Successive governments have pushed out the age at which Australians can access superannuation and aged pension benefits, which for many, delays the age at which they can retire. In this article, Centuria Capital examines the need for retirement savings and looks at investment strategies outside of superannuation that could fund an early retirement.

Up there with the great Australian dream of home ownership is the dream of early retirement – why wait until you’re too old to enjoy it, right? Whether it’s world travel, undertaking voluntary work, or buying a caravan and seeing Australia grey nomad style, most of us have a plan, a dream, for those post-work years. Why then does early retirement seem to be out of reach for the majority?

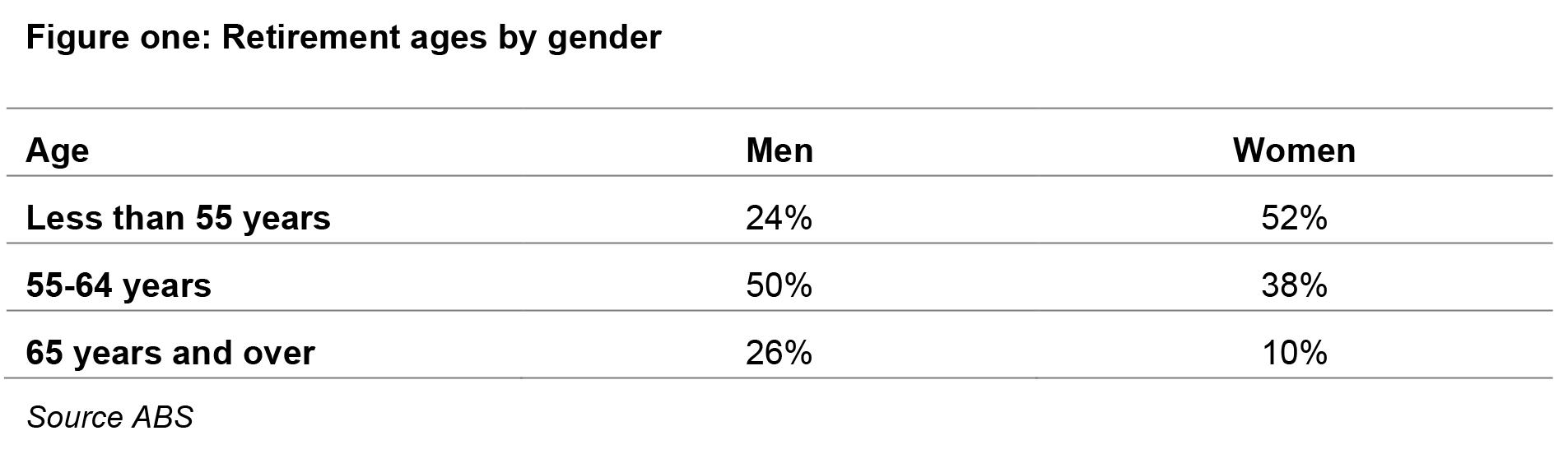

Retirement age and intention

The 2014–15 Multipurpose Household Survey (MPHS) undertaken by the Australian Bureau of Statistics (ABS) found that the average age at retirement for people aged 45 years and over in 2014–15 was 54.4 years (58.2 years for men and 51.5 years for women); as illustrated in figure one, women generally retire at an earlier age than men.

The average retirement age those who have retired in the last five years was 61.5 years; 62.6 years for men and 60.4 years for women.

