Fundamentals steady, but investors question reflation story

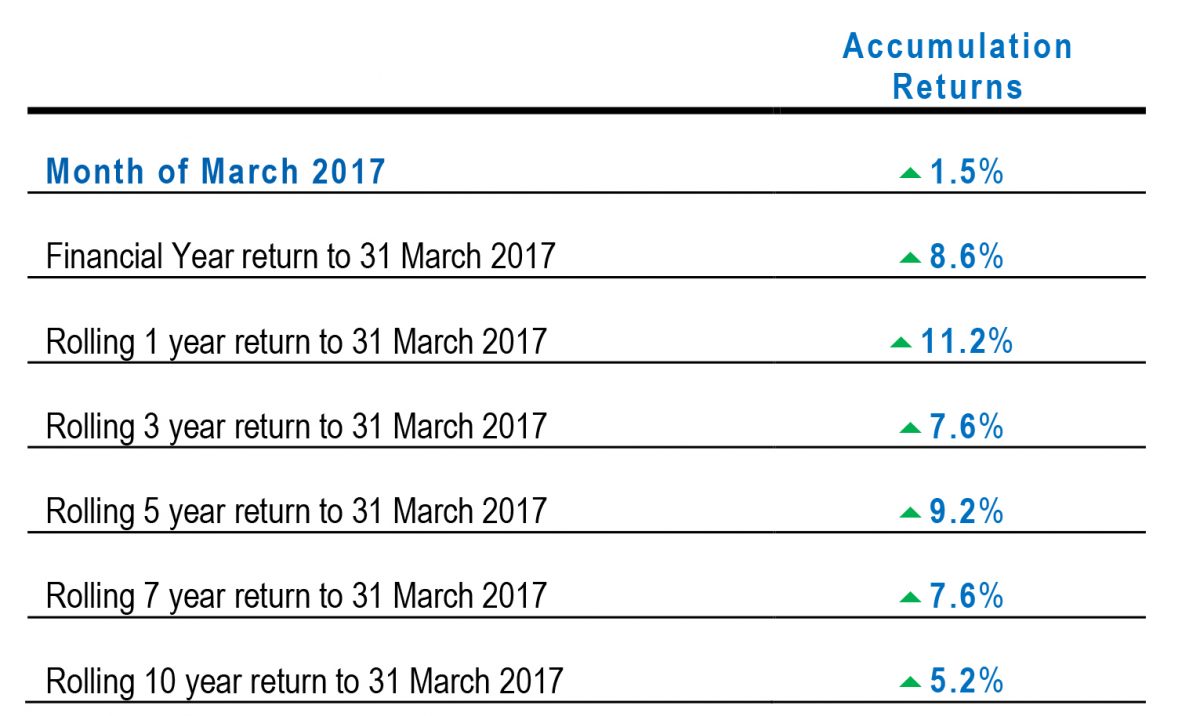

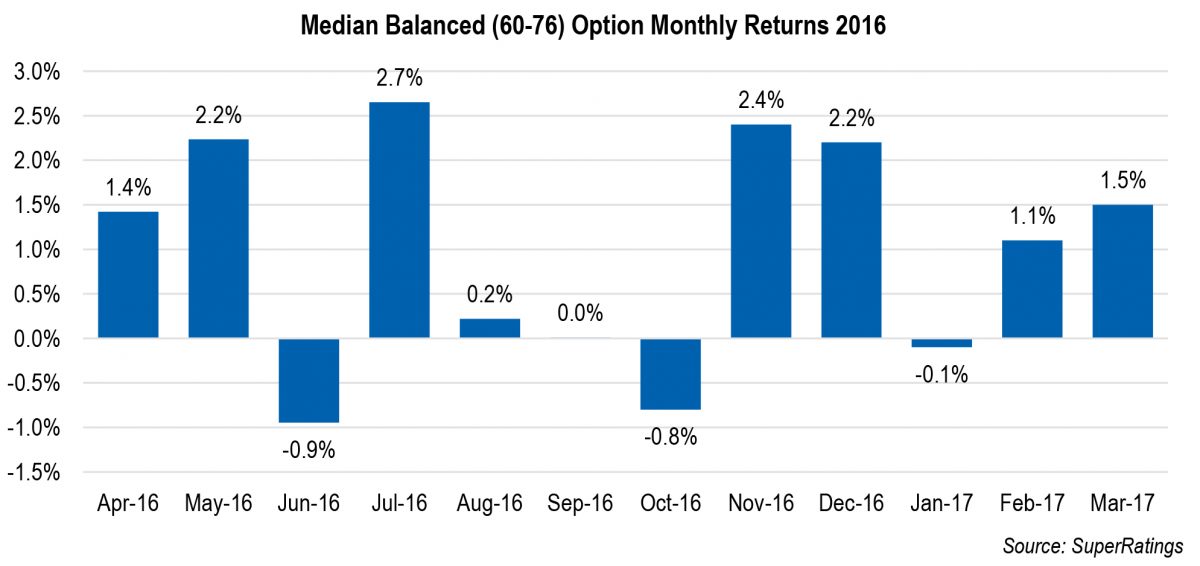

Superannuation fund returns were driven higher in March, boosted by continued gains from the Australian share market. The median balanced option posted a return of 1.5%, while the return for Q1 2017 was 2.5%, weighed down by a small negative return in January.

Global markets have generated strong returns on the back of improving economic fundamentals and consistent signs of inflation, which have generally fed back into Australian shares. Overall, the balance of risk appears to be improving, but while investors have every reason to be upbeat, they should not expect clear skies for the rest of the year.

“The rotation into equities has been a consistent theme since October last year, with yields moving off historic lows and shares pushing ever higher,” said SuperRatings Chairman Jeff Bresnahan. “But we saw the market embracing duration again in late March, indicating that investors are questioning whether the reflation trade is sustainable. In short, the market is not convinced that shares will keep rising in perpetuity.”

Global yields were flat in March, and the US currency came under pressure despite the Fed’s recent rate hike. The failure of the White House to pass its healthcare bill in the US House of Representatives put a dent in the reflation story, with the full implementation of tax cuts and promised infrastructure spending now appearing further from political reality.

On the domestic front, manufacturing activity continues to expand and Australia’s trade surplus remains strong. While iron ore took a big hit in March, the price ended the month above the US $80/t mark.

“The main threats to fundamentals come from the interrelated issues of low wage growth and rising house prices, especially in the Melbourne and Sydney markets,” said Mr Bresnahan. “The RBA has noted that households do not appear to be under stress because of repayments, but we may be due for a correction in these markets.

Australian equities lead the charge

The Australian market powered on through March, returning 3.3% during the month with all sectors gaining. The index delivered

4.8% in Q1 2017, with the 12-month return holding at a non-trivial 20.5%. In March, the Healthcare sector (+5.6%) built on solid gains made through the start of the year, led by Ansell (+13.1%) and Sirtex Medical (+12.2%), which is catching up with the sector after disappointing results in December. Heavyweight CSL (+7.1%) continued to push higher after upgrading its guidance in January.

