Traumatic injury has far-reaching impact on individuals and families.

Unfortunately, a large number of Australian’s experience traumatic personal injury or illness every day. Many receive lump sum insurance or compensation payments, but are not always able to access financial advice appropriate for, and tailored to, their circumstances.

In this article, Zurich explores the incidence of traumatic injury and its far-reaching impact on individuals and families. The article examines how advisers can best serve those who have experienced trauma and includes insights from AFA Adviser of the Year winner, Charlie Fraser of Shadforth Financial Group, an adviser who has made it his business to focus on, and advocate for, such clients.

The statistics are alarming. On average, 20 Australians die each month at work[1] and in 2015-2016, there were 104,770 serious workers’ compensation claims[2]around the country. While a lot of attention is paid to road deaths, many more road users are left injured than are killed. While there were 344 fatalities in Victoria in 2016, a further 17,722 people were injured[3], some catastrophically so. There are many other causes of catastrophic injury – medical negligence, sporting injuries, assault, near-drowning and reckless behaviour, to name just a few.

Danger in the workplace

Workplace deaths frequently make the headlines and are increasingly the subject of shock tactic style advertising campaigns. Safe Work Australia has calculated that workplace injury and disease costs the Australian economy $61.8 billion[4].

Between 2000-2001 and 2014-2015, the median time lost for a serious claim rose by 33 per cent from 4.2 working weeks to 5.6; over the same period, the median compensation paid for a serious claim rose by 112 per cent from $5,200 to $11,000.

Worker’s compensation is typically paid at the worker’s current rate of earning for the time off work, plus medical costs. Lump sums may be paid for physical or psychological impairment and generally do not affect regular payments or expenses.

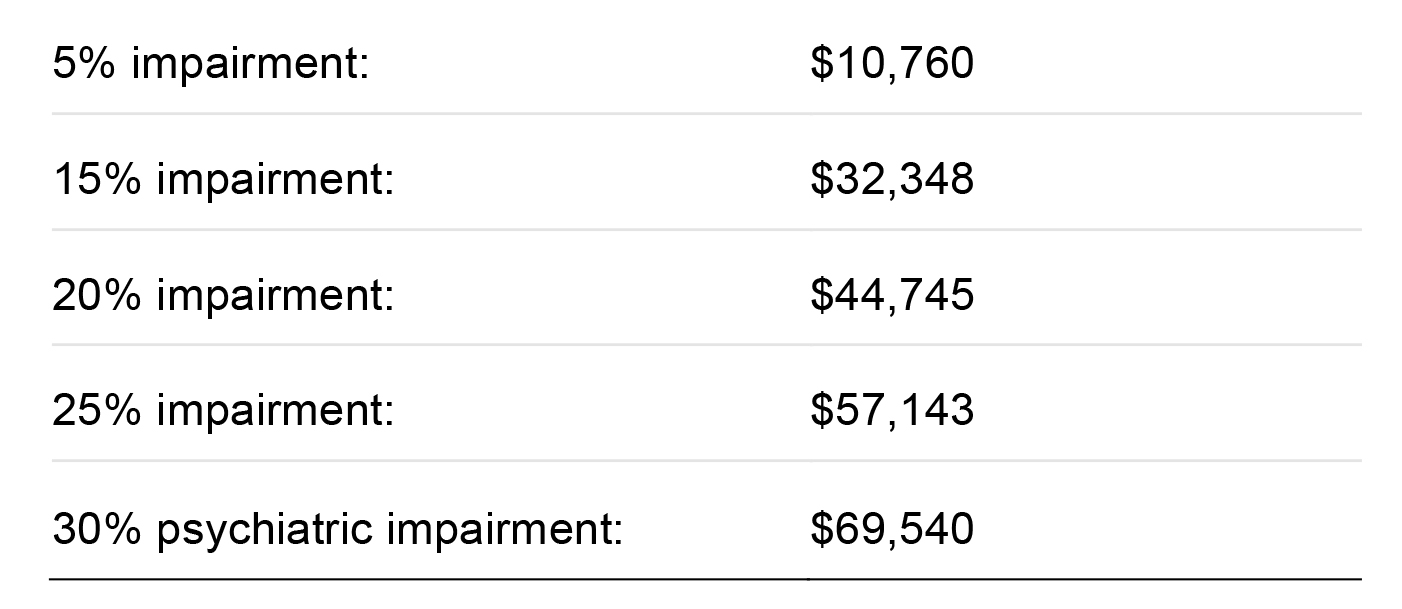

According to a law firm specialising in workplace injury[5], generally, a worker must have at least a 5% physical impairment as assessed by WorkCover, or a 30% psychiatric impairment. The compensation guide they provide prospective clients suggests the following:

More serious impairment, such as mesothelioma from working with asbestos, can attract higher settlements – on average, $250,000 to $400,000. Earlier this year however, a former James Hardie employee received a record settlement in excess of $1 million[6].

Carnage on the roads

While there are plenty of national statistics published about road deaths, information about injuries tends to be published on a state by state basis. A monthly bulletin published by the Department of Infrastructure and Regional Development showed 94 road deaths Australia-wide for October 2017, with a total of 1,217 deaths for the year ended 31 October 2017.

The data in table one has been compiled by Victoria’s Transport Accident Commission and looks at accepted claims over the past five years.

