How can investment bonds can help to mitigate risk?

Investment risk can be defined as the probability that an investment’s actual return will differ from its expected return; however, there are other risks that can impact investors, particularly those close to, or in, retirement.

In this article, Centuria Capital examines those risk and discusses ways that investment bonds can help to mitigate them.

There is a Wall Street saying that the market is driven by two emotions – fear and greed. So entrenched is this view that CNN Money created the ‘fear and greed’ index, which measures seven indicators to see which emotion is currently driving the market. While the index currently suggests that ‘extreme greed’ is driving US markets, many investors remain fearful about a market correction and capital loss.

Whether in the accumulation phase, pre-or-post retirement, fear can drive investors to make poor decisions; fear of a making a poor investment choice, fear of holding an investment too long, fear of low returns or a market crash. Each of these fears can lead to behaviour that can undermine the long-term returns of an investment portfolio.

US-based research company Dalbar[1] has been studying investor behaviour since 1994. According to Dalbar’s research, negative behaviours exhibited by investors have a common outcome – they lead investors to deviate from their investment strategy, even those tailored to their financial objectives, risk tolerance and time horizon. This often results in a knee jerk response to short term market conditions. For example, in its most recent report (for periods ending 31 December 2016), Dalbar’s research found that:

- Over 2016, the average US-based equity managed fund investor underperformed the S&P500 by a margin of 4.7%; much of this underperformance can be attributed to investors missing the ‘Trump rally’ in November (1.13%) and December (1.34%) 2016

- Over a 20-year investment period, the average equity fund investor underperformed the market by 2.89% per annum

- Equity fund retention rates decreased in 2016, from 4.10 years to 3.80 years

- Fixed income fund investors also experienced below market returns in 2016, with the average investor underperforming the Bloomberg Barclays Aggregate Bond Index by 1.42%.

According to Dalbar, the data emphasises two key points:

- The average fund investor does not stay invested for a long enough period to reap the rewards that markets can offer long term investors

- When investors react to short term market conditions, they generally make the wrong decision.

Investors need growth assets

Growth assets are important to all investors, both accumulators and retirees, because they provide longer-term capital growth as well as an income stream from dividends, distributions or rental income. While it is generally well accepted that investors in the accumulation phase should invest in growth assets to build their retirement nest egg, it’s just as important pre-and post-retirement. The average life expectancy is increasing and many retirees face the real prospect of outliving their retirement savings, especially if fear of loss drives them toward low risk investments that have little potential for capital growth or keeping pace with inflation. In fact, while investors may respond to fear of the risk of a market downturn, they might make themselves vulnerable to other risks.

