Should we play the ball or the man? How much attention should we pay to who might be selling stocks we are looking to buy or already own?

In general, the anonymity of the stock market prevents us from knowing too much about the sellers. However, there are important instances where we do.

Director and other insider selling

It makes sense that investors should sit up and take notice when those in the know are selling. Directors, CEOs and CFOs invariably know more about their company than outside investors. Any insider selling should thus invite questions over what might be implied.

The last year has seen a number of high profile cases of insider selling that have preceded company problems and steep share price declines. These include at Aconex, Bellamy’s, Brambles, Healthscope, Sirtex Medical, Vita Group and Vocus Communications. It is tempting to conclude that investors should assume the worst upon seeing any insider sales. Academic research[i], and BAEP’s own quantitative analysis, shows that insider selling indeed correlates with subsequent underperformance. However, the extent of this is relatively insignificant, statistically speaking at least. Insider selling is not necessarily a forewarning of troubles ahead. In fact, the ASX specifically warns against assuming as much[ii]. After all, inside selling is quite common. Over the last 12 months, 47 of the companies in the ASX 100 disclosed insider sales[iii]. Of course, not all of these stocks have struggled. In fact, some have been among the past year’s best performers, including those in the table across.

It is said there is only one reason to buy shares, but there are many reasons to sell. Only if the reason denotes something negative of the company’s prospects should investors be concerned. Determining a seller’s reasons, however, is not always easy. Companies will often point to some innocuous reason, such as to fund the purchase of a house. Investors should, however, treat them with scepticism. Never is the reason given that the insider sees troubles ahead, believes the shares are overpriced, or considers now a better time than later to cash out. The surrounding circumstances of the selling are likely to be far more telling.

A Case Study: Ramsay Health Care

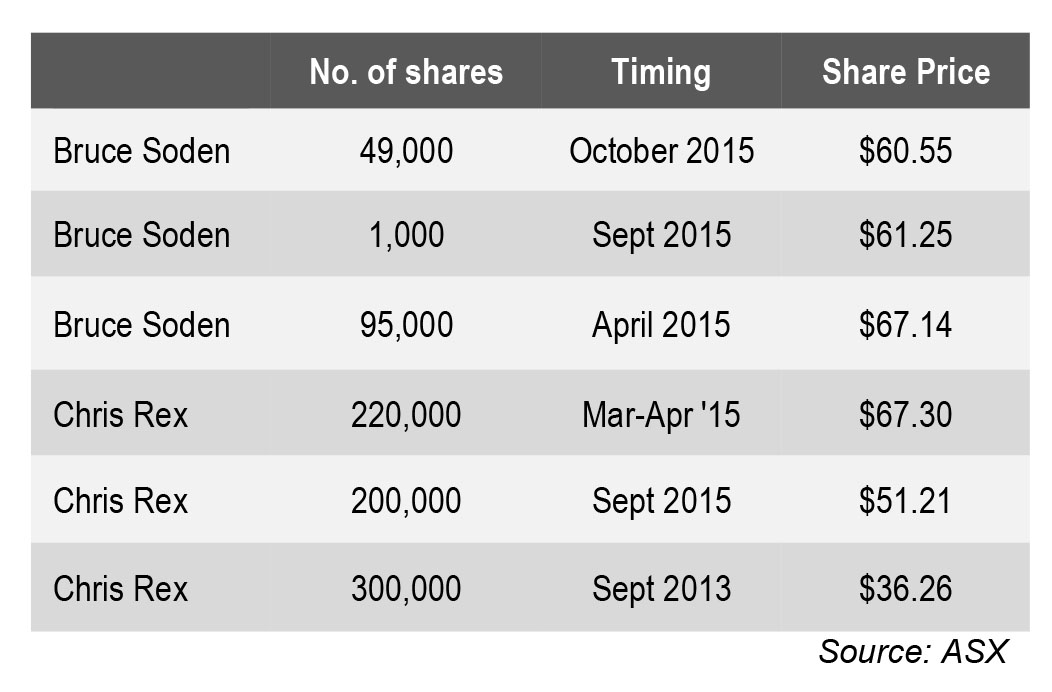

Earlier this year, one of BAEP’s largest holdings, Ramsay Health Care, announced the following significant insider selling on 6 March 2017:

- Chris Rex, the outgoing CEO, sold 400,000 shares at $68.10 per share, with sale proceeds of just over $27 million; and

- Bruce Soden, the CFO, sold 110,000 shares at $68.18 per share, with sale proceeds of $7.5 million.