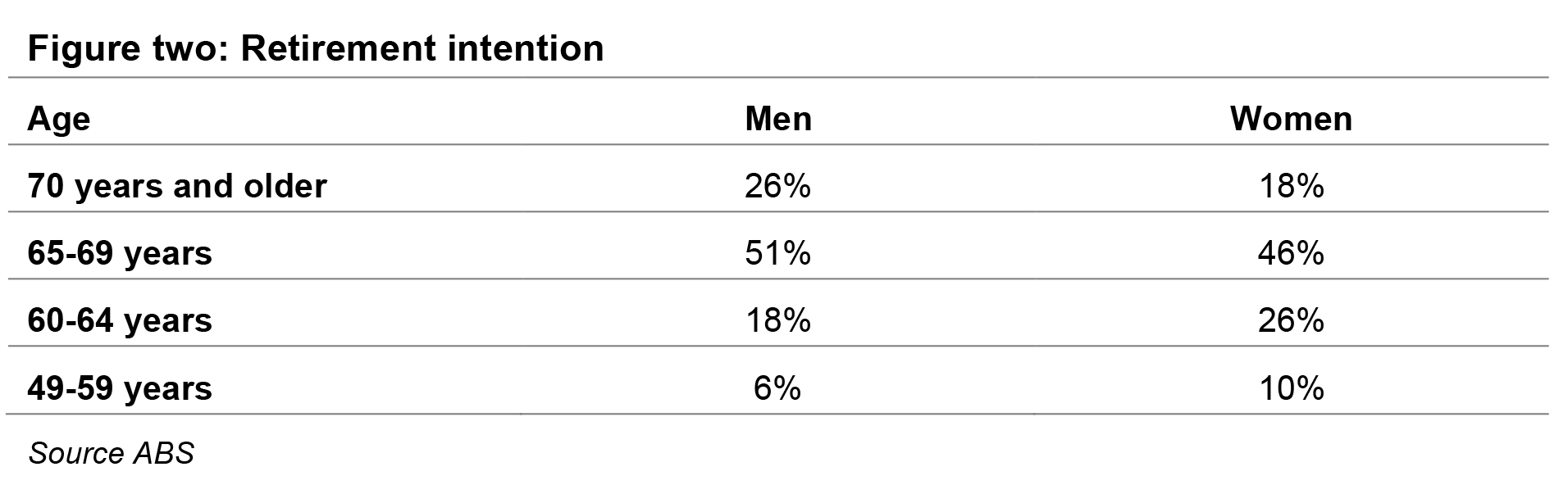

Of the 3.8 million people over 45 years that are currently employed, 1.3 million (35%) could not say at what age they would likely retire. Figure 2 indicates the responses from the remaining 65% of this cohort.

The survey included retirement funding; 53% of those aged 45 years and over expect their main source of retirement income to be superannuation, annuity or allocated pension, and 27% cited government pension or allowance to be the main source of expected income. Early retirement is not the in the sights of many.

Access to superannuation and aged pension

Two factors trigger access to superannuation savings – reaching the preservation age and retirement. Tax may be payable on any super benefits withdrawn before the age of 60 (subject to certain exceptions).

Since 1 July 2017, the age at which retirees can apply for the Age Pension has increased to 65.5 years and, as illustrated in figure four, will increase to 67 years of age in coming years. When he was treasurer, Joe Hockey caused a lot of angst with a proposed increase in this age to 70 years; while this did not pass, there remains the spectre of further increases in age before eligibility in the future.

As well as speculation around a changing age at which the Aged Pension may come into play, there has been chatter about increasing the preservation age for access to retirement savings. For clients making medium to long-term retirement plans, the potential for such changes needs to be considered. Many of those solely reliant on superannuation savings will have little choice about the timing of their retirement.

Getting older, living longer

Australia’s population is ageing and, at the same time, life expectancy is increasing thanks to better healthcare and a higher standard of living.

Retirement savings will have to last longer in the future. A person who retires at age 55 will have, on average, a further thirty years of life to fund. With the limits on superannuation savings that came into effect on 1 July this year, can superannuation be relied on as the only form of retirement savings?

Although the ABS retirement intentions data suggests only a small number of Australians wish to retire early (i.e. between ages 49 and 59), this is likely tied in with the planned reliance on superannuation to fund retirement. With super off the table until at least age 60 – with the prospect of further changes pushing out preservation age – what investment strategies can be engaged to fund an early retirement?

Investment strategies to fund an early retirement

Many Australians invest outside the superannuation system. Whether it’s an investment property, a share portfolio, ETFs or a term deposit, investors adopt a range of strategies to meet short, medium or long-term financial goals. Let’s consider the pros and cons of several common investment strategies that could be used to fund an early retirement.