Longevity risk

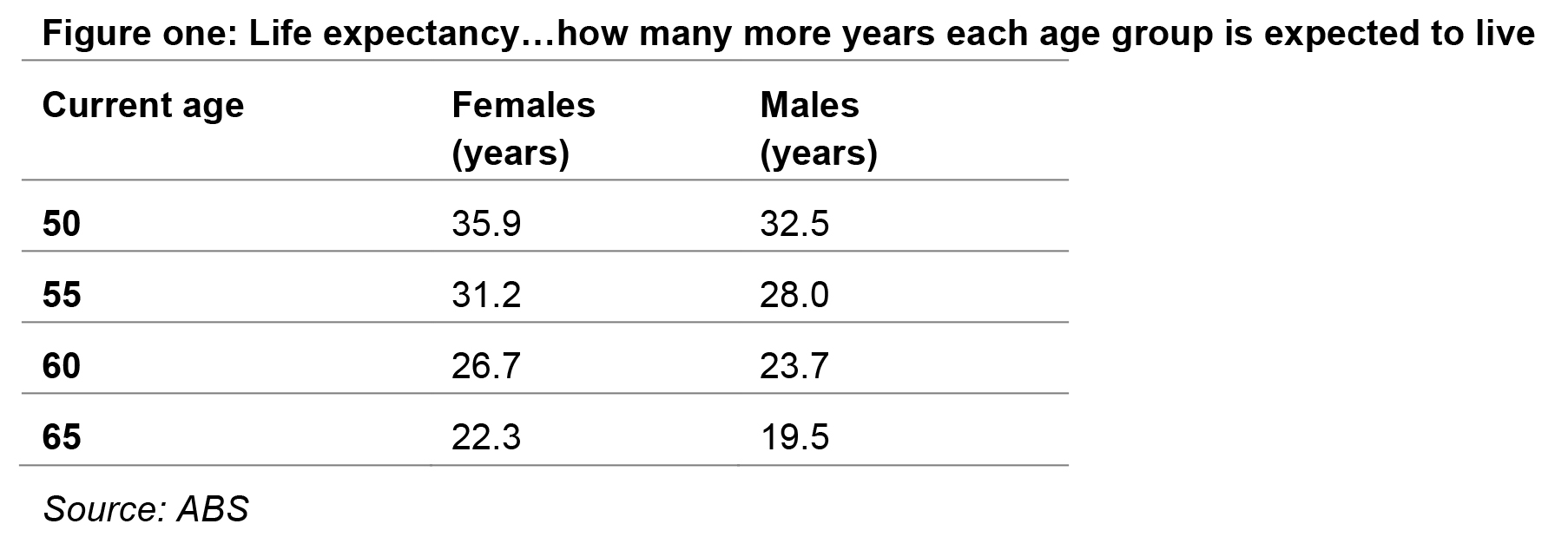

Put simply, longevity risk is the risk of a client outliving their retirement savings; Australian retirees face the very real prospect of a shortfall in their retirement savings as life expectancy continues to increase thanks to improvements in living conditions, health and medical advances. Figure one outlines today’s life expectancy for a range of ages.

While many Australians risk of outliving their savings if they invest too conservatively both before and during retirement, fear of capital loss from a downturn in markets restricts their exposure to growth assets.

Inflation risk

Inflation risk is the risk that investments and income lose purchasing power over time as the cost of goods and services increase. Purchasing power is the value of money, expressed in terms of the amount of goods or services that one unit of money can buy. Higher inflation means lower purchasing power.

Although Australia’s inflation rate at 30 September was a relatively low 1.3% (source: RBA), some essentials – such as gas and electricity, health insurance, and meat and dairy – have experienced price increases well above the headline inflation rate. As with investment returns, inflation has a compounding effect over time and can erode the value of a capital pool that remains static.

According to the Reserve Bank of Australia’s Inflation Calculator[2], a basket of goods and services worth $100 in 1996 would have cost $163.49 in 2016 – an increase of 63.5% over the 20-year period. So, while money in the bank may have preserved capital, its value diminishes over time.

