While emerging market debt has evolved, investment approaches have lagged.

While the emerging market debt universe has evolved beyond recognition over the last two decades, the way that investors approach the asset class has been slower to evolve. It is time for investors to look beyond constrained benchmarks and toward a total return approach.

While emerging market debt has evolved, investment approaches have lagged

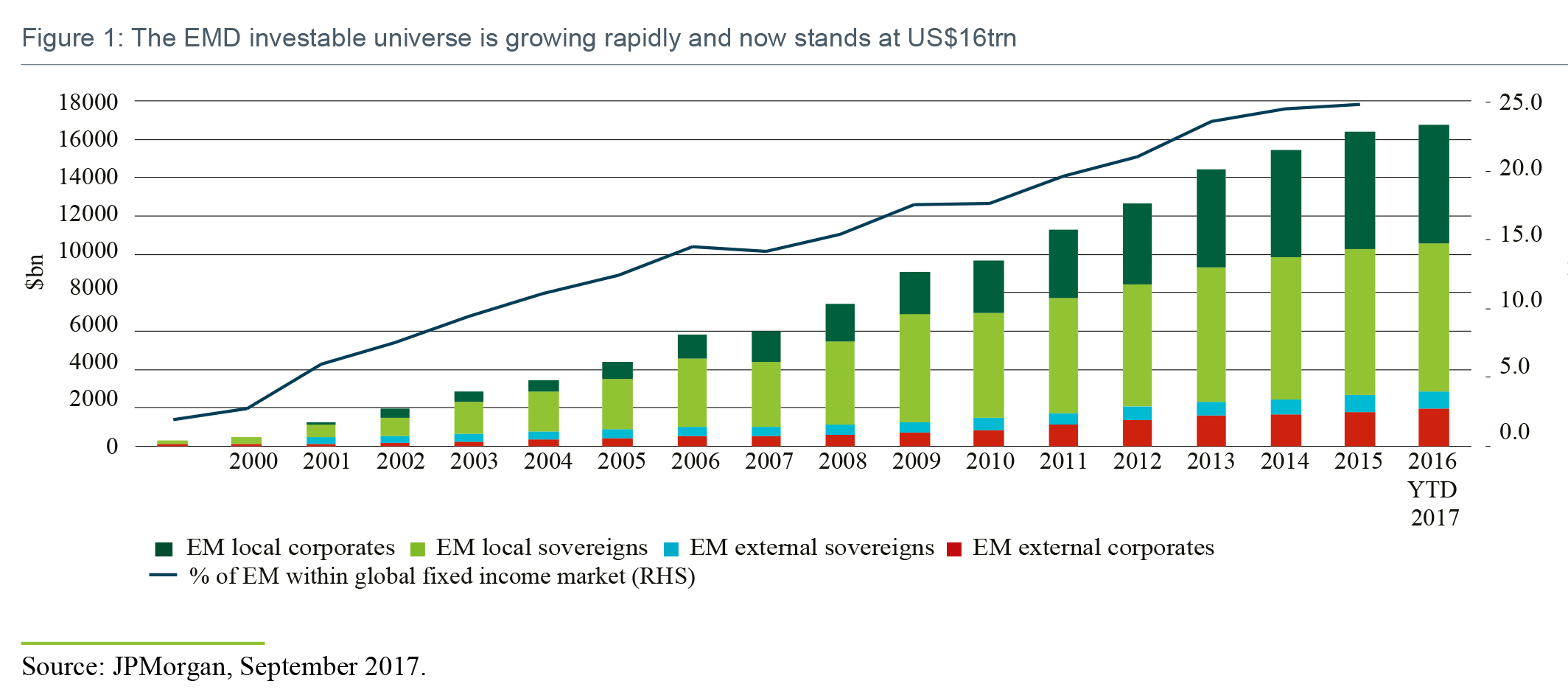

Emerging market debt (EMD) has come a long way since the turn of the millennium. The dramatic and structural improvement in macroeconomic fundamentals prompted a rapid expansion in both the breadth and depth of emerging market (EM) capital markets. And for EMD specifically, this transformation has changed the asset class beyond recognition. Today, the investable universe exceeds US$16trn (Figure 1) across local and hard currency sovereign and corporate debt. Whereas in 2000, EMD represented about 2% of global fixed income, today that proportion is closer to 25%. We believe the investment proposition has never been more compelling.