While the average reported[7] compensation payment to accident victims was $44,600, this varied by injury and the time taken to recover. The families of those killed in accidents receive, on average, compensation of $162,000; those who received catastrophic injury, such as quadriplegia or acquired brain injury, received an average of $3,441,700. This cohort will need sound financial advice as their earnings capacity would be significantly curtailed.

A range of studies have examined the financial impact of trauma resulting from accident or illness. In some cases, excessive out-of-pocket treatment costs can add to financial stress; however even where these costs are negligible, studies have shown that financial hardship is commonly prevalent after hospitalisation for serious illness or injury. Financial hardship affects more than the individual – it also impacts the broader family. How can financial advisers best support clients that have experienced trauma?

Best practice

For advisers with an interest in this relatively large cohort, it’s important to learn about the signs of trauma and how these might manifest for different people; this in turn can impact the decisions they make and behaviours they display.

Empathy and soft skills are important, as is resilience. As well as the trauma of the incident, clients and their families generally experience ongoing trauma – the understanding that life will never be the same and that the individual may never be the same physically, mentally or emotionally. The family often bears the brunt of the emotional side of caring for injured loved ones and it’s important for an adviser to be empathetic while retaining a degree of detachment; after all, they will see the worst life has to offer and continue to do what they need to do, day in and day out.

According to AFA Adviser of the Year, Shadforth’s Charlie Fraser, an adviser working in this area needs to take on enough of the family situation to make sure they are ‘sitting on their side of the table’, but be professionally removed enough to make the right decisions for that situation. It is particularly important not to become emotionally loaded.

Understanding the interface between different types of disabilities and how they are supported in the community is essential. It is critical to have a referral network that can understand the NDIS, provide support for physical, mental or emotional issues, know where people may get support regarding Centrelink and Medicare, and who can advocate for those clients and families unable to do it themselves.

Charlie believes the most important thing for an adviser to do is to identify the job each family is hiring the adviser to do. While some just want their money managed, others require broader assistance – whether to navigate government support, access private services, or to ensure they meet their trustee obligations. The key, according to Charlie, is to sit in front of each client and determine their needs and their capacity to make rational decisions about their money and situation.

Charlie’s first step is for a client and their family to meet with their wellbeing advocate, Sarah Grealy. Her key role is to get an in-depth understanding of the nature of the injury and determine what problems the family needs solved. This includes linking the family with an appropriate support network in their community.

Sarah ensures that the health and wellbeing of both the client and family is being taken care of and considers the costs associated with maintaining this. Wellbeing discussions are converted to financial recommendations, which may have to satisfy a relevant Trust Act or other legal requirements.

An important piece of advice from Charlie: don’t make clients reliant on you, don’t replace a dependency with a dependency. Identify issues and create a network of appropriate specialists around the client and their family.

Business ethics

While there is never a time that ethics does not play a vital role in providing financial advice, it is more important than ever when dealing with victims of trauma and their families.

From a financial advice perspective, any compensation payment is probably the only capital they will have for the rest of their lives. Anything that is inefficient, or costs the client but delivers no value, decreases their ability to live on this capital; accordingly, the requirement to satisfy the best interests duty is heightened.

For practices providing a wellbeing service, it is imperative not to provide, or be perceived to provide, any form of treatment. Rather, the focus should be to identify issues or problems to solve, and work with the client and their family to build and connect with a network of appropriate specialists.

Case study – an acquired brain injury from medical negligence

Charlie shared this story of a client with an acquired brain injury that resulted from a surgical procedure that did not go to plan. Please note: names and places have been changed for privacy reasons.

Robert, aged 40, was admitted to hospital for a surgical procedure where, due to medical negligence, he experienced a bleed in his brain. This was the equivalent of a stroke and resulted in a significant and permanent brain injury.

Robert and his wife June were a professional couple living in Adelaide. His brain injury resulted in a significant personality change, which caused distress to his wife and children. As a result, Robert moved into a care facility.

Robert had other medical issues, including diabetes, which required ongoing medical treatment. Despite his brain injury, Robert remained very articulate, but with little insight into his medical condition; this resulted in him being argumentative and difficult with medical professionals who increasingly refused to deal with him.

Charlie and Sarah became involved when Robert and June’s solicitor called them, after which Sarah started to work with June. The problem: she had been unable to access dental care for Robert – his tendency to stress meant he would often bite the dentist and because of his diabetes, the work could not be performed under anaesthesia. Sarah contacted the Dental Board of South Australia and, through this organisation, found a dentist willing to perform the work in Robert’s room at the care facility. This meant he was less stressed and less inclined to bite. Organising this took time and patience; two things that families in this situation are often short of.

The financial planning aspect of Peter and June’s was the easy part; a $10 million+ compensation payment invested to ensure financial security for the family. The ongoing support for Robert’s family is more time consuming. Sarah is paid by the client to act as a conduit between them and a range of care providers. Sarah speaks with June each week, so she can hear what’s required and what she can take off June’s hands.

Cases like this, where the client has capacity but no insight into his injury, can be particularly challenging for the family, care providers and other specialists.

Dealing with traumatic situations can be difficult; dealing with the victims of traumatic personal injury is full of complexity. For advisers who wish to provide services to the catastrophically injured, there are many more considerations than when servicing most client groups. There’s the family involvement, the family or third party acting as trustee, and a raft of service providers. There is also the range of government bodies that provide important support. For an adviser, it’s less about the technical aspects of financial planning and more about empathy, resilience, and developing the referral networks required to provide the necessary support and advice for the client.

———