Following the announcement, the shares traded down about 5% over the subsequent week, to a low of $62.35. We treated the insider selling as a ‘red flag’, something that gave us cause to consider the implications. In doing so, we considered the following factors.

1. The percentage and dollar value of the insider’s shareholding sold/retained

The sales were material, but both still retained significant shareholdings. Mr Rex retained 806,213 shares and 589,181 performance rights (leaving him with more than two-third of his previous holding of ordinary shares). Mr Soden retained 290,791 shares and 254,419 performance rights (leaving him with about three-quarters of his previous holding of ordinary shares).

2. The frequency and extent of previous selling

Both Mr Rex and Mr Soden had previous form in selling material stakes, none of which had preceded troubles for Ramsay.

3. The number of insiders selling around the same time

The more insiders selling, the worse the assumption might be. That both the CEO and CFO were selling was significant. Partly diminishing its significance is that they had sold at similar times before, as shown in the table above, and that there has been minimal other recent insider selling in recent years[iv].

4. Recent share price performance

If a company’s share price has fallen hard, insider selling may confirm troubles ahead[v]; if the shares have been particularly strong, insider selling may imply a view they have become overvalued. Ramsay’s shares were broadly stable in the preceding few months. They had traded higher at around $80 six months earlier, but there was no insider selling at these prices, many other ‘defensive growth’ stocks had also been sold off over that time period, and the company had since upgraded earnings guidance.

5. The timing of the sales, particularly around regulatory change, earnings results, etc.

Two weeks before the insider selling, the company reported a strong first half financial result and upgraded full year earnings guidance. This provided comfort at least on the company’s near-term prospects. However, also at the time, the company announced the intended retirement of the CEO, Chris Rex. He was highly respected, and news of his retirements was inevitably taken negatively by the market. The news of the CEO’s intended retirement clearly added to concerns raised by his selling. As a separate issue, we were able to satisfy ourselves of the reasons for the CEO’s departure, which included discussions with him directly. He had, after all, been CEO of the company for eight years and Chief Operating Officer before that for 13 years. Thus satisfied, we were able to get comfort that the insider selling did not imply anything untoward in the context of recent developments. Indeed, those developments offered a justification for the CEO’s selling. We also noted favourably from a corporate governance viewpoint, that the selling had transacted after news of these developments was released[vi].

6. The stated reasons for the sales

Some reasons given are tenuous and their implication equivocal. These include to diversify (denotes the shares carry risk that needs diversifying from), to provide greater liquidity in the company’s shares (how selfless?), and to fund tax liabilities (possibly only solved by selling shares but it’s impossible to verify). For both Mr Rex and Mr Soden, the later reason was given, specifically, to fund tax liabilities arising from shares they received as part of their remuneration. This is largely unhelpful.

In Mr Rex’s case, it is understandable that he might sell down what is likely his most valuable asset as he nears his retirement and the need to fund it becomes pertinent. As before, his resignation explains his selling. Indeed, the other reason Mr Rex gave for this selling was for “the orderly diversification of his personal investment portfolio following the announcement of his intention to retire”.

7. The company’s future prospects

Based on our research, these continue to look good for Ramsay, with earnings growth supported by a pipeline of high-returning capex projects for hospital expansions, a procurement cost-out program, a retail pharmacy network rollout, and structural industry tailwinds owing to factors such as a growing and ageing population.

