Investors should consider an absolute return approach to fixed income.

Objective assessment

As key global central banks tentatively turn toward monetary policy normalisation, the prospect of a prolonged period of rising interest rates has left some investors questioning the merits of retaining an exposure to fixed income. Investors concerned about the potential for rising interest rates could consider an absolute return approach to bond investing as an alternative or complement to traditional, long-only bond strategies.

Global interest rates: to rise or not to rise? That is the question

After almost a decade of ultra-accommodative monetary policy, key developed market central banks are now shifting their focus toward policy normalisation. The Federal Reserve (Fed) kick- started the process in January 2014 by tapering its bond purchase program, a process it concluded by October that same year. It proceeded to the next phase of normalisation a year later by implementing a 25 basis points (bp) rate hike, the first since 2006, and has implemented a further three hikes since then. An announcement on its strategy for balance sheet reduction looks likely in late 2017.

While the European Central Bank (ECB) is at a different stage of the policy normalisation process, it looks set to provide some clear guidance on tapering of its bond purchase program in the near term and may begin raising interest rates in 2018. Although Australia’s economic narrative has largely diverged from that of the US and Europe over the past decade, the Reserve Bank of Australia (RBA) currently maintains its benchmark cash rate at the historically low level of 1.5%. The RBA may be inclined to sync its monetary policy cycle with that of the Fed and ECB should inflation return to target and growth accelerate.

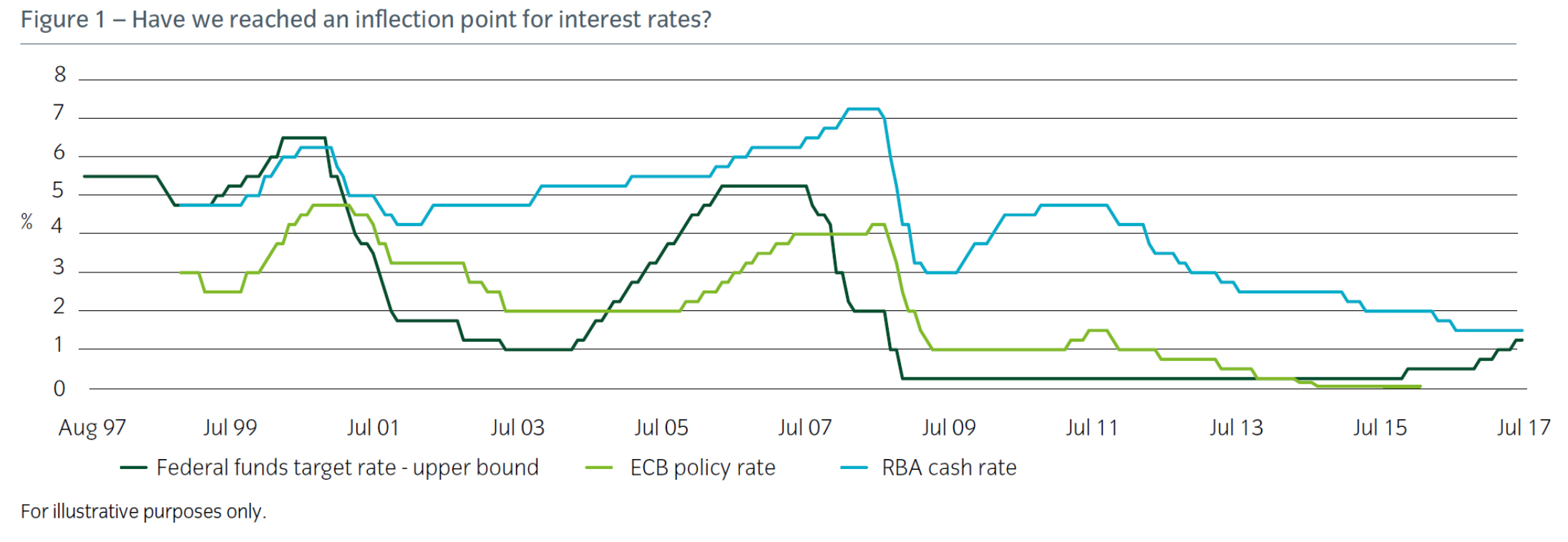

For some investors, these cues mark the start of a prolonged period of tighter monetary policy and rising interest rates, and increase concerns over the outlook for bonds (Figure 1). Such concerns are understandable because bond prices move inversely to movements in interest rates. Most at risk are government treasury bonds, which are purer interest rate securities and lack the additional spread component of credit bonds. Also at greater risk are longer-duration bonds, which have inherently higher levels of interest rate sensitivity (or duration), and low-yielding bonds which lack the carry cushion to absorb adverse price movements.