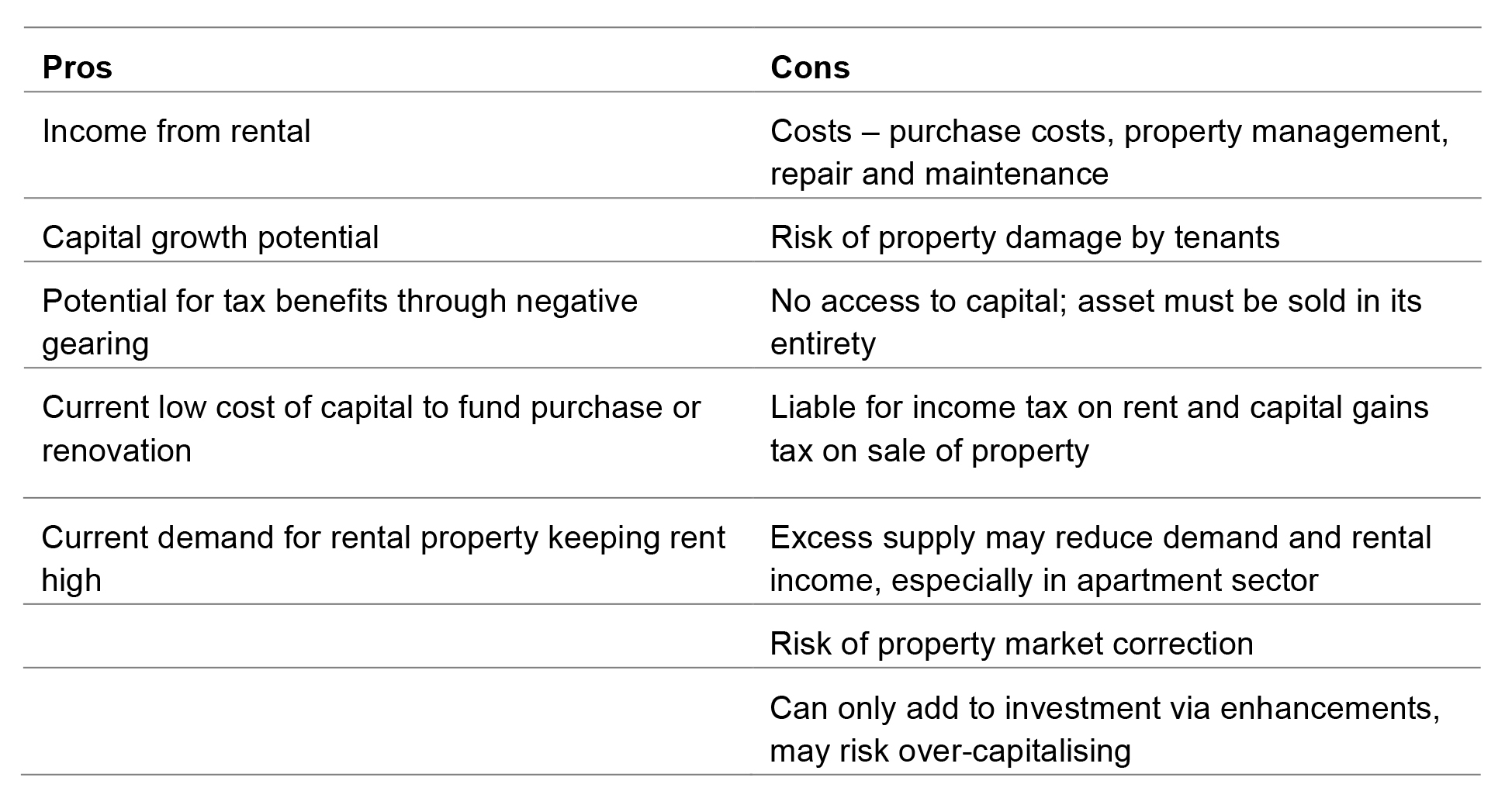

Residential investment property

Low interest rates coupled with increased demand for housing stock has created a boon for property investors. The opportunity to use negative gearing can provide some tax benefits to property investors.