While the asset class has evolved, the same cannot be said for the methods investors use to gain exposure to it. The use of traditional benchmark-constrained long-only strategies, either single-sector or blended, continues to dominate investment allocations. However, such strategies suffer from several limitations that inhibit a manager’s ability to capture the most compelling beta opportunities:

- Static sector allocation: Benchmark-constrained blended EMD strategies have predefined weights to any combination of the three main EMD subsectors: local currency sovereign debt, hard currency sovereign debt and hard currency corporate debt. They are limited in terms of the degree to which the asset allocation can deviate from this neutral position. When allocation changes do occur, they tend to be incremental and While these blended approaches offer enhanced diversification benefits over single-sector strategies, they still remain constrained in terms of the manager’s ability to actively avoid segments of the EMD universe where the prevailing view is negative.

- Forced country exposure: Tracking-error and other constraints can also limit the extent to which benchmark- constrained strategies can deviate from prescribed benchmark country During times of idiosyncratic, country-specific stress – Brazil’s recent economic and political challenges, and the Russia/Ukraine Crimea crisis being two such examples – the best exposure might be outright country avoidance. Indeed, at the height of their respective crises, Brazil and Russia maintained close to a 10% weighting in the most widely followed EM local currency index. For benchmark-constrained strategies outright avoidance is often unpractical and costly in terms of risk budget usage.

- Drawdown capture: Single-sector benchmark-constrained EMD strategies have structural and indiscriminate long positions to the underlying beta of that This is clearly not an issue when on the right side of the credit or interest rate cycle, but when the market corrects, investors are exposed to the full drawdown impact with limited scope to mitigate.

There is a better approach

We believe total return EMD strategies represent the next phase in the evolution of EMD investing. At their core, these strategies can actively and rapidly allocate to the most attractive segments of the market while avoiding the least attractive, without being restricted by tracking error or traditional benchmark constraints. They seek to generate returns from both income and capital growth. While benchmark-aware, they are not benchmark- constrained and the manager typically enjoys large degrees of freedom to seek out the most attractive investment ideas and the best ways to access the structural beta of the market. Unlike a benchmark-constrained strategy where the benchmark serves as the starting point, a total return strategy effectively starts with a clean slate. Every exposure is an active decision.

