For many retirees, the family home represents their primary source of personal wealth. For most, paying off the mortgage has been more important than making additional contributions to superannuation, creating the ‘asset rich, cash poor’ generation. This will likely be followed by a generation of retirees who are still paying the mortgage or, in some cases, paying rent.

In this article, DomaCom examines the property trends and their impact on retirees, now and in the future, and examines potential avenues to bring this asset into scope for the development of a new retirement income source, and potential business for financial planners.

Just last week it was announced that Melbourne’s median house price has recorded its strongest quarterly price growth since 2013, crashing through the $800,000 barrier for the first time. The median price increased 7.6 per cent in the first quarter of 2017, to record a high of $826,000, an increase of more than $55,000 on December 2016 figures.

For many Australians approaching, or in, retirement, the commensurate increase in the value of their home represents a boost to their primary source of personal wealth. While the superannuation guarantee has helped reduce the retirement savings gap, ownership of the family home remains the principal wealth accumulation strategy for most Australians. Accumulating superannuation has, and will continue to be, a second-place savings priority compared to extinguishing the mortgage on the family home.

Superannuation – a comfortable lifestyle?

Superannuation assets, in aggregate, amounted to $2.2 trillion as at the 31 December 2016 quarter, an all-time historical record. Despite this growth, the savings priority of home over super has in no small way contributed to the projected average superannuation account balance for Australians aged between 55-64; $321,991 for men and $180,013 for women.[1]

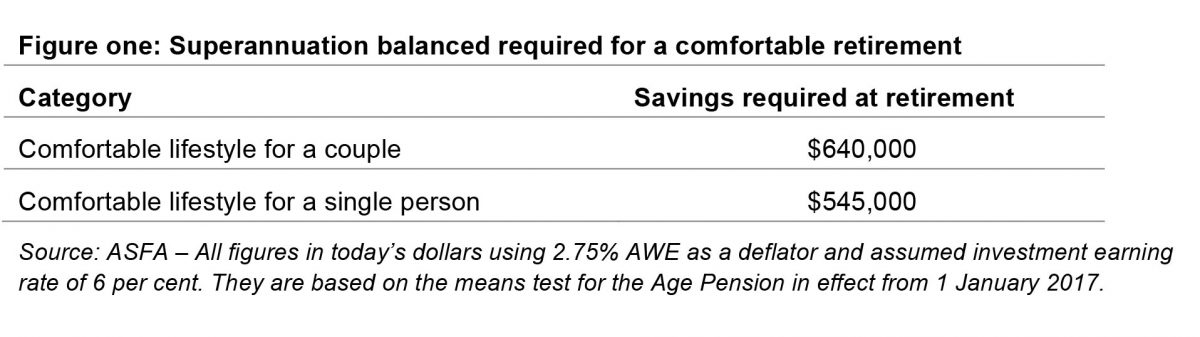

According to ASFA, the following retirement lump sums are required to fund a comfortable retirement, assuming the retiree owns their home outright, draws down all their capital and receives a part Age Pension. These sums are significantly higher than the average balances projected by the ABS.

ASFA defines a comfortable retirement as one where:

“…the retiree can be involved in a broad range of leisure and recreational activities and to have a good standard of living through the purchase of such things as; household goods, private health insurance, a reasonable car, good clothes, a range of electronic equipment, and domestic and occasionally international holiday travel.”

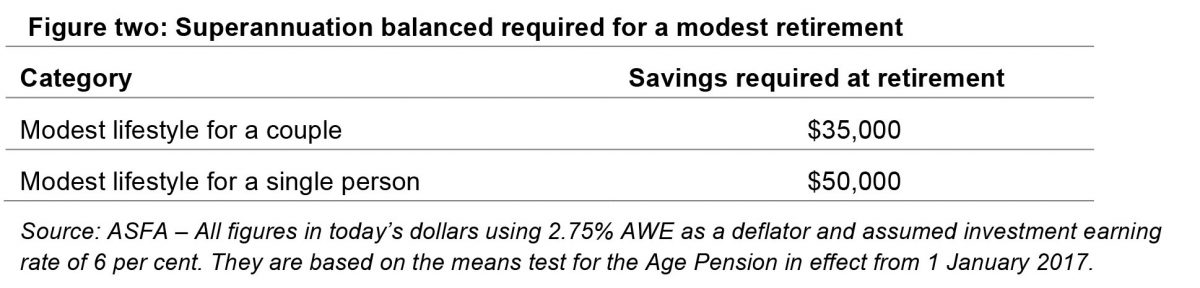

If one can’t have a comfortable retirement, then the step down is what ASFA classifies as a ‘modest’ retirement. The lump sum required for a ‘modest’ retirement is relatively low because the base rate of the Age Pension, plus additional supplements, is sufficient to meet the expenditure required at this budget level…again, assuming the retiree owns their home outright.