On this last point, it is important to realise the extent to which the company’s prospects depend on exogenous factors. For example, selling by an insider at a resource company is less telling given his company’s prospects depend heavily on commodity prices, in respect of which an insider’s view generally carries limited insight.

We were mostly able to get comfort in the insider selling, and accordingly, maintained a position in the company, albeit that it has been reduced. So far, Ramsay’s shares have not moved far from the time of the insider sales. We nevertheless remain vigilant, and willing to change our view if warranted by our continued research and analysis.

The important takeaway is that insider selling is not always a worrying sign. At BAEP, we have over time been invested in a number of stocks that have performed well despite substantial insider selling. A good example is Aristocrat, which is referred to in the table on the first page and whose stock price has risen very strongly.

Initial Public Offerings

Like insiders, the vendors in an IPO typically have an intimate understanding of the company they are selling. This places them at a considerable advantage over new investors. The vendors get to choose the timing of the float, presumably to coincide with when they believe the company looks best and market conditions most receptive. As well, potential investors generally get limited access to historical financials and other information, and limited time in which to assess an investment in the IPO.

On the other hand, the vendors are often trying to sell a large amount of stock, and need to price it favourably enough to encourage sufficient uptake to get the IPO away. In part owing to this, the track-record of IPOs is actually a generally positive one, remembering of course that all listed companies were once IPOs. Undoubtedly, there is a mix of good floats and bad. The trick, of course, is to identify the former. In this respect, investors should gain conviction as they would in respect of a stock already listed. However, it is also worth considering the position of the vendor.

In some IPOs, the vendors are selling their entire shareholding, leaving them with little concern for the company’s success once listed. Here, the vendors will be motivated typically to maximise the IPO price, and caution is required. In other IPOs, the vendors might retain a significant shareholding. Indeed, in some IPOs, it is only the company itself that raises money, achieved through the issue of new shares, with this money directed back into the company itself rather cashing out some or all of the shareholders. In these instances, it is possible to imply confidence on the part of existing shareholders, and an ongoing interest in the company’s future success.

