Developments in Australian equities and the expansion of the LIC sector

What are the past, present and future trends in Australian equities and the LIC sector.

In the first of a two-part series on LICs, Ross Barker, Managing Director of Australian Foundation Investment Company (AFIC), will look at trends – past, present and future – in Australian equities and the LIC sector.

The first in the series will review developments in Australian equities and the expansion of LICs, and second part will provide an outlook for future trends and performance of the market.

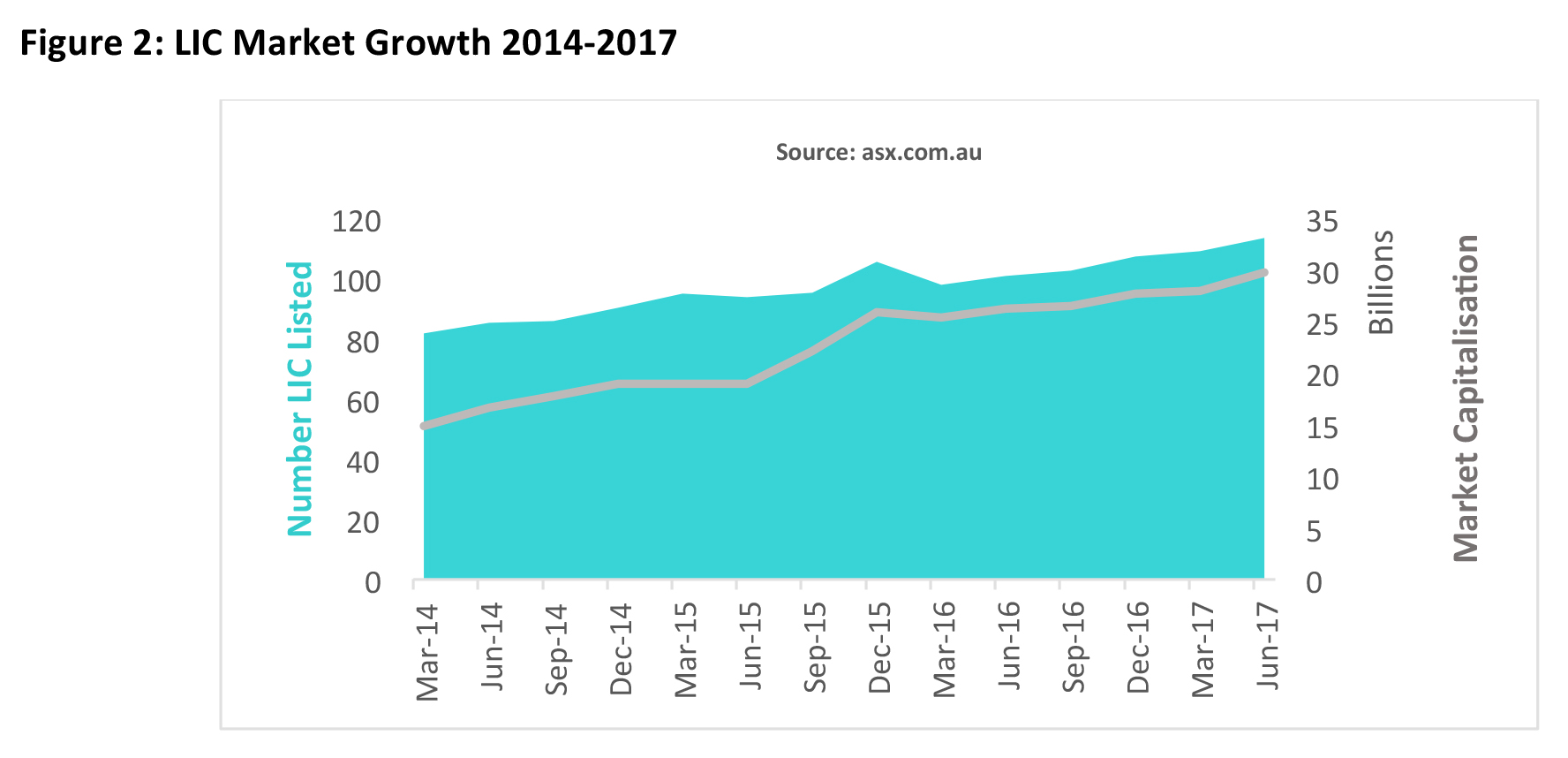

Although Listed Investment Companies (LICs) have been trading on the Australian Stock Exchange (ASX) for nearly a century, the sector is one of the great success stories of the ASX as investors continue to chase income in the new post-Global Financial Crisis environment characterised by very low interest rates and slower growth in many global economies.