In the US, markets moved slightly higher, with the S&P 500 Index gaining 0.9% in AUD terms, while the Dow Jones Industrial Index was down 0.3%. While the reflation narrative has been reflected in higher equity prices, the market pulled back midmonth. Information Technology (+3.0%) continued to rise, with shares like Micron Technology (+23.8%) benefiting from a favourable pricing environment, while the Health Care sector was dead flat following Congress’s rejection of the repeal and replace legislation.

Global yields generally also ended flat in March, after some movements higher earlier in the month. While rates have been trending higher since October 2016 and yield curves have steepened, investors appeared to embrace duration again in the latter part of the month, reflected in longer-term fund flows. While recent CPI releases in both Europe and the US have been promising, the numbers have moderated in recent months, and core inflation remains well below central bank targets.

While global conditions have improved, especially in the second half of 2016, and higher commodity prices have boosted Australia’s national income, local labour market conditions are still mixed, with considerable variation in employment outcomes across the country.

Central banks take action

Longer-term returns for super funds continue to sit close to inflation targets, with the seven-year return sitting at 7.6% p.a. (above most funds’ CPI targets). The 10-year return has moved slightly higher to 5.2% p.a., although it remains impacted by the Global Financial Crisis, which occurred nearly ten years ago. The point of maximum monetary stimulus has passed, signalled by the US Fed’s March rate hike, although monetary policy remains very accommodative globally, and quantitative easing measures

in Europe have not yet been tapered. Along with tightening labour market conditions, this could create a more challenging environment for super funds attempting to reach the common CPI + 3.5% target, especially if expansion in yields fails to keep pace. However, steady inflation matched with higher rates of growth would be beneficial for super fund performance.

The monthly returns for the year to 31 March 2017 are noted in the table below:

——–