Weekly market update – week ending 8 September, 2017

Investment markets and key developments over the past week

Share markets mostly fell over the last week as worries around North Korea continue, combining with concern about the impact of hurricanes on US growth, albeit most markets remain in the range they have been in for a while and have proven quite resilient in the face of bad news thanks to solid global growth and supportive monetary policy. While Eurozone shares rose 0.1%, US shares lost 0.4%, Japanese shares fell 2.1%, Chinese shares fell 0.1% and Australian shares fell 0.9%. Bond yields fell further helped by dovish comments from ECB President Draghi, a downwards revision to the ECB’s inflation forecasts and worries about the impact of hurricanes on the US. However, the Euro rose as President Draghi wasn’t seen as dovish enough resulting in a new down leg in the $US which also saw the $A push back above $US0.80. Oil and gold prices rose but iron ore fell.

Having broken key technical support levels the US dollar could fall further in the short term – which would be positive for US shares as it boosts US profits, global liquidity and the emerging world with $US debt – but it’s likely to reverse sometime in the next few months. The impact of hurricanes on US growth will be temporary and on a 3-6 month horizon they will provide a rebuilding boost so the Fed will look through them – as it did with Hurricane Katrina in 2005. And more fundamentally the falling $US is unwinding the Fed’s monetary tightening which is risking it becoming more aggressive at some point and the rising Euro is driving a monetary tightening in Europe at a time when Europe still needs easing and so will eventually force the ECB to counter it. This could mean a slower reduction than expected in its quantitative easing program. The rising $A will also constrain Australian growth and inflation, further delaying RBA tightening.

We thought Hurricane Harvey made a US Government shutdown and debt ceiling crisis this month very unlikely and this has proved to be the case with President Trump and Congress agreeing to extend government funding and raise the debt ceiling out to mid-December. So no shutdown and no debt default for now. This continues the period of budget and spending stability that has been in place since the 2013 “crisis”. Uncertainty will rise again in December but a shutdown/debt default is also unlikely then. At the margin the move adds to confidence that tax reform will happen.

Trump’s threatening tweets – eg, that he will stop all trade with countries trading with North Korea (read China) – create great media headlines but just remember that the trick with Trump is to take him seriously but not literally. His approach is all about setting up tough a negotiating stance, getting some movement in his direction and then settling. So yes he is trying to put more pressure on China regarding North Korea but don’t expect the US to cease trade with China.

Uncertainty around the Fed ramped up a bit over the last week with Vice Chair Fischer resigning and reports that President Trump’s economic adviser Gary Cohn was no longer in the running for Fed Chair raising the possibility that Trump’s replacements may see the Fed take a more hawkish turn. This is not necessarily the case and in fact it’s in Trump’s interest to have stability at the Fed and he has indicated a leaning towards a “low interest rate” Fed all of which suggests he is unlikely to rock the boat with hawkish appointments. Yellen remains in with a chance if she wants it, but her supportive comments for post GFC financial regulation work against her to some degree.

North Korean risks continue to escalate. Our view remains that the risk of a skirmish or war has grown – particularly due to a miscalculation by either side in the conflict, but that a diplomatic solution remains most likely as North Korea is not quite so stupid to set off a war in which it will be annihilated and the US and its allies are aware of the potential huge loss of life in South Korea and potentially Japan that would flow from a pre-emptive military response. But we are a long way from a diplomatic solution yet. So the issue is likely to escalate further posing the risks of triggering further downside in share markets and demand for safe havens.

The September 24 German election and October 1 Catalan election are of limited relevance for investors. Polling has Angela Merkel on track to easily “win” the German election with the issue being who she forms a coalition with: the Social Democrats again in which case the outcome is more pro-Europe or the Free Democratic Party which is less pro-Europe. It’s probably irrelevant as Merkel has migrated to a more pro-Europe stance anyway. The nationalist anti-Euro Alternative for Deutschland is a sideshow getting less than 10% support. The Catalan independence referendum on October 1 may generate a bit of noise but it’s essentially a Spanish issue with not much relevance to the Eurozone. In any case the referendum is illegal, most Catalan’s prefer to stay in Spain but with more fiscal independence, independence is a long way off anyway even if there is support for it amongst a majority of Catalans and in any case Catalonia wants to stay in the Euro. The Italian election to be held before May 2018 is the one to watch but even here the populist Five Star Movement is wavering in its anti-Euro stance and it remains doubtful it will be able to form government (even if it gets more parliamentary seats than any other party). So a Euro break up continues to look unlikely and in the meantime its economy is getting stronger and its shares are cheap. The only fly in the ointment is the rising Euro.

