Although the Australian options market as we know it commenced operations in February 1976, options of some form have been around for many hundreds of years. However, new margining requirements will potentially impact the future of options trading in Australia. In this article, OpenMarkets examines options trading – past, present and future.

The Australian Options Market (AOM) was established by the Sydney Stock Exchange on 3 February 1976 and provided the first marketplace for exchange traded options outside the United States. The first options were traded over four stocks – BHP, CSR, Western Mining and Woodside-Burmah Oil. In the US, while an over the counter (OTC) options market had existed for 100 years prior, exchange traded options were introduced in 1973 with the establishment of the Chicago Board of Exchange (CBOE) and the Options Clearing Corporation.

Options…from vanilla to exotic

Vanilla options and strategies

Many brokers hold level one derivatives accreditation, which allows them to advise on and implement basic option positions. They can:

- Sell options to close out a position

- Buy and sell warrants

- Exercise warrants and options

- Write covered call options.

These are non-margined options – in other words, there is no additional margining requirement throughout the life of the option. A set value is charged, paid for upfront.

Correctly managed option strategies can be very useful for share investors, particularly those managing their retirement money via an SMSF. There are strategies such as covered call writing that can earn an investor additional income from a ‘lazy’ share portfolio, or the purchase of puts to protect the value of a share portfolio in the event of a market downturn.

Covered calls and buy-write strategies

In a covered call, an investor holds a long position in an asset and writes (sells) call options on that same asset, usually over an equivalent number of shares.

To illustrate, an investor wishes to implement a covered call on 1000 NAB shares. Those shares must be paid for, settled, and in the client’s portfolio. That parcel of 1000 shares is then lodged with ASX Clear and must maintain a 1:1 relationship with the call options – i.e. there can only be 1000, or fewer call options, purchased.

The system automatically rejects a trade that is not covered by an owned security.

Similarly, a buy-write strategy is where an investor simultaneously buys shares and writes a call option contract over an equivalent number of shares. Slightly different strategies, with the same outcome – the investor can earn additional income from pocketing an unexercised premium, can earn income from the dividend, and the premium can balance out a fall in the value of the underlying shareholding.

Selling covered call options can help offset downside risk, but it also means the investor trades the cash received from the option premium for any upside gains beyond the current value of the share until option expiry.

The strategy of buying shares and writing options is an eligible strategy for SMSFs, as long as it is allowed for in the Fund’s investment strategy.

Although these strategies can be used in any market condition, they are typically used when an investor believes a company’s market value will not move significantly over the life of the call option.

The investor generally has two goals: firstly, to generate income from the dividends paid by the underlying shares, and secondly, to provide some protection against a decline in underlying share value. Accordingly, a covered call or buy-write strategy can be expected to underperform in a bull market, and outperform in both flat and bear markets.

Protective put strategy

The buyer of a put option has the right (but not the obligation) to sell a stock at a set price until the contract expires. Where an investor owns an underlying share or other security, a protective put strategy involves purchasing put options, on a share-for-share basis, on the same security.

A protective put strategy protects against losses from a decline in the value of the underlying share, but importantly, allows for capital appreciation if the share increases in value.

In other words, if the share price rises, the investor benefits (less the cost of the put options), and if the share price falls, the put increases in value to offset losses.

An investor employing a protective put strategy may have unrealised gains on their shares and is concerned about short term risks. Purchasing puts while holding shares is generally considered a bullish strategy because ultimately the shareholder would like to see their shares appreciate, even though the put option would then be worthless on expiry. In effect, the put option acts as an insurance policy against a fall in the value of a security.

A protective put strategy is often used by investors with margin lending accounts where a fall in the price of securities in the portfolio could trigger a margin call.

Exotic options strategies

In the case of the more exotic naked option, which requires level two derivatives accreditation, the investor does not own any, or enough, of the underlying security to act as protection against adverse price movements.