As at 30 June 2017[1], the market capitalisation for the sector has nearly surpassed $33 billion and in the last three years over $3.2 billion has been raised from LIC IPOs alone. The sector is continuing its growth trajectory and is expected to expand further as additional fund management groups seek to tap into demand, particularly from self-managed superfunds via the ASX. A look back at trends shaping Australian equities in the last decade will provide a perspective on why the LIC sector remains a popular option for investors.

Australian equities market: the past decade

The Global Financial Crisis

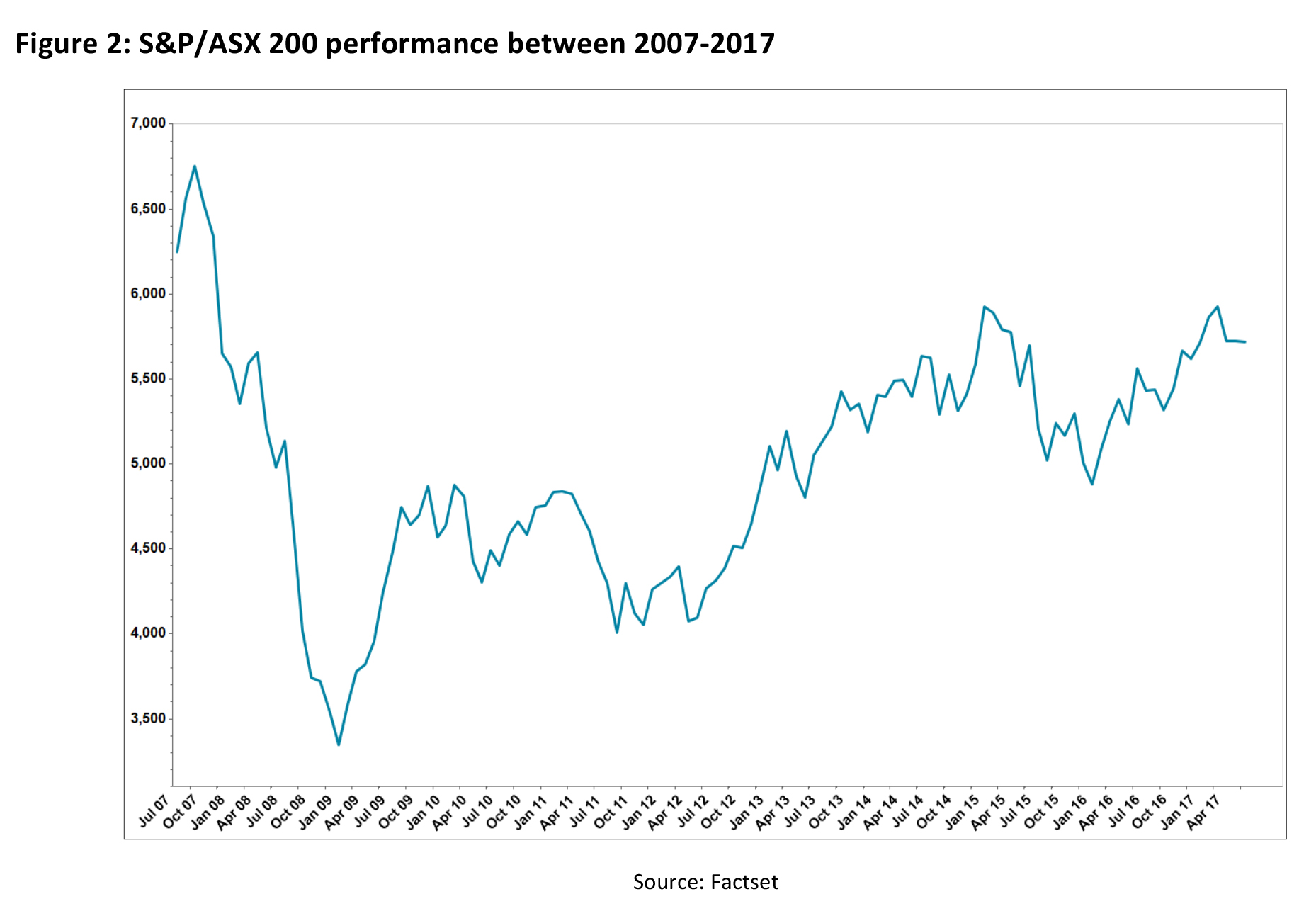

The severity of the Global Financial Crisis (GFC) caused by the United States (U.S.) real estate bubble in 2007 led to sharp declines in stock market indices in the U.S. and across global financial markets.