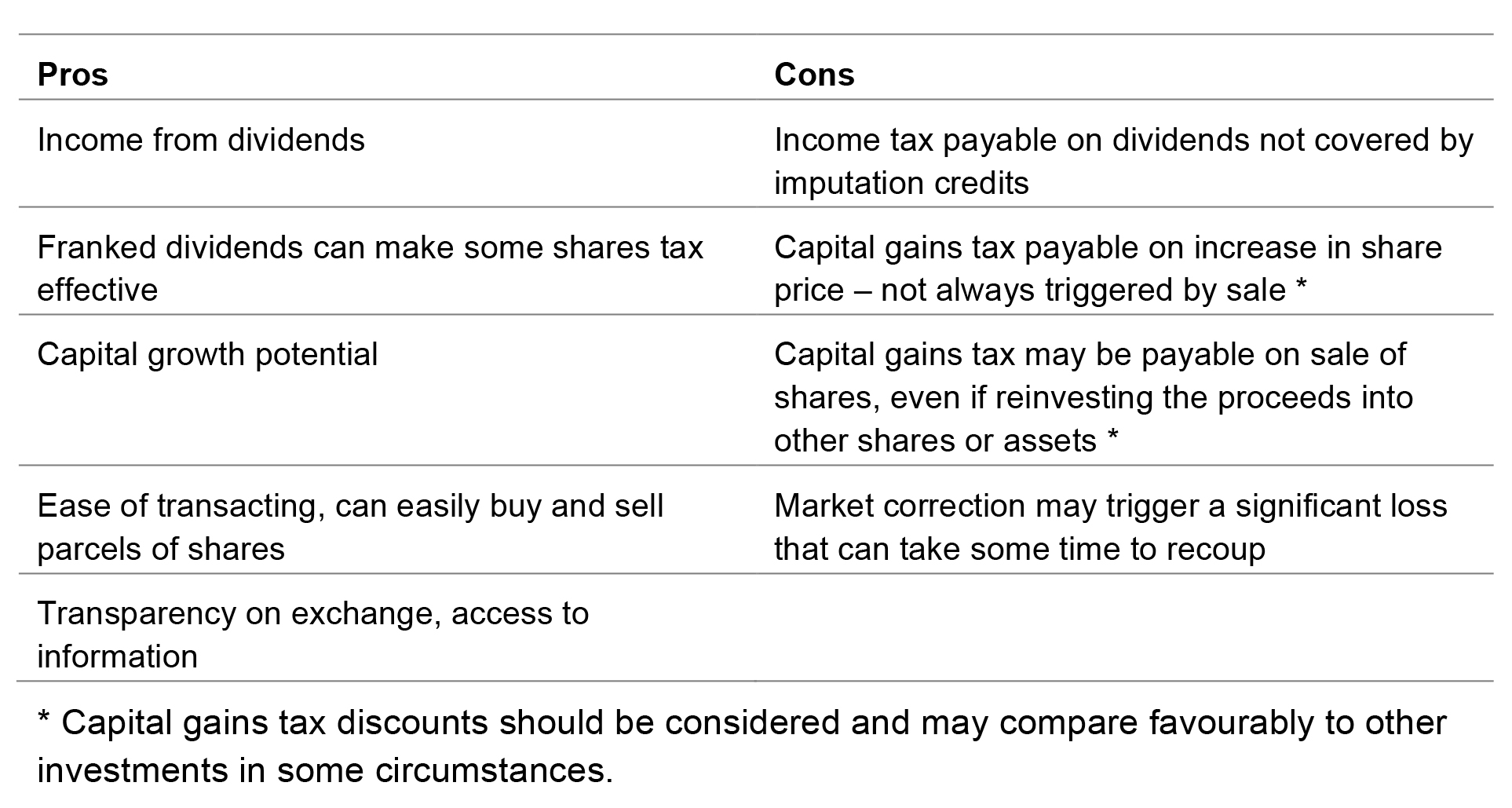

Australian share portfolio

Australia’s unique dividend imputation system allows many listed companies to pay dividends that are partly or fully franked – in other words, are partly or fully tax paid, at the prevailing corporate tax rate. If an investor holds a portfolio of stocks that each pays a fully franked dividend, the investor would pay:

- No income tax if their marginal tax rate is equal to or less than the corporate tax rate, or

- The difference between their marginal tax rate and the corporate tax rate.