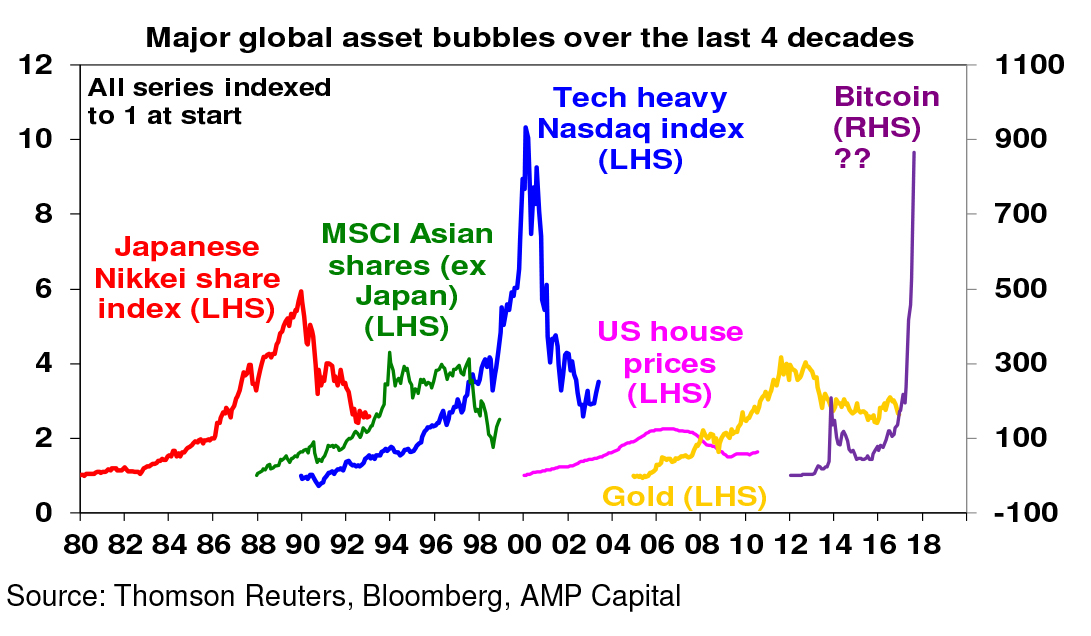

What about Bitcoin? Crypto currencies led by Bitcoin are generating much interest. They and the block chain technology underpinning them seem to hold much promise but there is reason to be cautious. Lots of them are popping up, the ascent of Bitcoin’s share price looks very bubbly (although its potential ramifications if it bursts are nowhere near as significant as the other bubbles shown on the chart) and regulators are starting to take a closer look. I also still struggle to fully understand how it works and one big lesson from the GFC is that if you don’t fully understand something you shouldn’t invest (who really understood CDOs? – obviously not many!)

Investment markets and key developments over the past week

Share markets mostly fell over the last week as worries around North Korea continue, combining with concern about the impact of hurricanes on US growth, albeit most markets remain in the range they have been in for a while and have proven quite resilient in the face of bad news thanks to solid global growth and supportive monetary policy. While Eurozone shares rose 0.1%, US shares lost 0.4%, Japanese shares fell 2.1%, Chinese shares fell 0.1% and Australian shares fell 0.9%. Bond yields fell further helped by dovish comments from ECB President Draghi, a downwards revision to the ECB’s inflation forecasts and worries about the impact of hurricanes on the US. However, the Euro rose as President Draghi wasn’t seen as dovish enough resulting in a new down leg in the $US which also saw the $A push back above $US0.80. Oil and gold prices rose but iron ore fell.