During the most recent period of monetary easing prompted by the 2008-2009 Global Financial Crisis (GFC), interest rate sensitivity was viewed less as a concern and more as a boon for investors.

The sharp decline in global interest rates led bonds to outperform. The reverse may be the case if we enter a prolonged period of rising rates – one would expect bonds to incur capital losses as prices fall. With many core government bond yields currently at multi-decade lows, the cushion available to absorb any meaningful move higher in interest rates is severely limited. Hence the concerns shared by many bond investors.

The limitations of long-only, constrained fixed income investing

By design, traditional long-only or constrained approaches to fixed income investing limit the opportunity set to that prescribed by a benchmark. In the case of government bond funds – where duration is a key driver of return – investors are typically exposed to adverse interest rate moves, with limited scope to mitigate these risks. These funds are structurally long duration by design and the prospect of rising interest rates over the coming years may leave these investors exposed to capital losses. Even in the case of funds managed against more broad-based fixed income benchmarks – such as the Bloomberg Barclays Global Aggregate Index[1] – tracking error constraints can restrict the degree to which fund managers can avoid the most interest rate-sensitive segments of the market, irrespective of their overall view on the direction of bond yields.

Not all fixed income is equal

The global fixed income market is very diverse in terms of instrument type, sector, credit quality, maturity and geographical composition. According to the Bank for International Settlements’ latest estimates, there is currently in excess of US$100 trillion worth of fixed income securities outstanding globally[2] . Fixed income provides scope for opportunity far beyond the traditional core sectors of developed market government bonds and investment grade credit. Opportunities exist across the risk/return spectrum and include investment grade and high yield credit, global treasuries, securitised products and emerging market sovereign and corporate debt. Duration, yield curve, credit, geography and sector selection, inflation and currency all provide avenues for alpha generation. We believe the diversification benefits and scope for generating positive returns using fixed income should not be ignored.

Investors should consider an absolute return approach to fixed income

With such a broad palette of opportunity available, fixed income ought to be an integral part of any investor’s portfolio. Investing in bonds does not mean, however, that investors should be forced to assume unnecessary interest rate risk – particularly if they are concerned about the potential for rising rates. An absolute return approach to fixed income is naturally unconstrained and allows investors to benefit from the sheer breadth of alpha and diversification opportunities that the market provides, without the risk and sector biases inherent in more traditional, long-only constrained approaches. Such strategies typically seek a lower volatility profile and have the potential to deliver positive returns in both strong and weak market environments. In addition to sourcing alpha opportunities from across the fixed income universe, absolute return fixed income strategies can use techniques to generate positive returns in declining markets, preserve capital and smooth volatility. As a result, they tend to have a low correlation to both equity and bond markets and act as effective portfolio diversifiers.

Conclusion

As central banks sharpen their focus on monetary policy normalisation, investors are understandably concerned about the prospect of a prolonged period of rising interest rates and what this means for their bond investments. It is evident from the last few years that constrained, fixed income offerings have benefitted from falling interest rates and compressing spreads. Should these tailwinds begin to subside, it is not unreasonable for investors to ask how returns and capital preservation will be delivered in the future under the possibility of different economic and financial market conditions. Indeed, it is worth reflecting upon how your fixed income manager has added value to your portfolio over recent years and whether the same value can be achieved going forward. An unconstrained, absolute return approach to fixed income investing allows investors the potential to reap the diversification and alpha opportunities that the global fixed income universe provides, without being forced to take unnecessary interest rate risk.

[1] The Bloomberg Barclays Global Aggregate Index is a measure of global investment grade debt from 24 local currency markets. This multi-currency benchmark includes treasury, government-related, corporate and securitised fixed-rate bonds from both developed and emerging markets issuers.

[2] Bank for International Settlements (BIS), June 2017, BIS Quarterly Review June 2017 – International Banking and Financial Market Developments.

———-