What does ‘total return’ mean in practical terms

Dynamic sector allocation

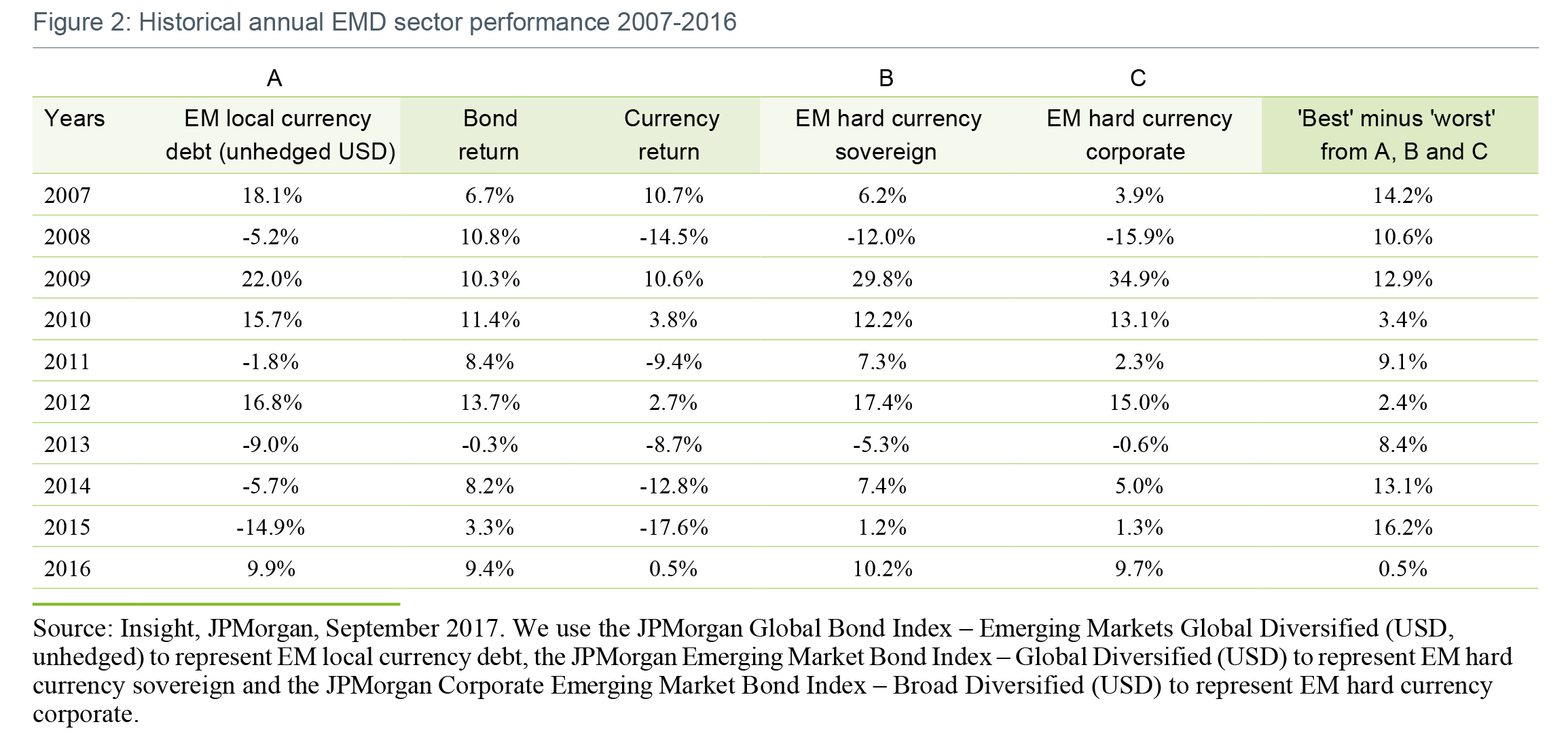

EMD is often couched in terms that infer homogeneity. As the performance table in Figure 2 demonstrates, however, EMD is anything but homogeneous. Annual performance divergence between each of the three key sectors can vary substantially in any given year. During the 2008 global financial crisis for example, hard currency sovereign and corporate credit underperformed, while local currency debt’s currency-driven negative return was softened by a strong positive return from the underlying bond exposures. In the aftermath of 2013’s ‘taper tantrum’ episode it was local currency debt’s turn to underperform, while corporate debt stood out as an oasis of relative calm. Meanwhile, in 2015, the magnitude of performance dispersion between the best and worst performing EMD sub-sectors was in excess of 16% (see final column, Figure 2).

These episodes demonstrate that being tied to a benchmark effectively removes a manager’s ability to avoid considerable drawdowns. In a blended total return EMD strategy, the manager can actively and decisively allocate between these sectors in response to evolving market conditions. When conditions are detrimental to a specific sector the manager retains large degrees of freedom to reallocate capital away from it and toward the more promising sectors within the opportunity set. In other words the manager can actively manage beta exposures away from ‘expensive’ or fundamentally deteriorating sectors towards ‘cheap’ or fundamentally improving sectors.

Complete country selection freedom

Being fully flexible and unconstrained, total return strategies typically have no intrinsic country exposure biases. When the manager’s view of a given country’s economic fundamentals is deteriorating, he or she can simply maintain a zero exposure to that country. Conversely when the view is positive, the manager can take a more concentrated exposure.