Having broken key technical support levels the US dollar could fall further in the short term – which would be positive for US shares as it boosts US profits, global liquidity and the emerging world with $US debt – but it’s likely to reverse sometime in the next few months. The impact of hurricanes on US growth will be temporary and on a 3-6 month horizon they will provide a rebuilding boost so the Fed will look through them – as it did with Hurricane Katrina in 2005. And more fundamentally the falling $US is unwinding the Fed’s monetary tightening which is risking it becoming more aggressive at some point and the rising Euro is driving a monetary tightening in Europe at a time when Europe still needs easing and so will eventually force the ECB to counter it. This could mean a slower reduction than expected in its quantitative easing program. The rising $A will also constrain Australian growth and inflation, further delaying RBA tightening.

We thought Hurricane Harvey made a US Government shutdown and debt ceiling crisis this month very unlikely and this has proved to be the case with President Trump and Congress agreeing to extend government funding and raise the debt ceiling out to mid-December. So no shutdown and no debt default for now. This continues the period of budget and spending stability that has been in place since the 2013 “crisis”. Uncertainty will rise again in December but a shutdown/debt default is also unlikely then. At the margin the move adds to confidence that tax reform will happen.

Trump’s threatening tweets – eg, that he will stop all trade with countries trading with North Korea (read China) – create great media headlines but just remember that the trick with Trump is to take him seriously but not literally. His approach is all about setting up tough a negotiating stance, getting some movement in his direction and then settling. So yes he is trying to put more pressure on China regarding North Korea but don’t expect the US to cease trade with China.

Uncertainty around the Fed ramped up a bit over the last week with Vice Chair Fischer resigning and reports that President Trump’s economic adviser Gary Cohn was no longer in the running for Fed Chair raising the possibility that Trump’s replacements may see the Fed take a more hawkish turn. This is not necessarily the case and in fact it’s in Trump’s interest to have stability at the Fed and he has indicated a leaning towards a “low interest rate” Fed all of which suggests he is unlikely to rock the boat with hawkish appointments. Yellen remains in with a chance if she wants it, but her supportive comments for post GFC financial regulation work against her to some degree.

North Korean risks continue to escalate. Our view remains that the risk of a skirmish or war has grown – particularly due to a miscalculation by either side in the conflict, but that a diplomatic solution remains most likely as North Korea is not quite so stupid to set off a war in which it will be annihilated and the US and its allies are aware of the potential huge loss of life in South Korea and potentially Japan that would flow from a pre-emptive military response. But we are a long way from a diplomatic solution yet. So the issue is likely to escalate further posing the risks of triggering further downside in share markets and demand for safe havens.

The September 24 German election and October 1 Catalan election are of limited relevance for investors. Polling has Angela Merkel on track to easily “win” the German election with the issue being who she forms a coalition with: the Social Democrats again in which case the outcome is more pro-Europe or the Free Democratic Party which is less pro-Europe. It’s probably irrelevant as Merkel has migrated to a more pro-Europe stance anyway. The nationalist anti-Euro Alternative for Deutschland is a sideshow getting less than 10% support. The Catalan independence referendum on October 1 may generate a bit of noise but it’s essentially a Spanish issue with not much relevance to the Eurozone. In any case the referendum is illegal, most Catalan’s prefer to stay in Spain but with more fiscal independence, independence is a long way off anyway even if there is support for it amongst a majority of Catalans and in any case Catalonia wants to stay in the Euro. The Italian election to be held before May 2018 is the one to watch but even here the populist Five Star Movement is wavering in its anti-Euro stance and it remains doubtful it will be able to form government (even if it gets more parliamentary seats than any other party). So a Euro break up continues to look unlikely and in the meantime its economy is getting stronger and its shares are cheap. The only fly in the ointment is the rising Euro.

What about Bitcoin? Crypto currencies led by Bitcoin are generating much interest. They and the block chain technology underpinning them seem to hold much promise but there is reason to be cautious. Lots of them are popping up, the ascent of Bitcoin’s share price looks very bubbly (although its potential ramifications if it bursts are nowhere near as significant as the other bubbles shown on the chart) and regulators are starting to take a closer look. I also still struggle to fully understand how it works and one big lesson from the GFC is that if you don’t fully understand something you shouldn’t invest (who really understood CDOs? – obviously not many!)

By Shane Oliver, AMP Capital