Using the earlier example, if the options holder did not own the NAB shares and the market moved against them, they’d be required to purchase the shares regardless of price. If the investor had sold a naked call option on the NAB shares, it carries unlimited risk. While that might not seem significant on 1,000 NAB shares, consider naked calls on more speculative stocks and larger parcel sizes.

While it’s possible to mathematically calculate the risk involved with a naked sold put, where the largest risk is the stock price falling to zero, there is no risk matrix or mathematical solution to measure risk for the naked sold call.

The changing Australian landscape

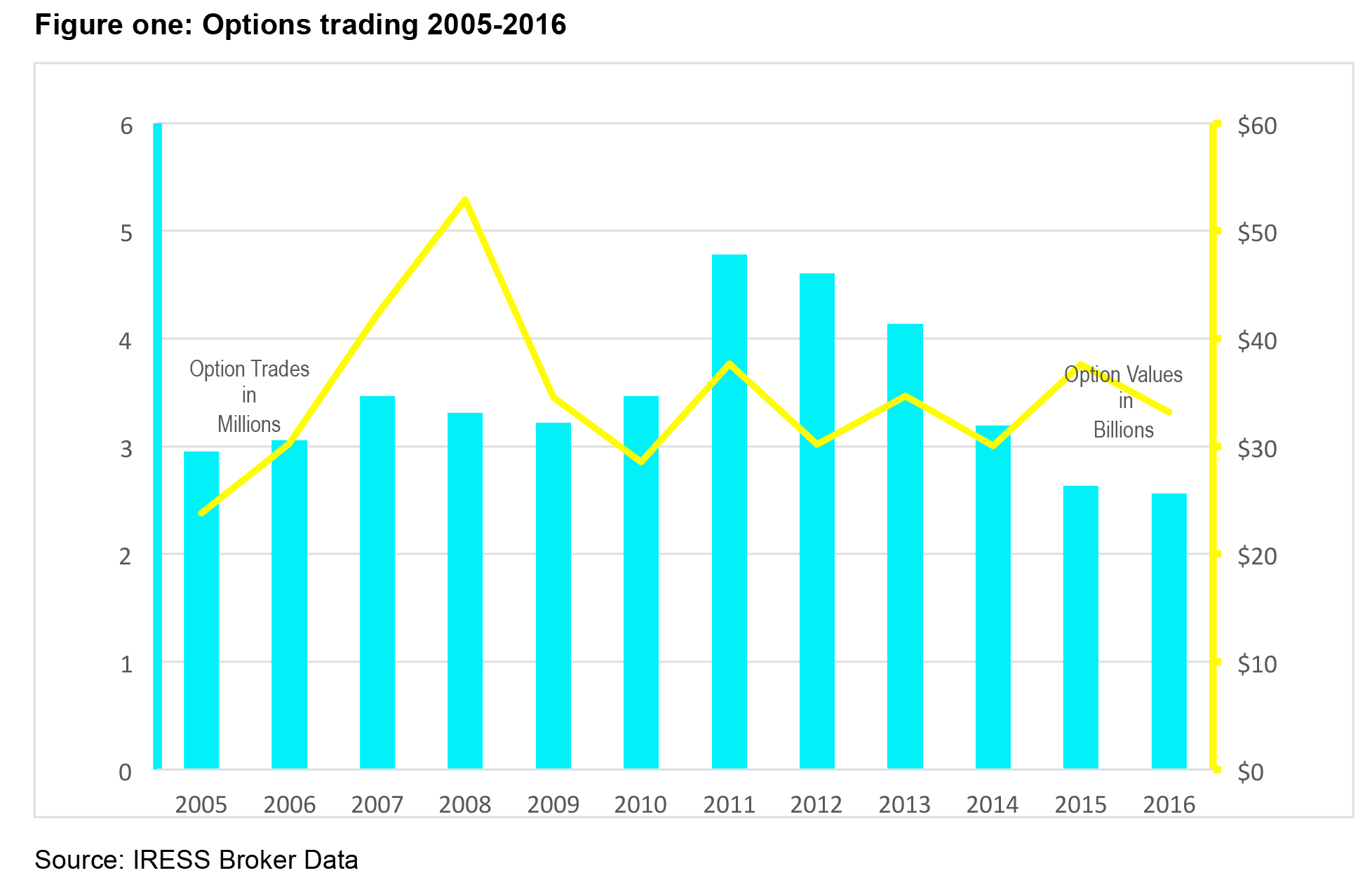

Anecdotal evidence suggests that options trading in Australia is on the wane; this is supported by the data presented in figure one, which shows that both the number of trades and the value of options traded has declined. The value of options traded peaked during the GFC, while the volume peaked in 2011, just post the GFC.

Since that time, several brokers have dropped their level two options trading business due to risk and collateral requirements; it seems the ASX move to the global standard CME SPAN Margining (SPAN) to calculate collateral requirements has had a significant impact. It has dramatically increased some collateral requirements, particularly for riskier options strategies, making them less attractive to brokers and other market participants.

New margining requirements

A margin is an amount, calculated by ASX Clear, that is required to cover the risk of financial loss on an options contract due to an adverse market movement. Simple options strategies, such as a covered call, don’t require margining because the stock is lodged as collateral. At the other end of the scale, how can a margin be calculated for a strategy with unlimited loss potential?

Australia’s margining system was changed in December 2012. SPAN is considered to be the industry standard for portfolio risk assessment, and is the official margin mechanism for more than 50 registered exchanges, clearing organisations, and other agencies worldwide. According to the CME Group website:

“SPAN evaluates overall portfolio risk by calculating the worst possible loss that a portfolio of derivative and physical instruments might reasonably incur over a specified time period (typically one trading day). This is done by computing the gains and losses the portfolio would incur under different market conditions.”

In other words, margining is based on worst case scenarios; for many exotic options strategies, this increased margining requirements and reduced the attractiveness of offering such strategies for several market participants.