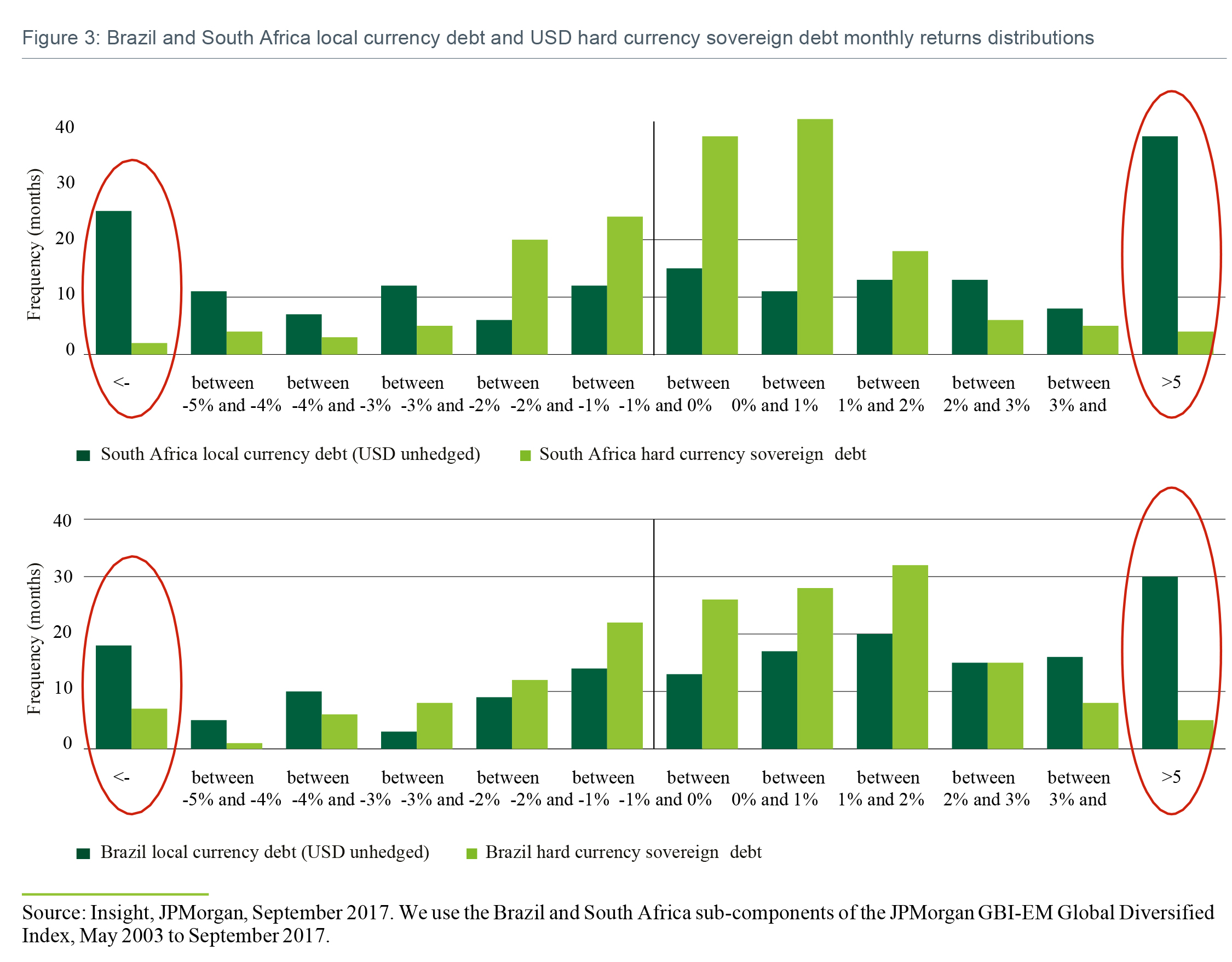

We believe such flexibility can add substantial value. Figure 3 presents monthly local currency sovereign (USD, unhedged) and hard currency sovereign returns for two major EMD countries, Brazil and South Africa. Brazil is an example of an EM country that was recently on the receiving end of negative political and economic headlines, while South Africa – itself not immune from political and economic noise – represents an example of a high-beta country historically prone to more extreme returns.

Strikingly, each returns distribution exhibits non-normal tendencies, characterised by ‘fat tails’ and a large degree of positive skew. South Africa local currency debt, for example, has produced 25 months of negative returns greater than -5% and 38 months of positive returns greater than +5%, with currency a key driver of performance. Monthly drawdowns in excess of -10% are also not uncommon. December 2015’s political roller coaster that saw President Jacob Zuma sack Finance Minister Nhlanhla Nene only to change his replacement within a week saw South African local currency debt assets sell-off -13%. Similarly, May 2013’s taper tantrum episode prompted a sell-off close to -15% during that month.

Brazil was a considerable underperformer at the height of its domestic economic and political woes in 2014 and 2015, when a deep recession and pervasive corruption scandal rocked the country. Brazilian local currency debt generated a negative cumulative return in excess of -30% over this two-year period.

Against such a negative fundamental backdrop, outright avoidance was perhaps the most prudent approach to Brazilian assets. For single-sector benchmark-constrained strategies a zero weighting would have been impractical, consuming a considerable amount of the manager’s risk budget usage through tracking error. At the time, Brazil’s weight in the widely followed JPMorgan GBI-EM Global Diversified Index was 10%. For a total return EMD strategy on the other hand, the manager would typically have had complete freedom to maintain a zero exposure to Brazil if the fundamental view warranted.