However, not all companies pay fully franked dividends, and some dividends have no tax paid at all.

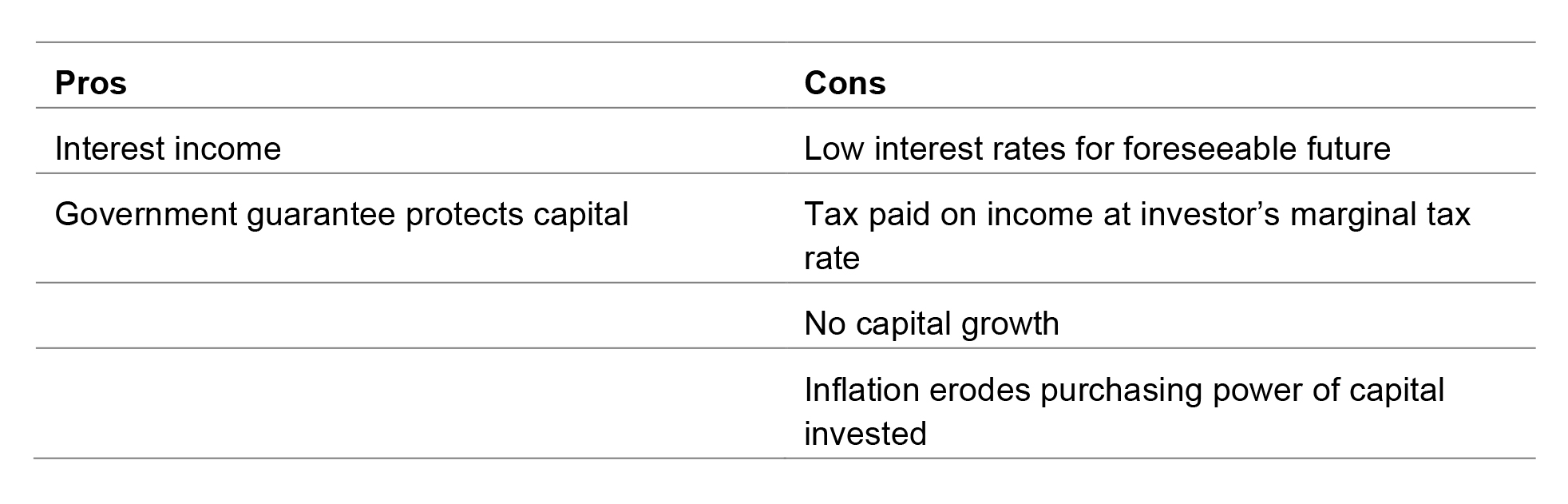

Term deposits

RBA data reveals the average term deposit rate on a one year, $10,000 investment was 2.25% at 31 July 2017; for three years, it’s 2.5%. Given the current inflation rate of 1.9%, once tax is paid on the income received, it would be unlikely to keep pace with inflation. In real terms, each dollar of income received would be worth less than when it was invested. Despite this, APRA’s Monthly Banking Statistics for June 2017 shows that Australians have more than $844 billion on deposit.

