Benjamin Franklin said that “an investment in knowledge pays the best interest”; however, given prevailing interest rates and the spiralling costs of education, saving enough to fund the educational needs of your clients’ kids or grandkids can be a significant challenge.

Here, Neil Rogan, Head of Investment Bonds for Centuria, looks at the benefits of using investment bonds to invest your client’s savings for educational expenses.

Wouldn’t it be great for your clients to know they had the school fees covered? One less big ticket item to worry about, and the confidence of knowing that they are able to make the best educational choice for their child or grandchild, without being unduly influenced by the price tag.

Education, and particularly private education, can be monumentally expensive. For most Australians, unless they win the lottery, education is ‘pay as you go’…and a constant cost pressure. As returns on savings attract tax, any attempt to save consistently for a long-term goal can feel like one step forward and two steps backward. Super is great from a tax perspective, but it’s not much help if your clients’ children will be starting school before the client is 65!

The true cost of education is surprisingly high

Costs vary enormously depending on the choices made, but you can be sure of one thing – it’s all expensive. According to recent research, parents of a child born today, who has a fully Government funded (public) education, including university, will spend in the order of $200,000 on education. A fully private education, on the other hand, comes in at nearly $700,000. And a mix of the two will be somewhere in between[1]. It’s a lot of money to save, and if your client has more than one child or grandchild to fund, it can be daunting.

It’s important to be realistic

Education is more than simply tuition; the desire of parents to give children a well-rounded education adds to the total cost. An increasing number of parents are concerned that an intense focus on academic excellence in some schools is overshadowing the social and emotional growth of their children, and that children should be more engaged in activities other than academic studies[2].

This means extra-curricular activities, which more and more parents see as crucial to a well-rounded education, but which also incur additional costs. While a realistic estimate of educational costs should include extras such as books, uniforms and stationery, it should also include the costs of extra-curricular activities such as sport, music and dance. Add to that the increasing number of overseas opportunities for kids today – sporting competitions, art tours, music camps and student exchanges – it can add up quickly.

The solution? Encourage your clients to start investing their savings as soon as possible, and choose a tax-effective structure.

Investment bonds – one of the most tax-effective investment structures outside of super.

An investment bond is an insurance policy, with a life insured and a beneficiary; in reality however, it operates like a tax-paid managed fund. And as with a managed fund, you can make recommendations to your client from a broad range of underlying investment portfolios. These typically range from growth oriented assets, such as equities, to defensive assets such as fixed interest. They can also include other asset classes and combinations of assets.

An investment bond has a number of advantages:

Tax effectiveness

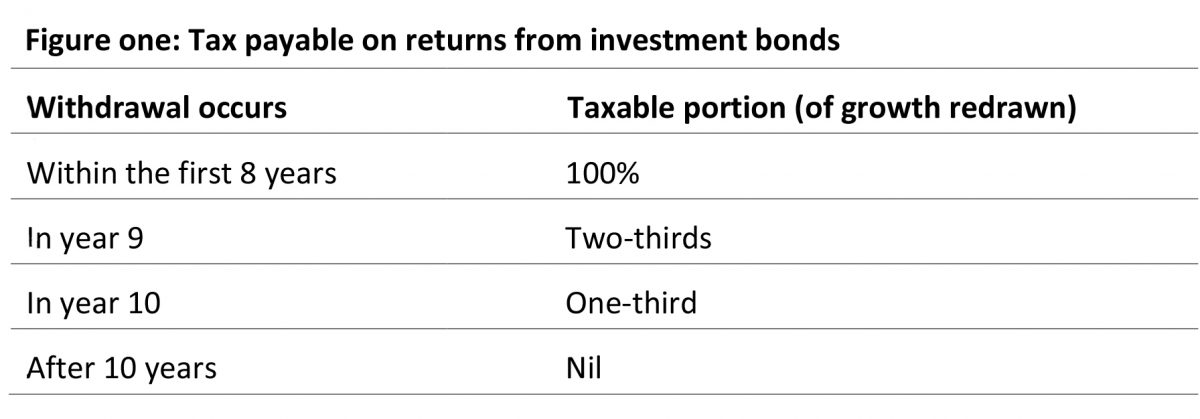

An investment bond is tax-effective because returns from the investment portfolio are taxed at the company tax rate (currently 30%) within the bond structure, and are then re-invested. They are not distributed as income. This means your client does not need to include them in their annual tax return, and as illustrated in Figure one, if the bond is held for 10 years, all funds are distributed with personally tax-free.

If a withdrawal is made within the first ten years:

- The earnings are included in the investor’s personal tax return and

a 30% tax credit applies (as shown in Figure one, a smaller proportion is included for withdrawals in the ninth and tenth year)

- Only the net after-tax income received from an investment bond is taxable

- If the holder of the investment bond dies during the 10-year period, neither the beneficiary nor the estate needs to pay any further tax on proceeds.

In addition, depending on the investments in the underlying portfolio, dividend imputation credits and other credits may apply, making the effective tax rate less than the prevailing company tax rate. This compares very favourably with the top marginal tax rate of up to 49%.

Capital gains tax simplicity

As earnings are automatically reinvested in the bond, reinvestment dates do not need to be tracked for capital gains tax purposes. In addition, the bond holder can switch between investment options without triggering a capital gains tax liability.

Affordability

There is no limit on how much is invested in an investment bond. A client can start with as little as $500 and make additional contributions every year, up to 125% of the previous year’s contribution.

Flexibility

Investment bonds are most tax-effective when held for 10 years or more, but the funds can be withdrawn at any time as required. If the money saved is not in fact needed for education, it can be used for any other purpose.

Ownership and transfer

If a client is saving for a child’s education, the investment can be held in the child’s name, as long as he or she is over the age of 10. This means however, that child will gain full control to decide how to spend the money once he or she reaches age 16.

