Why you should rethink your bond strategy – beware the inflation overshoot

Gopi Karunakaran

As the tailwind of synchronised central bank support for asset prices subsides, conventional fixed income strategies aiming for true risk diversification may struggle to achieve their objectives, says Ardea Investment Management portfolio manager, Gopi Karunakaran.

Conventional thinking has it that bond and equity prices have an inverse relationship: When a “risk off” scenario such as a recession occurs, capital flight to safety, together with the potential for interest rate cuts, causes bond prices to rise. In this way bond holdings can provide risk diversification against falling equity values.

However, Mr Karunakaran is urging investors to re-evaluate the widely held view that governments bonds are inherently defensive and risk diversifying in the current economic climate.

For the first time in years, the largest economies in the world are all growing and finally allowing central banks to look beyond monetary stimulus, despite still low inflation. If the consensus view of improving economic growth, contained inflation and gradual central bank policy normalisation does play out, bonds can provide stable income while exposing investors to risk of modest capital losses from rising interest rates (duration risk).

“Even in this scenario, the current combination of very low yields and term premia, means bond holders are being poorly compensated for bearing duration risk. The issue is compounded for passive bond investments as benchmark index duration is longer, therefore riskier, while average yields have declined and there is asymmetric risk of capital losses from rising interest rates,” he said.

“But if nascent inflationary pressures become more established, this would quickly shift focus to fear of inflation overshooting, forcing aggressive, unexpected and disruptive normalisation of monetary policy. Bonds would then become the catalyst for a broader sell-off in other asset classes, rather than acting as a defensive risk diversifier,” he added.

“We got a small taste of what such unanticipated policy tightening can do to markets during the ‘taper tantrum’ in 2013 when US Federal Reserve chair Ben Bernanke unexpectedly announced the possibility of reducing the Fed’s bond buying program. This caused bond prices to drop sharply and trigger a sell-off in equities. The negative correlation between bonds and equities has been less reliable in the years since.”

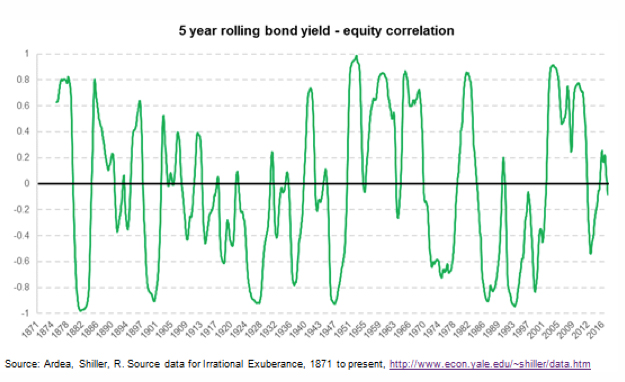

In fact, longer term data shows that bond-equity relationships are unstable, tending to be impacted by inflation and interest rate paradigm shifts. While such paradigm shifts are easier to identify in hindsight, there are enough early indicators suggesting we are in the initial stages of one.

Mr Karunakaran said that irrespective of whether this scenario plays out, the conclusion is the same –the assumed negative correlation between bonds and equities is not as reliable as hoped for.

“The implication for portfolio construction is clear. Re-evaluate the conventional assumption that owning government bonds is inherently defensive and risk diversifying. At best, it’s an expensive choice and at worst, it won’t work,” he said.

“There’s more to fixed income than just buying and holding bonds. It is an asset class with a wide range of instruments, strategies and return sources that can be exploited to achieve genuine risk diversification. For example, the same factors that distorted bond market valuations have also created relative value pricing anomalies, underpriced volatility, skewed risk premia and cheap tail risk opportunities.”

“Fixed income can still diversify portfolio risk, but only if you choose the right strategy,” he added.