PE-backed IPOs

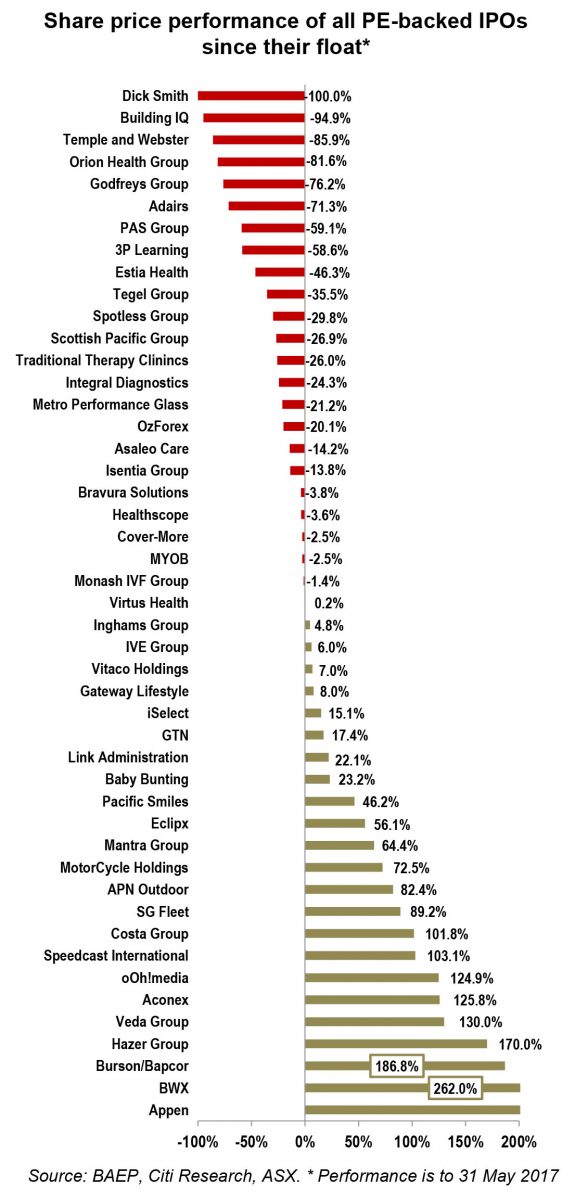

Investors have learnt to take extra caution when it comes to IPOs in which the vendor is a private equity firm. PE firms are purely financial sellers, and unashamedly motivated to maximise investment returns and therefore the IPO price. In some cases, this appears to have led them to dress up the business to look more attractive, for example by reducing costs and capex and providing overly optimistic earnings forecasts. There have been many examples that have gone horribly wrong over the years, including high profile IPOs such as Myer. Owing to examples like this, the markets have increasingly required private equity to retain significant shareholdings, forcing them to own the company’s prospects in the first years of its listed life. In some cases however, this has just delayed the inevitable, with the stock’s performance suffering soon after private equity have sold down their stake once it comes out of escrow. Examples include post-IPO sell-downs at Spotless, Dick Smith, Estia Health, Healthscope and iSentia. In this respect, investors should be conscious of the possibility of a post-IPO private equity sell down, and when that might be.

The reputation of private equity has obviously suffered as a result of some notable disasters. This has recently meant some difficulty in encouraging investors to take up PE-backed IPOs. Some potential IPOs have been pulled, such as Zip Industries, and some have found greater interest via trade sales, such as Alinta Energy. Private equity has an interest in keeping open the IPO route as a viable exit strategy for future investments. A poor reputation will rob them of that opportunity.

The reality is that whilst there have been some disasters, there has also been some big winners. Examples include Seek and Invocare. In fact, the results of PE-backed IPOs are better than commonly perceived. The table on the following page looks at the returns of all PE-backed IPOs since the beginning of the current IPO cycle at the start of 2013. A $1 invested in each of these IPOs would have generated an average return of approximately 31% to the end of May 2017[vii]. Of course, there have been some stinkers like Dick Smith, but there have also been some very healthy returns to make. This recommends against blankly ruling out PE-backed IPOs.

At BAEP, we are admittedly more discerning when it comes to PE-backed IPOs. Even so, we have been able to participate in, and benefit from the success, of the IPOs of MotorCycle Holdings, Eclipx Group, BWX, Bursons, Veda and Mantra Group (some of which we continue to own).

Privatisations

“Whatever the Queen is selling, buy it.”

Peter Lynch, Beating the Street

Certain types of IPOs more consistently offer profitable experiences for investors. One of the best examples is a privatisation, where the Government is selling its wares via an IPO.

There are a number of reasons why it often makes sense to buy whatever the Government is selling:

- naturally, the Government wants to give incoming investors, who are also voters, a happy experience. Privatisations are typically priced accordingly;

- government-backed IPOs tend to be of solid businesses that are industry leaders. Examples include Commonwealth Bank, Aurizon, Telstra, Tabcorp and Medibank;

- government businesses are often bureaucratic, have inefficient cost bases, and lack accountability and entrepreneurism. Once listed, they tend to be run far more profitably, the benefit of which accrues to the new investors. Witness Aurizon’s cost-out programs, and CSL’s ambition in building out a global biopharmaceutical powerhouse; and

- privatisations are not necessarily timed to maximise sale proceeds in market upcycles. Instead, timing is more dependent on the Government’s desire to pay down debt, use the proceeds to invest elsewhere in the economy, or to deregulate industries.

Reflecting these factors, privatisations are generally relatively low-risk and nice returning IPOs to look out for.

Conclusion

The takeaway is that we should not necessarily fear who takes the other side of a trade we are on. This is so even when buying from a director or CEO, or from a private equity firm as part of an IPO or post-IPO sell-down. It should however focus the mind, leading one to understand the reasons for their selling, and to reconfirm one’s own conviction in the company’s prospects. In this respect, research is one’s best defence.

———