The preferred option in most cases is to hold the bond in the name of the parent or grandparent. This avoids penalty tax rates for children under 18 if they make withdrawals in the first 10 years, the adult stays in control, and the bond can be started for a child younger than age 10.

This is an option preferred by many grandparents putting money aside for a grandchild’s education. If ownership is transferred to the child, the original start date is retained for tax purposes.

Case study

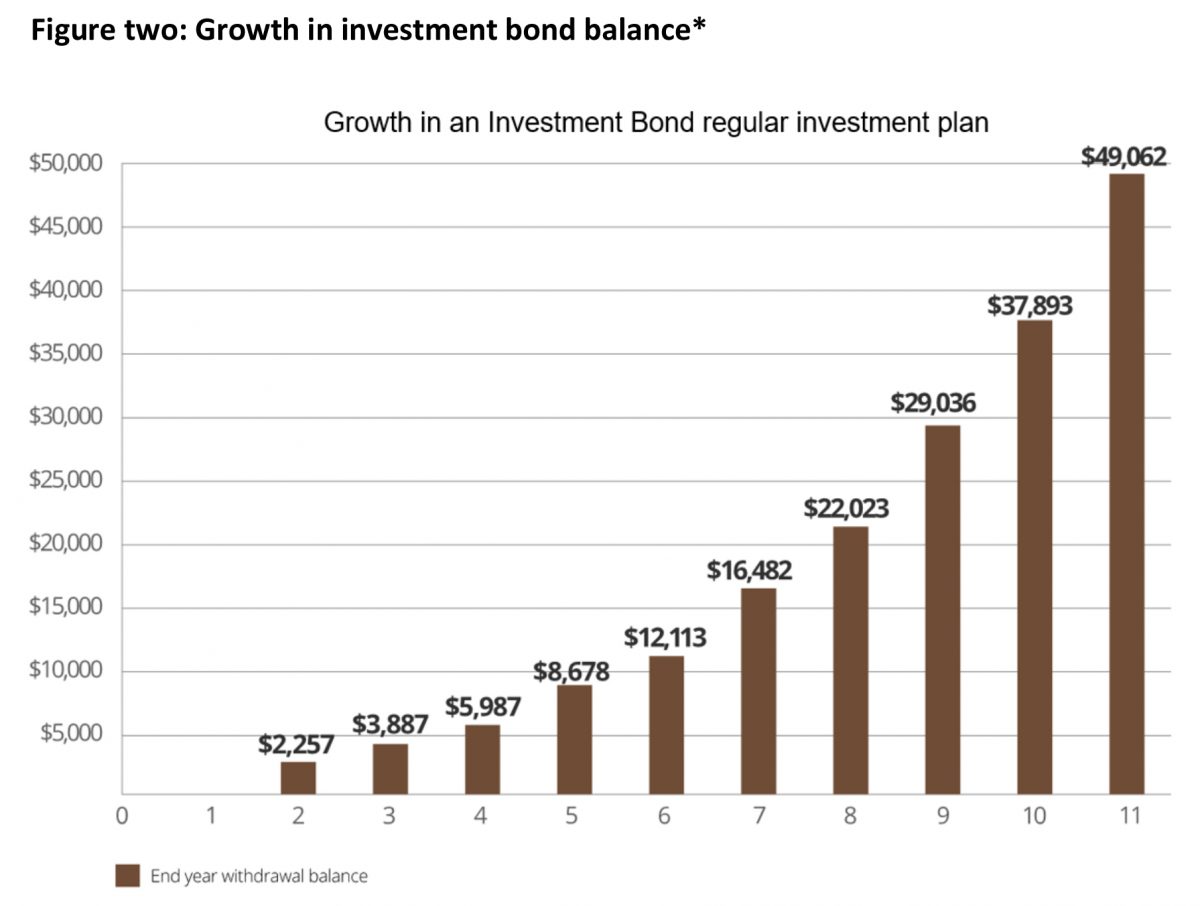

Andrea and Peter recently celebrated the birth of their first child, a son they named Noah. One of first things Andrea did was to put Noah’s name down at the same secondary school Peter had attended; a school he’d loved and that was local to them. Noah’s parent had been reading about the increased cost of education and realised they needed to start saving as early as possible to ensure that the cost of this secondary education wasn’t crippling – particularly as they intended on providing Noah with a sibling or two.

Andrea and Peter, both of whom are on a high personal marginal tax rate, chose to start an investment bond savings plan with $1,000. His grandparents and parents together add $100 each month to the investment bond.

Each year, the regular contribution amount is increased by 25%. Assuming the investment returns 4% income (70% franked) and 3% growth, by the eleventh year, when Noah has nearly completed primary school, there would be more than $49,000, tax paid, to put toward the cost of his education.

* Provided for illustrative example only based on the basic income and growth assumptions described above. This illustrative example does not purport to represent the actual return possible in any of Centuria Investment Bonds. An investment is subject to risk, the degree of which depends on the assets in which the bond invests.

In conclusion

Investing for a child or grandchild’s education may one of the most important challenges in your clients’ financial life. The key to their success will be keeping three things in mind.

- Firstly, investing regularly over the medium to long term can translate into a growing nest egg, and clients benefit from the power of compounding returns.

- Secondly, investment bonds provide many special features for investors seeking a simple tax effective alternative with the objective of building an asset over time.

- Finally, investment bonds are highly attractive investment vehicles for the investment of your client’s savings for the long-term, particularly for those on a higher marginal tax rate.

Remind your clients to start early, invest savings regularly and be realistic about the costs of education. That way, by using an investment bond, they can provide their kids, or grandkids, the education they want without breaking the bank.

———