Over the crisis period (July 2008-May 2009), the U.S. equity market lost about 40 per cent of its market capitalisation compared to the total market capitalisation of ASX-listed companies which fell by 19 per cent to $1.2 trillion in the same period[2].

While the U.S. economy continued to struggle despite the introduction of quantitative easing by the U.S. Federal Reserve, the Australian economy was buoyed by the resources demand from China which improved Australia’s terms of trade significantly. Australia also followed the U.S. lead in reducing official interest rates which contributed to the fall in the Australian dollar and improved the competitiveness of Australia’s manufacturers and services exports and imports[3].

By 2010, the Australian economy had marked nearly two decades without a recession and by 2013, the Australian equity market had started its recovery, delivering close to 20 per cent total return for investors. This trend of low cash rates and term-deposit rates has further contributed to the recovery of the equity market, making it increasingly appealing to investors seeking income returns.

Today: Market performance across sectors

In the decade since the GFC, markets and economies have had to adjust to a new norm of low economic growth, low interest rates and the challenge provided to many businesses from technology disruption.

With the market capitalisation of Australian equities at around $1.5 trillion[4], companies are responding to external pressures and focusing on cost-cutting measures to grow profits as revenue growth becomes more difficult to achieve. Low wages growth and reduced consumer confidence also makes for more subdued revenue for many consumer-focused businesses.

A look at specific sectors

Resources: Lower commodity prices have created headwinds for resource companies although those with lower costs and world-class assets such as BHP and Rio Tinto are better placed. More recently slightly higher prices have improved their position.

Energy: Lower oil prices and previous large capital expenditure on LNG projects has impacted the balance sheet and performance of Origin Energy and Santos. Woodside Petroleum and Oil Search are probably better placed given existing projects, their relative low cost position and access to capital. In the future, the energy sector may face significant challenges with emerging technologies, the shift to greater use of renewable energy, as well as accommodating disruptors such as the development of electric cars.

Banking: The big four banks, Commonwealth Bank of Australia, National Australia Bank, Westpac Banking Group and Australia and New Zealand Banking Group, have performed relatively well following the GFC as the banking sector market share consolidated in favour of the major banks given their better access to funding. Going forward increased competition, increased capital requirements and low growth in the Australian economy may provide headwinds for this sector.

Large retailers: Increased disruption and competition, particularly with the arrival of Amazon, may impact the retail sector. Already, the performance of larger grocery retailers including Coles and Woolworths is being disrupted by retailers including Aldi and Costco. Additionally, Amazon’s e-commerce model may signal a shift in consumer purchasing behavior which may put pressure on the ability of retail property trust sector to attract tenants at appropriate rents.

Telecommunications: The roll-out of the National Broadband Network (NBN) and increasing competition from smaller telco players offering competitive plans is impacting on incumbent, less agile organisations such as Telstra as the ‘grab’ for customers continues.

Property: The strong performance of the REITs over the last few years has been driven by low interest rates, attracting investors to this sector for yield-based security and high returning interest rate proxies. The sector’s performance was slightly weaker this year and will be influenced by the outlook for interest rates.

Health: Australia’s ageing population has buoyed the healthcare sector and while further growth is expected, returns will be dependent on several factors including the ability of the Government to provide funding support.

Technology: Established technology disruptors such as realestate.com, carsales.com and Seek have challenged the position of incumbent companies and have been successful in taking significant market share. As new business models emerge from the use of the internet and development of smart software solutions, there is likely to be a continued rise in companies coming to the market. However, this sector can be complex to navigate from an investor perspective including the rise in offshore technology companies listing on the ASX.

Investor trends

The ongoing demand for yield has meant the demand for equities has remained elevated as investors shift from ‘more traditional’ investments in government bonds and other low interest bearing assets, such as term deposits, which are offering only 1 to 2 per cent returns per annum.