As the rate of savings suggests, there will be a considerable lifestyle difference between a modest and comfortable retirement – the former is unlikely to travel, and according to ASFA, will drink cask wine over bottled wine!

Figures three and four, which assume the retiree owns their home outright and is in good health, translate to an annual income as follows:

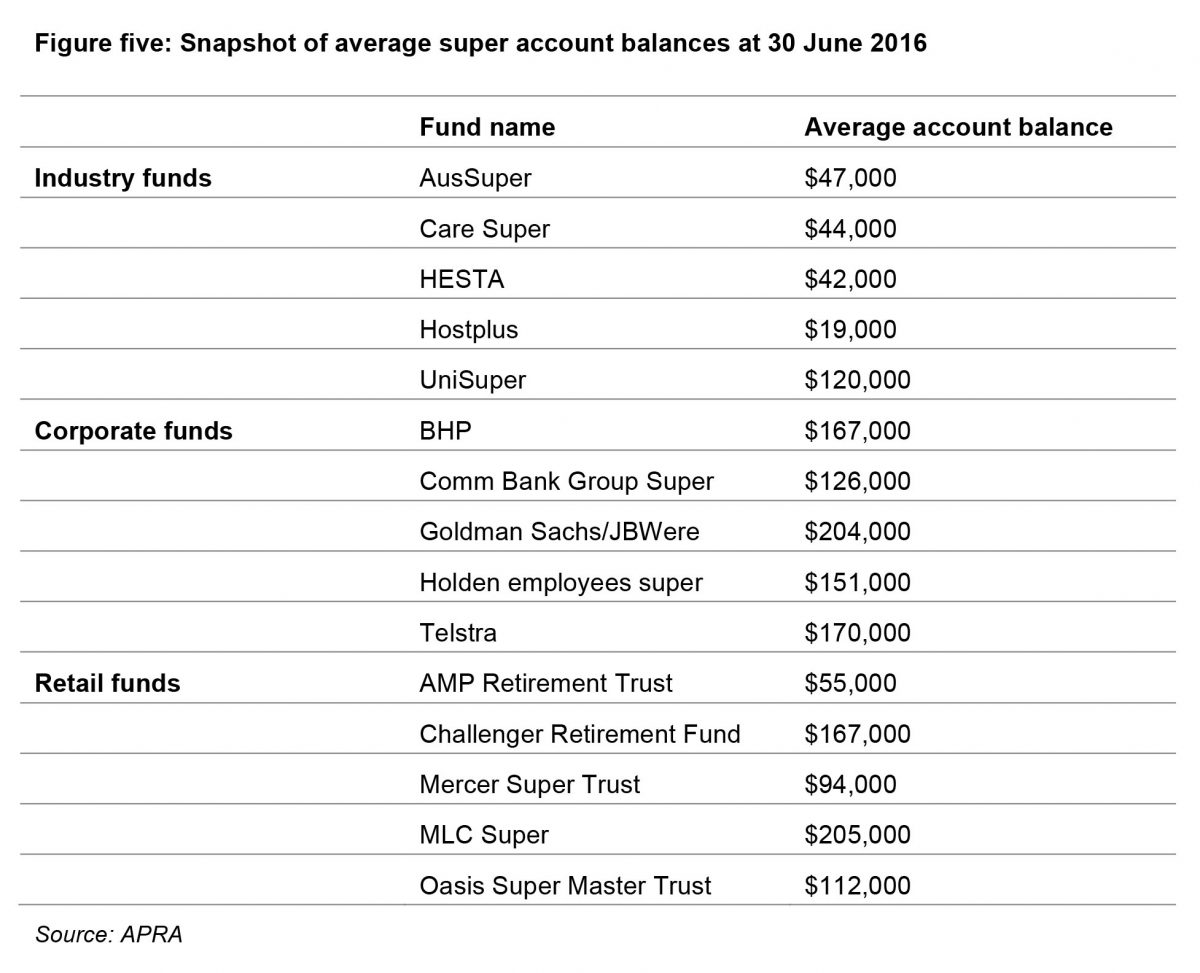

Consider then, some of the average superannuation account balances…are they likely to accumulate the amount required for the lifestyle retirees in for their post-work era? Figure five provides a snapshot of a range of industry, retail and corporate superannuation funds and their average account balance (note: these figures don’t take into account the fact that some people have more than one superannuation account).