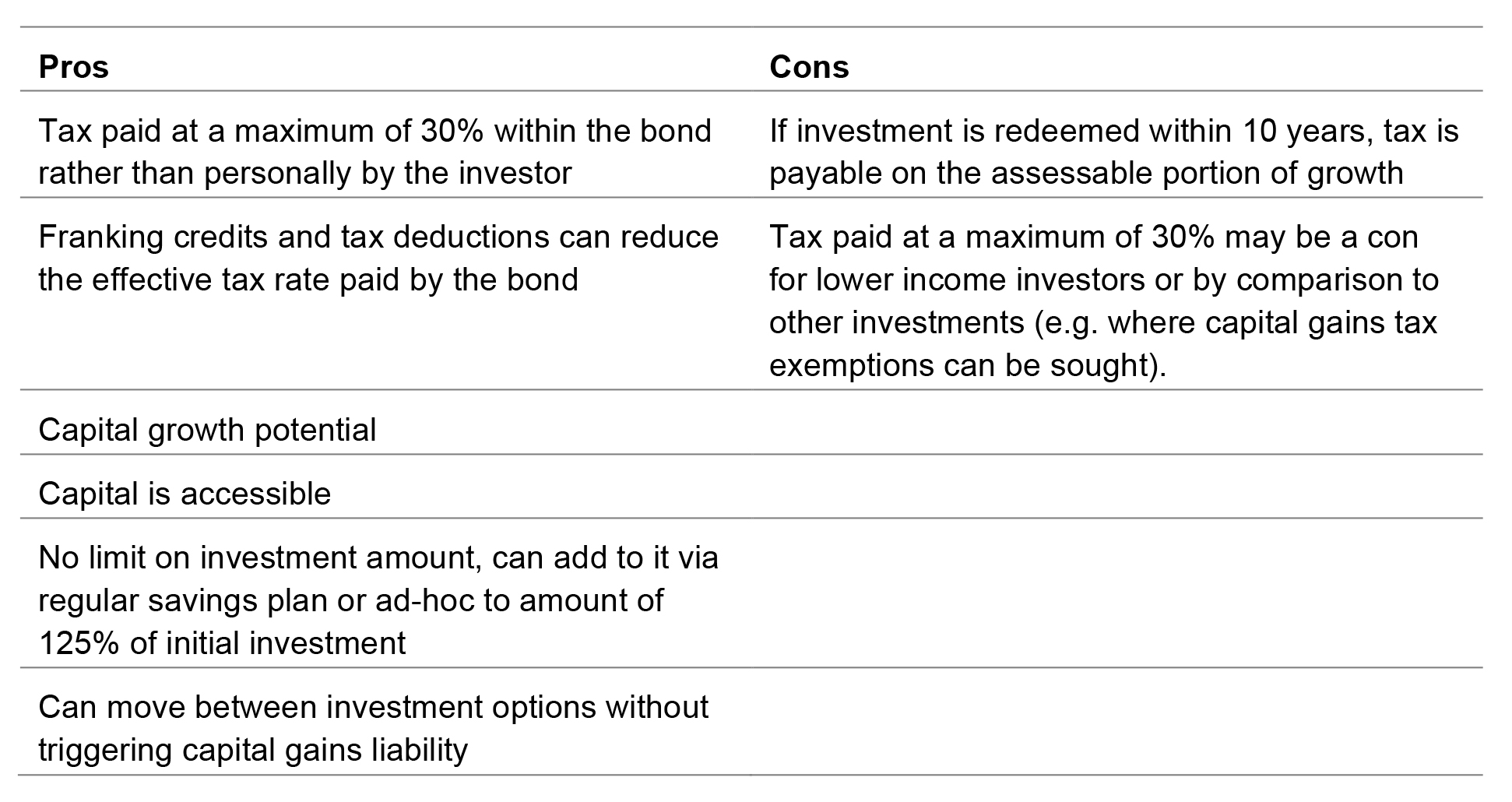

Investment bonds

An investment bond is a tax effective structure; tax is paid within the investment bond rather than personally by the investor. The maximum tax paid on the earnings and capital gains within an investment bond is 30%, although franking credits and tax deductions can reduce this effective tax rate.

If an investment bond is held for 10 years, no personal tax is paid by the investor, which makes investment bonds a particularly attractive retirement savings vehicle. However, the money is accessible; if the investment is redeemed in whole or part within the first 10 years, the investor will pay tax on the assessable portion of growth.

There are many ways to save outside of superannuation for an early retirement. Of the alternative options explored, investment bonds are a unique and useful savings vehicle. No other investment provides exposure to a range of underlying investment options with no tax liability on maturation after 10 years. Your clients don’t have to wait until they reach preservation age – with sound planning and saving, they can choose the timing of their retirement.