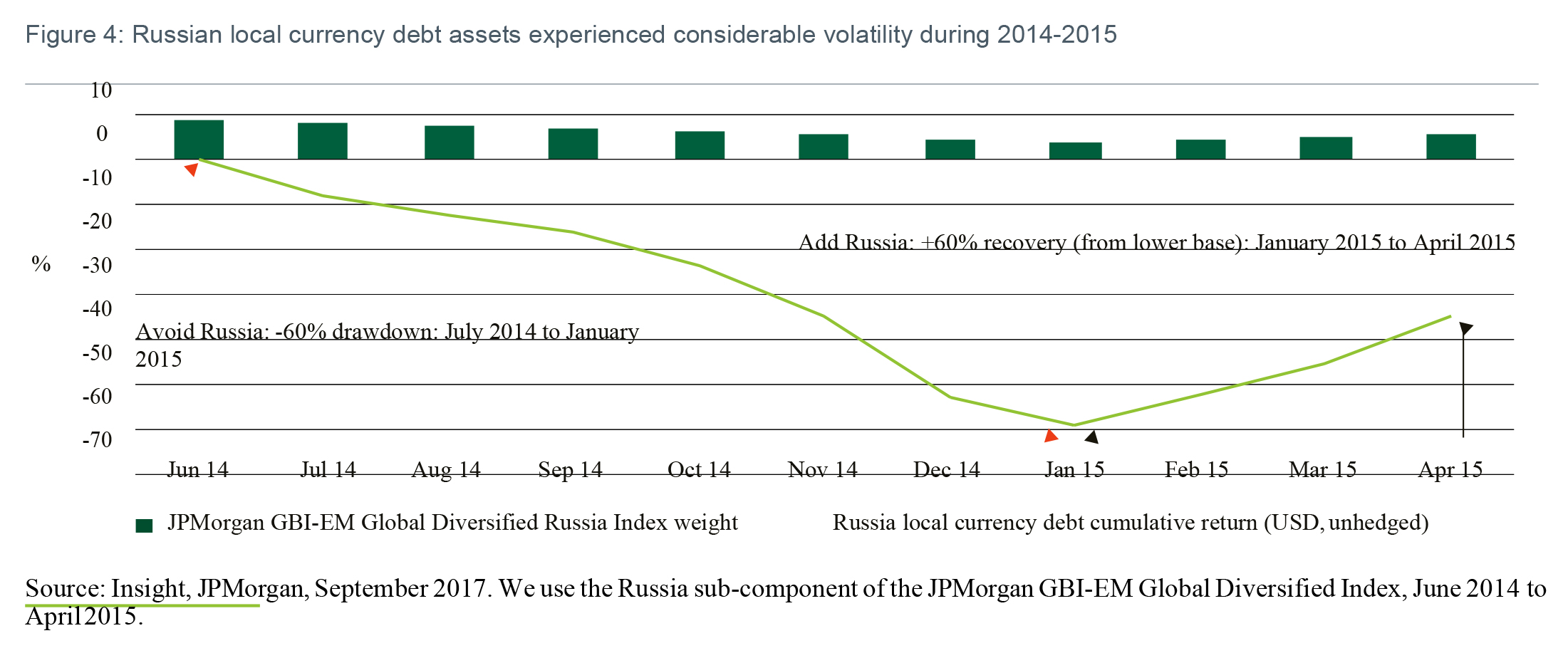

A similar narrative applies to Russia in late 2014, a time when the Crimea conflict was in full swing and oil prices were collapsing. Between July 2014 and April 2015, Russian local currency debt assets experienced tremendous volatility, declining close to -60%, before strongly rebounding +60% (from a lower base) in early 2015 (Figure 4). Russia constituted close to 10% of the JPMorgan GBI-EM Global Diversified Index just as the crisis was deepening, making it difficult to fully avoid for a benchmark-constrained investor. For a total return EMD manager who was concerned about the prevailing negative backdrop, a decision could have been made to completely avoid Russian exposure altogether.

As the value proposition became compelling once more in early 2015, the manager could have resumed a more concentrated exposure. As it was, Russia’s benchmark weight sank to just 3.71% in January 2015, the point which marked the trough of the sell-off and when a considerably larger exposure was probably justified.

When a market bottoms out and buying opportunities emerge, total return strategies have the potential to re-engage with concentrated, high-conviction allocations to capture the most compelling beta opportunities.

The end result

While the EMD investment universe has evolved and deepened considerably over the past two decades, most investors continue to access the asset class through traditional, benchmark- constrained approaches. In our view, such strategies suffer from several limitations that inhibit a manager’s ability to capture the most compelling beta opportunities and expose investors to unnecessary drawdown risks.

Ultimately, total return EMD strategies seek to achieve more structural beta exposure, but in a way that removes cyclicality, manages negative tail risks and focuses on only the most attractive investment ideas. In other words, they seek to focus on ‘cheap’ or fundamentally improving beta while avoiding ‘expensive’ or fundamentally deteriorating beta. They can do this through dynamic asset allocation and through including only the highest conviction country ideas. While benchmark aware, these strategies have high levels of flexibility and large degrees of freedom to achieve this outcome. As the EMD universe has evolved dramatically, these strategies represent the next phase in the evolution of EMD investing.

By Colm McDonagh, Head of Emerging Market Fixed Income

———-