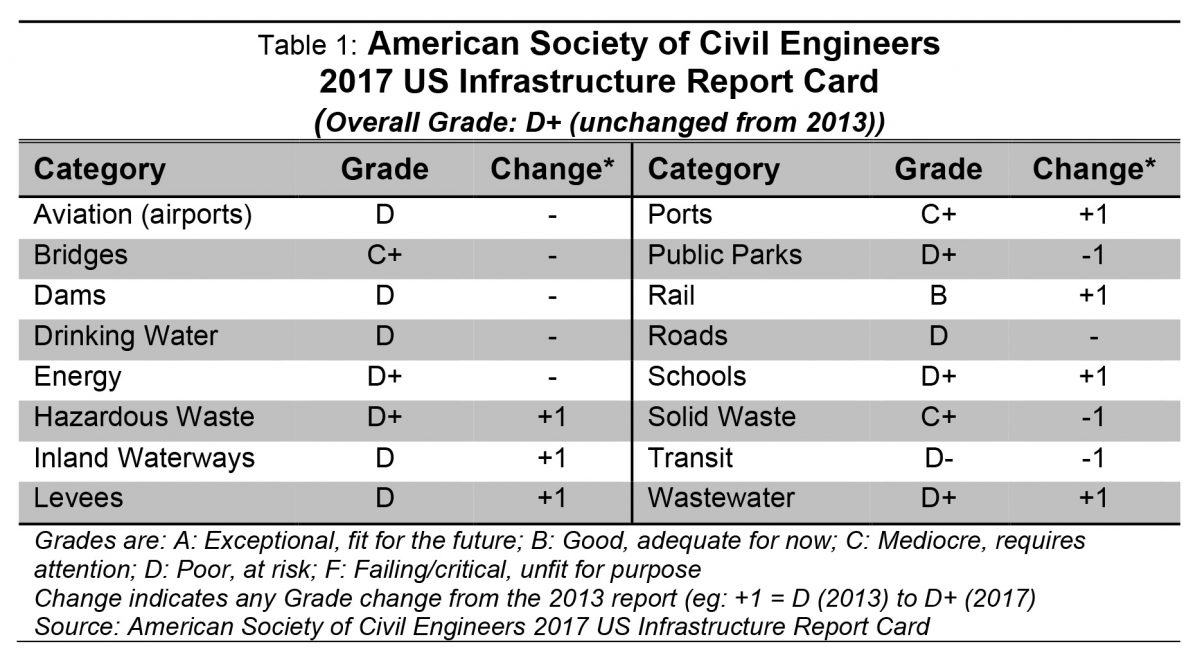

2017 US Infrastructure Report Card: Grade D+

For example, in the US this need for investment is clearly reflected in the 2017 Infrastructure Report Card from the American Society of Civil Engineers (ASCE). The results from the Report Card are summarised in Table 1 below.

The ASCE gave US infrastructure an overall Grade of D+, which was unchanged from the last Report Card in 2013. The highest individual grade was a ‘B’ for Rail, which is largely privately owned, while all the other individual category grades ranged from C+ to D-. Clearly, President Trump’s planned US$1 trillion (~5% of GDP) investment in US infrastructure is urgently needed.

US$300 billion 15-year German infrastructure spend

Similarly in Germany, in August 2016, the government announced a plan to spend €269 billion (US$300 billion, or ~9% of GDP) on construction and modernisation of the country’s infrastructure over the next 15 years. This is reputedly Germany’s largest ever infrastructure investment program. Much work and investment needs to be done in Europe as well.

Conclusion

The evolution of the middle class, especially in emerging markets, will be one of the most enduring investment themes of the next 50 years. Individual consumption patterns in countries such as China, India and Indonesia are set to change dramatically over the coming decades. Inevitably, there will be winners and losers from this transition. However, one constant will be the need for more and improved infrastructure around the world in order to meet the needs of this new, powerful and demanding consumer.

———

[1] The definition of ‘middle class’ can vary significantly but for the purpose of this paper is best thought of in a general sense as the broad social group between the upper and working classes, including professional and business people and their families.

[2] Morgan Stanley Research, Blue paper: Why we are bullish on China, February 2017

———