Investors spend a lifetime saving and building their wealth. Without an effective and up-to-date estate planning solution, families can face a range consequences upon the death of a parent.

This article from Centuria looks at how the changes to superannuation, which come into effect 1 July 2017, will impact estate planning, and considers strategies to ensure your clients’ plans are effective.

An estate plan defines how an investor wants their assets to be managed during their lifetime, and importantly, how they want them disbursed after death. The plan also deals with the weighty decision as to who will look after your clients’ estate.

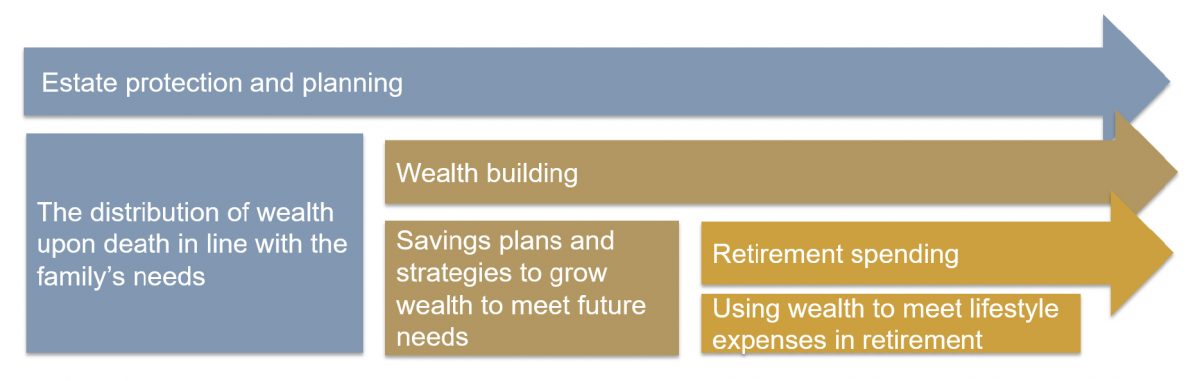

Estate planning should be considered early in the financial planning process. As illustrated, the phases of the financial planning and estate planning processes overlap. For example, wealth building plays a significant role throughout retirement to help manage longevity and inflation risks.

Poor estate planning can have a significant impact on the value of the estate and the beneficiaries:

- The estate could be distributed to unintended beneficiaries

- High legal fees could be incurred to collect all the assets

- Any disputes can result in lengthy delays in accessing estate proceeds

- Erosion of wealth due to tax implications, reducing the value of the estate

Such consequences can result from having no estate plan, or when estate protection and planning is considered as the final phase, once investment decisions have been made.

How will the impending changes impact estate planning?

There are several changes that can potentially impact estate planning:

1. The transfer balance cap of $1.6 million on retirement balances

Effective from 1 July 2017, an individual will be able to transfer only $1.6 million into retirement phase accounts. For the small number of Australians with a balance of more than $1.6 million in a retirement phase account now, they will need to withdraw the excess balance or revert it to accumulation phase, where it will be subject to 15% earning tax.

The upcoming changes not only limits the amount a person can have in their superannuation retirement pension account, but also limits the amount a member can receive from their deceased spouse’s pension account. This is because the deceased’s pension will now count towards the surviving spouse’s transfer balance cap.

2. Changes to concessional and non-concessional contribution caps from

There are three main changes:

- A reduction in concessional (pre-tax) contributions from $30,000 to $25,000

- Higher concessional caps for the over 50s will not exist after July 2017

- The annual non-concessional (after-tax) contributions cap has been cut to $100,000; it is only possible for investors to make non-concessional contributions if their super balance is less than $1.6 million.

3. Lowering of the income threshold from $300,000 to $250,000 for 30% rather than 15% tax on contributions

This means that any Australian with an income of $250,000 p.a. or more will pay 30%, double the usual tax rate of 15%, on contributions into super.

4. The tax-exemption for transition to retirement pensions (TRIP) will be removed

The upshot of this change is that super fund earnings supporting a transition to retirement pension will no longer be tax-exempt.

These changes will particularly impact higher net worth individuals, and seriously curtail the ability to contribute lump sums into super in the future. Finding an effective wealth building vehicle that also provides estate protection and estate planning opportunities is important.

How can investment bonds help in estate planning?

An investment bond is an insurance policy, with a life insured and a beneficiary; however, it operates like a tax-paid managed fund. And as with a managed fund, you can make recommendations to your client from a broad range of underlying investment portfolios. These typically range from growth oriented assets, such as equities, to defensive assets such as fixed interest. They can also include other asset classes and combinations of assets.

Importantly for estate planning, an investment bond is a tax effective structure. Like superannuation, tax is paid within the investment bond rather than personally by the investor. The maximum tax paid on the earnings and capital gains within an investment bond is 30%, although franking credits and tax deductions can reduce this effective tax rate. This makes them an attractive investment option for high income earners.