According to ASFA’s website superguru.com.au, life expectancy is expected to rise to 91 for males and 93 for females by 2050. Even those retiring today can expect to live for twenty plus years’ post retirement. Will their super savings be enough?

Housing affordability crisis

It’s the political hot potato of the moment, but it has real and potentially long-reaching implications for the next generations of retirees. The modelling by ASFA in figures one to four assumes that the retiree owns their home, outright. What if they don’t?

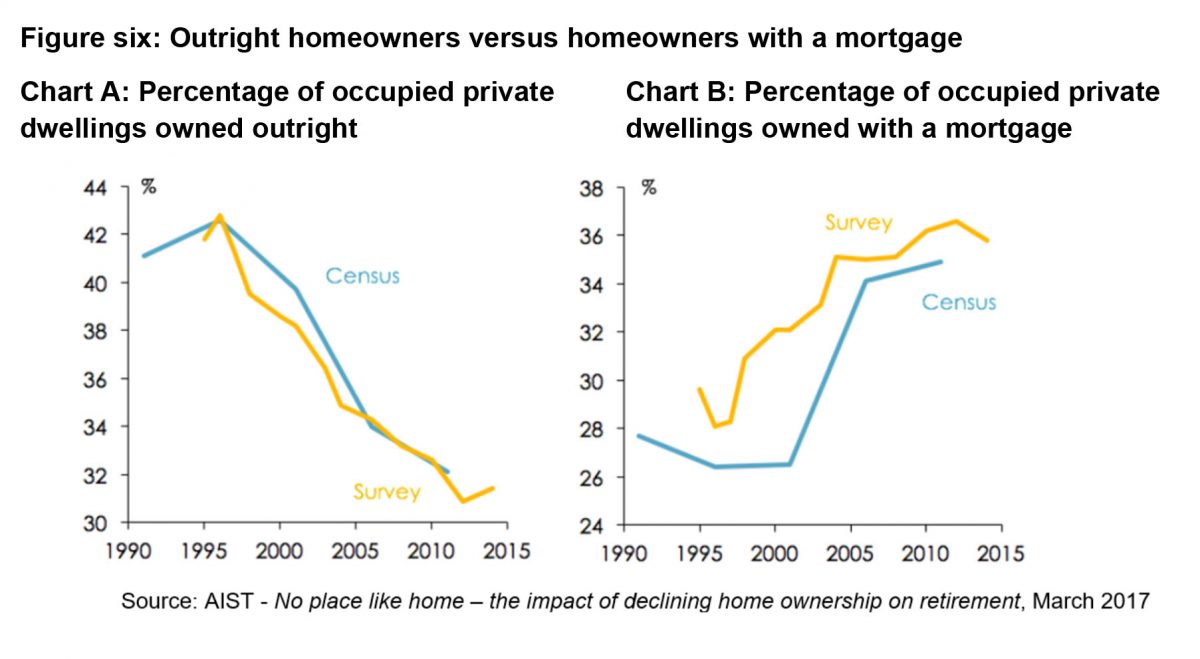

According to an AIST report [2], Australia’s retirement system has taken for granted that retirees will have low housing costs, based on the assumption that mortgages are paid in full or those in lower socio-economic groups will be accommodated in low cost government or social housing. As well as underpinning ASFA’s forecasts, this assumption underlies the government’s setting of Aged Pension rates. As figure six illustrates, the percentage of occupied private dwellings with a mortgage has markedly increased, while those paid in full have decreased.