Growth assets and fear

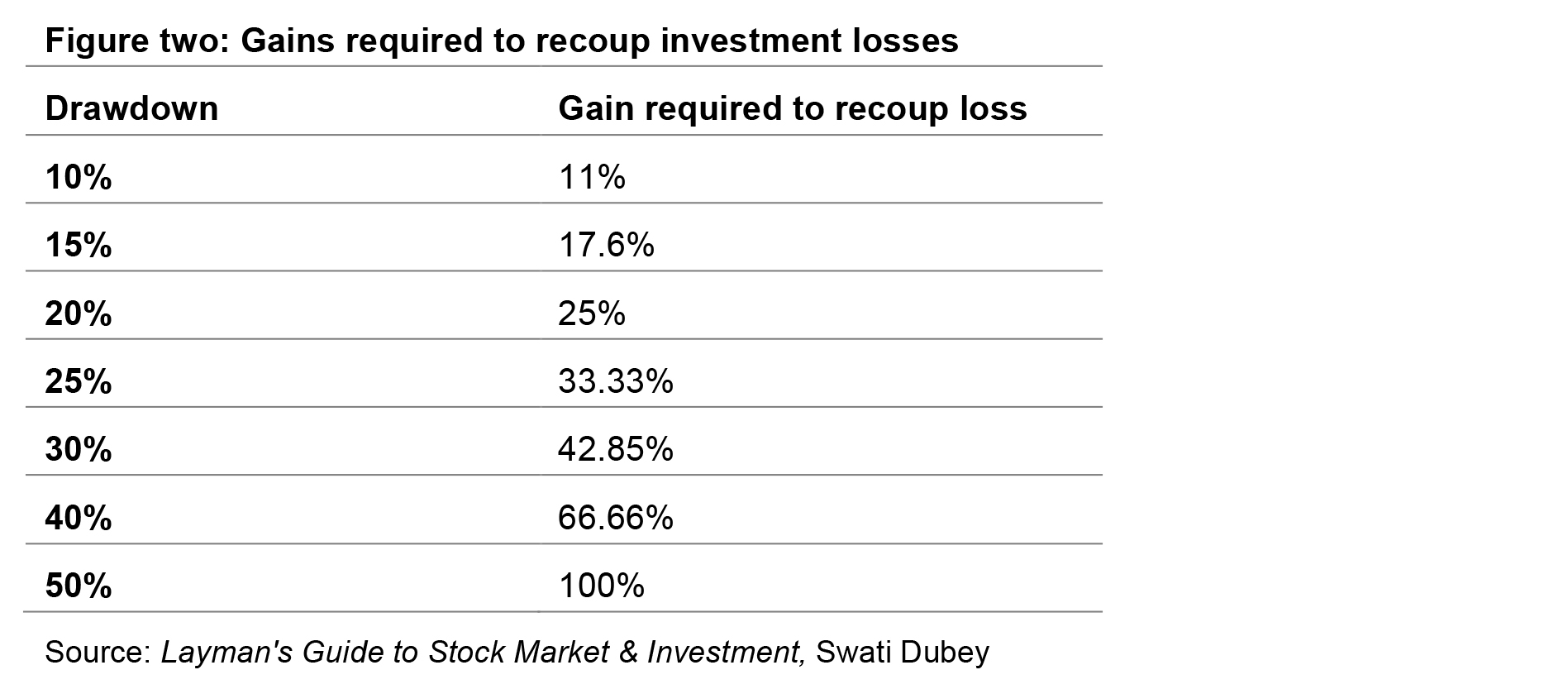

No-one likes to see the value of their assets diminish. Sequencing risk is the risk that the order and timing of investments and returns are unfavourable. The wrong sequence of returns can have a particularly significant impact on a retirement portfolio where investors have less time to recoup losses, and will be withdrawing funds from a diminishing pool of capital. As illustrated in figure two, investment losses, or drawdowns, require a significant uplift to get back to the same point, let alone grow.

If investors experience positive investment returns in the first few years of retirement, they will be better placed to ride out market downturns. However, if returns early in retirement are negative, then proportionately more capital is required to fund ongoing living expenses.

How can investment bonds help mitigate risk?

An investment bond is an insurance policy, with a life insured and a beneficiary, but works like a tax-paid managed fund. And as with a managed fund, you can make recommendations to your clients from a broad range of underlying investment portfolios. These typically range from growth oriented assets, such as equities, to defensive assets such as fixed interest. They can also include other asset classes and combinations of assets.

A key feature of investment bonds is the ability to switch between investment options without triggering a personal capital gains tax liability. For an investor fearful of an imminent collapse in equity or bond markets, they can simply switch all or part of their bond into another investment option.

While market timing has well documented risks of its own, the comfort of knowing an investment can be simply and easily transferred from one asset class to another may be enough to assuage the fear of loss; and if not, an investor that moves from a growth option to a more conservative option for a period of time can do so without giving up precious capital gains. It is, of course, a simple task to switch back – or take a diversified option – in due course.

Investment bonds provide a range of other benefits that make them ideal vehicles for both accumulators and retirees:

Tax effective structure

An investment bond is a tax effective structure; tax is paid within the investment bond rather than personally by the investor. The maximum tax paid on the earnings and capital gains within an investment bond is 30%, although franking credits and tax deductions can reduce this effective tax rate. This makes investment bonds a particularly attractive savings vehicle, pre-and post-retirement, for high income earners.

No annual tax reporting

As long as a client’s money remains invested, the manager of the investment bond will pay tax on investment earnings; there is no requirement for your client to declare those earnings in their annual tax reporting.

No limit on investment amount

There is no limit on the amount that can be invested to establish an investment bond. Investors can make subsequent investments up to maximum of 125% of the previous year’s contribution without restarting the ten-year period.

Additional investments can be made annually or as a regular contribution. For those concerned about market risk, the benefits of dollar cost averaging can provide a compelling rationale for a regular contribution.

Importantly, investment bonds can help you address the two behaviours that, according to Dalbar, result in below average returns for many investors:

i) The average fund investor does not stay invested for a long enough period to reap the rewards that markets can offer long term investors.

While an investor can withdraw capital from an investment bond at any time, the tax benefits of maintaining the investment for 10 years may encourage clients to take a longer-term view.

ii) When investors react to short term market conditions, they generally make the wrong decision.

While not advocating an attempt to time the market, for those clients fearful of a market correction and the impact of sequencing risk on their portfolio, investment bonds provide an easy way to switch between asset classes without incurring capital gains liabilities.

While there is no magic bullet to mitigate the risks associated with investment, the tax benefits of investment bonds can provide a means for you to help your clients manage their fears and avoid rash decisions. No other investment provides exposure to a range of underlying investment options with no tax liability on maturation after 10 years, and no capital gains tax liability when switching between investment options.

———-