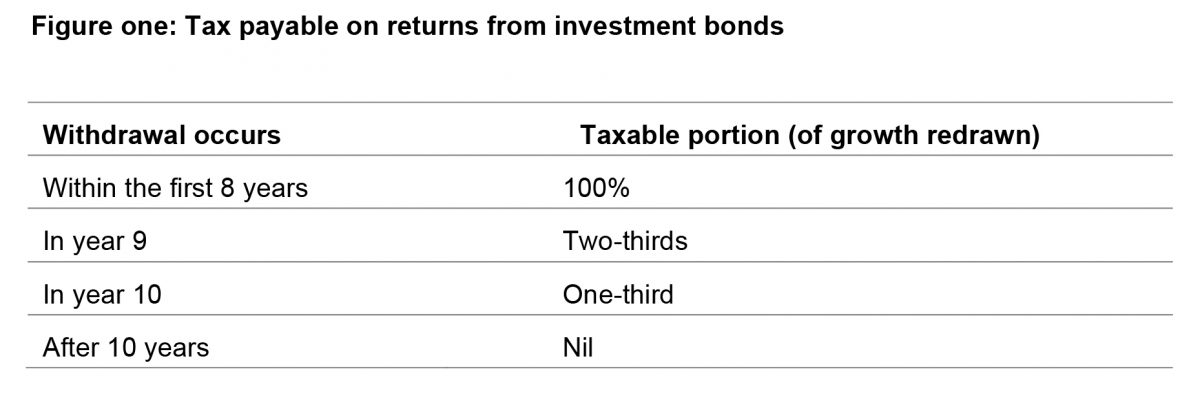

A key feature of investment bonds is that if the investment is held for 10 years, no personal tax is paid by the investor. However, if the investment is redeemed within the first 10 years, the investor will pay tax on the assessable portion of growth as shown in figure one.

For those concerned with estate planning, investment bonds are structured to allow investors create certainty with respect to their wishes regarding passing on wealth. Investors can nominate beneficiaries who then receive benefits directly and free of personal income tax liability.

There are several benefits that make investment bonds an ideal tool for estate planning.

No limit on investment amount

The contribution caps will limit the amount of contributions that can be made to superannuation, however there is no limit on the amount that can be invested to establish an investment bond. Investors can make subsequent investments up to maximum of 125% of the previous year’s contribution without restarting the ten-year period. Investors can choose to start a new investment bond if higher amounts are to be subsequently invested.

Investment bonds can provide a tax effective means of investing and avoid excess contributions tax that may otherwise apply in the case of superannuation contributions post 1 July 2017.

Transfer of ownership

The ownership of the investment bond can be easily assigned or transferred at any time. The original start date is retained for tax purposes. This may not be achieved within a company structure without creating tax liabilities.

Beneficiaries

Investment bonds provide investors with freedom to nominate anyone as a beneficiary in the event of their death. They fall outside of the estate, so are not distributed according to the will, nor are they affected if the owner dies intestate.

Paid tax-free to nominated beneficiary/ies

Investment bonds are paid tax-free to the nominated beneficiary/ies. Depending on the age and life stage of the beneficiary/ies, the funds can then be:

- Reinvested in a new investment bond

- Transferred into the recipient’s retirement phase superannuation account, as long as it will not exceed the $1.6 million transfer balance cap

- Used to make additional superannuation contributions up to the recipient’s relevant contributions cap.

Investment bonds versus other investments

An investment bond may provide greater simplicity and control over death benefits than other investment products such as unit trusts, shares or term deposits.

Upon death, most investment products form part of the estate and may be caught up in any actions taken against the estate. It is also left to the executor to make decisions about the distribution in accordance with the terms of the will.

These actions usually cannot be undertaken until probate or letters of administration are obtained, which means the entire process can take months or even years if the estate is complicated or being disputed.

Once distributions are made, tax may be payable by either the estate (if assets are sold) or the beneficiary when assets that are received in-specie from the estate are subsequently sold.

In contrast, the death benefits from an investment bond can be directed to a nominated beneficiary. Investment proceeds are paid tax-free to dependant and non-dependant beneficiaries, regardless of how long the investment has been held.

Building wealth in an investment bond may reduce the risk of disputes over estates and enable the benefits to be paid more quickly. The advantages of an investment bond in an estate protection and planning strategy are summarised in figure two.

Case study – a blended family

Joan (68) and Brian (73) are married, for both it is their second marriage and each have children from their first marriage; Joan has four children and Brian has two.

Joan’s main estate planning issue is to leave her non-superannuation assets, accumulated during her first marriage, to her four children. She considers investing her non-super assets into an investment bond, with her four children as beneficiaries.

Joan remains the owner and life insured, and because investment bonds provide the flexibility to withdraw funds at any time, she continues to have access to them if necessary. If Joan is alive when the bonds mature, she can reinvest them for a further ten years, knowing that upon her death, the funds are paid tax free to the beneficiaries, her four children.

Estate planning is a critical component of the financial planning process. A sound plan will define how an investor wants their assets to be owned, managed and preserved during their lifetime and, importantly, how they want them disbursed after their death. The different treatment of assets upon death can materially affect a surviving spouse’s superannuation accounts under the new regime, and have a serious impact on the tax liabilities of beneficiaries. The unique features of investment bonds make them worthy of consideration when estate planning for your clients.