The Australian market has risen strongly over the past twelve months as investors embraced a more positive outlook for global growth. Notably with rising commodity prices, the resources index was up 23 per cent over the financial year after two years of underperformance and the banking sector also enjoyed a strong rebound over the year to produce a return of 18 per cent. This was somewhat surprising given the headwinds facing the sector came from regulatory and economic conditions as well as new taxes/levies. However, the dividend yield on offer in this sector remains attractive for income-focused investors.

In contrast over the year, investors displayed more caution towards other smaller companies which had previously been trading at very high share prices. Some experienced significant reductions in value as they lowered their growth expectations.

With investors seeking greater access to diversity and competitive yields, the popularity and demand for LICs continues to rise, particularly from SMSF investors. This has also meant there has been a significant expansion in the number and asset classes covered by the LIC sector, as well as the increased use of ETFs.

Financial advisers will be expected to understand the differences between LICs and ETFs, as well as understanding the features and benefits of LICs.

The rise of different investment vehicles: LICs vs. ETFs

Prior to the Future of Financial Advice (FoFA) reforms implemented in 2012, LICs were not popular investment options for many financial advisers because commissions were not available.

When the legislation became mandatory in 2013[5] and trailing commissions were banned, many financial advisers changed their business models to accommodate a different approach to charging customers. This levelled the playing field for investment vehicles such as LICs and ETFs as advisers sought lower cost alternatives for their clients in the context of evaluating which investments would be best for them.

LICS:

LICs are close-ended actively managed funds with a fixed number of shares and capital on issue. The shares trade daily on the ASX allowing investors to buy and sell with relative ease. LICs are valued at the proportion of underlying net tangible assets (the portfolio) per share (NTA), while the share price depends on equity market demand. Sometimes the share price can trade at a premium or discount to the NTA. This can create further opportunities for investors.

Investors are also attracted to LICs because of their transparent and simple structure. Continuous market disclosure is a feature because LICs are listed on the stock exchange. This means shareholders have the opportunity to gain a greater understanding of what’s in the portfolio and receive briefings from the LICs’ management team. Similarly, the structure of LICs is such that dividend payments are often more reliable and tax implications are usually more straightforward e.g. fully franked dividends and LIC gains.

ETFs:

Comparatively, Index ETFs tend to track share market indices or use a rule-based approach to investing, rather than the active management approach of LICs. They are structured as open-ended trusts, meaning these vehicles are exposed to capital inflows and outflows as market sentiment changes. The ETF structure allows investors to receive the market value of the underlying portfolio (less a small margin), should they wish to buy or sell their position. There are certain tax obligations associated with distributions from an ETF depending on its investment focus.

The key differences – LICs vs. ETFs

The close-ended structure of a LIC allows it to concentrate on selecting investments without having to factor in money coming into or leaving the fund. This stability assists in taking a long-term approach to investing. It also allows the portfolio manager to take advantage of weak market conditions when value may be on offer as the LIC does not need to manage redemptions in a difficult market. In contrast, when the market is running strongly, a LIC does not have to buy holdings when value may be more difficult to identify.

ETFs, on the other hand, are exposed to redemptions and issuance depending on market sentiment with no control over the investment timing or process.

As a company structure, LICs can choose to retain earnings and reinvest them or pay out earnings as dividends. LICs pay company tax on their earnings and can pass through franking credits along with their dividends. This flexibility in the distribution of dividends allows them to potentially smooth out dividend payments over time. This is very important to many LIC investors focused on more certainty of income.

ETFs are unable to retain earnings so these vehicles must pass on any earnings – dividends or realised gains – within any given financial year meaning distribution may be more variable.

Both LICs and ETFs can appeal to retail investors, so it is the responsibility of the financial adviser to review the underlying performance of the fund, the cost and the track record of the people managing the money to ensure that the vehicle aligns with their clients’ best interests.

——–

[1] http://www.morningstar.com.au/s/documents/201706_ASX-LIC-NTA-Report.pdf

[2] http://www.asx.com.au/resources/newsletters/listed_at_asx/20090820_market_performance.htm

[3] http://www.treasury.gov.au/PublicationsAndMedia/Publications/2011/Economic-Roundup-Issue-2/Report/Part-1-Reasons-for-resilience

[4] http://www.asx.com.au/about/corporate-overview.htm

[5] http://futureofadvice.treasury.gov.au/content/Content.aspx?doc=home.htm