Brokers pull out of options

In March 2017, Pershing announced its plan to de-risk its business; it will no longer deal in or clear trades involving naked options. Pershing clears trades for a number of Australia’s brokers, so this has ramifications for each of them.

Other players have also pulled back from the risker end of the options market; in late 2015, Morgan Stanley stopped dealing with naked and unhedged option positions. Major options market makers Tibra and Optiver exited the Australia derivatives market a few years ago, citing lack of profitability of their respective businesses. Market makers play an essential role in options trading; they ensure traders can price and trade options by always being available to buy or sell as required.

Over the past few years derivatives and market making trading costs have increased. This increased cost of doing business, coupled with the risks associated with more exotic option strategies, has made such strategies a less attractive proposition for some broking houses.

Although there appear to be a range of obstacles that make options trading a little more challenging in the current environment, the basic tenets that make some option strategies a valuable portfolio management tool remain in play. It may be harder to implement strategies using more exotic option strategies, although given the risks inherent therein, these should remain the domain of the experts.

———-

This article provides general information only and has been prepared without taking account the objectives, financial situation or needs of individuals. The information contained in this article reflects, as of the date of publication, the views of OpenMarkets Australia Limited ABN 38 090 472 012 AFSL 246705 (OpenMarkets) and sources believed by OpenMarkets to be reliable. We do not represent that this information is accurate and complete, and it should not be relied upon as such. Any opinions expressed in this material reflect our judgment at this date, are subject to change and should not be relied upon as the basis of your investment decisions. All reasonable care has been taken in producing the information set out in this article however subsequent changes in circumstances may occur at any time and may impact on the accuracy of the information. Neither OpenMarkets, its related bodies nor associates gives any warranty nor makes any representation nor accepts responsibility for the accuracy or completeness of the information contained in this article. Past performance is not a reliable indicator of future performance. Investing involves risk including loss of capital invested. ©2017 OpenMarkets Australia Limited.