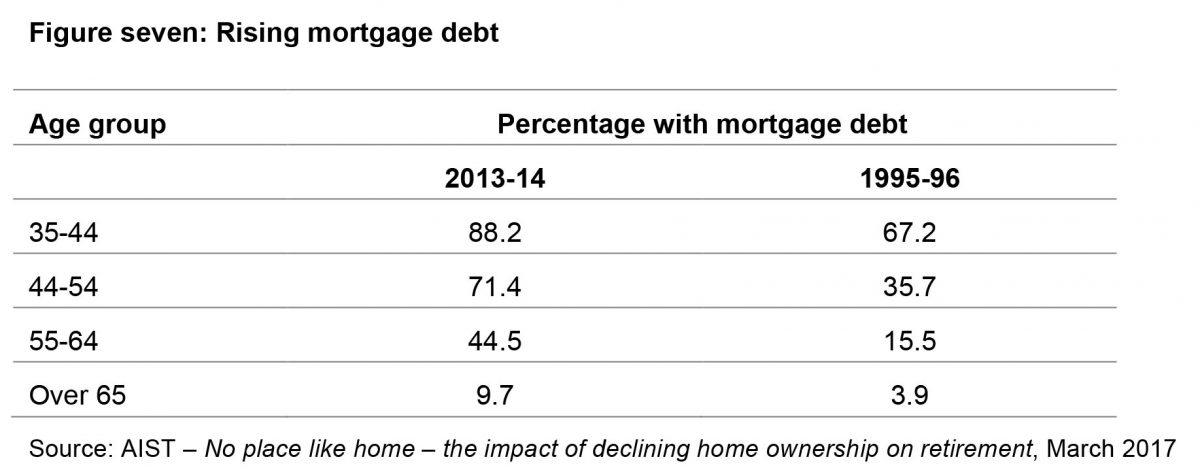

Figure seven shows the change in homes with mortgages across the age groups; most remarkable, the pre-retirement cohort in which home-owner are nearly three times more likely to have a mortgage than in the mid 1990’s. Also noteworthy is the increase in the proportion of over 65s carrying a mortgage into retirement.

Reduced housing affordability is creating two new cohorts of retirees:

- Those still paying down a mortgage at retirement; this group often uses a lump sum superannuation payment at retirement to discharge the mortgage, generating a larger retirement savings gap and, in all likelihood, greater reliance on the Age Pension.

- Long term renters, not eligible for lower cost social housing, who will need to spend a high proportion of retirement income on accommodation costs, again increasing reliance on the Age Pension.

As housing affordability continues to decline, the size of mortgages increase; this results in a greater portion of income being spent on servicing the mortgage. As a result, there is less available to contribute to super, which suggests the retirement savings gap of the future could be greater.

Bridging the retirement savings gap

There are several ways that, with appropriate legislative changes, the retirement savings gap could be closed. With many Australians retiring with a greater amount of wealth embedded in their homes than in superannuation, there is an opportunity for retirees to fund future retirement incomes using the family home.

Hypothetical solution: Equity release to top up super as an undeducted contribution

Home equity release products have been used by retirees to access funds to finance their retirement living costs; this is a trend that DomaCom believes will significantly increase over the coming years.

In the current regulatory environment, when using home equity release, retired Australians have little incentive to use these funds to invest in any current (or new) retirement income products, largely because:

- Retirement income products do not attract concessional tax treatments unless purchased using existing superannuation savings; as outlined, a number of superannuants will retire with too little super to enable them to fund such a purchase.

- There are no incentives for a retiree to use home equity release; it needs to be positioned as a source of wealth that can fund the purchase of a retirement income stream.

The data around superannuation balances, superannuation requirements, mortgages and ongoing housing affordability indicates that many retirees will have insufficient superannuation at retirement to enable them to purchase an expensive retirement income product. If the existing tax-concessional superannuation regime was expanded to include home equity release, it will provide an incentive for many retirees to use the equity in the family home to increase their retirement spending using a pension product, while giving the retiree guaranteed tenure over their home for life. For this to work, alternative retirement income stream products that incorporate home equity release within the superannuation regime are required. While this will not suit every member, or their family circumstances, it could be a strategy to increase a client’s superannuation balance and eventually draw down a tax-free income to supplement the age pension.

While Australians continue to have so much wealth tied up in the family home, super balances may remain lower than the level required for a comfortable retirement; and given this is based on home ownership, the costs of that comfortable retirement are likely to rise! The government needs to consider innovative solutions to enable retirees to maximise the equity in their homes; after all, the alternative is much greater reliance on the Age Pension, which somewhat defeats the purpose of having a compulsory superannuation regime.

[1] ABS 4125.0 – Gender Indicators, Australia, August 2015

[2] No place like home – the impact of declining home ownership on retirement, March 2017

———-