At a time when life expectancy is increasing, your clients may want to take advantage of planning for the best future possible.

Australians are living longer but many are failing to plan for it, new research from National Seniors Australia shows. The report, Hope for the best, plan for the worst? Insights into our planning for a longer life, suggests that many are resigned to outliving their savings. At a time when life expectancy is increasing, Centuria examines investment strategies outside of superannuation your clients may want to take advantage of planning for the best future possible.

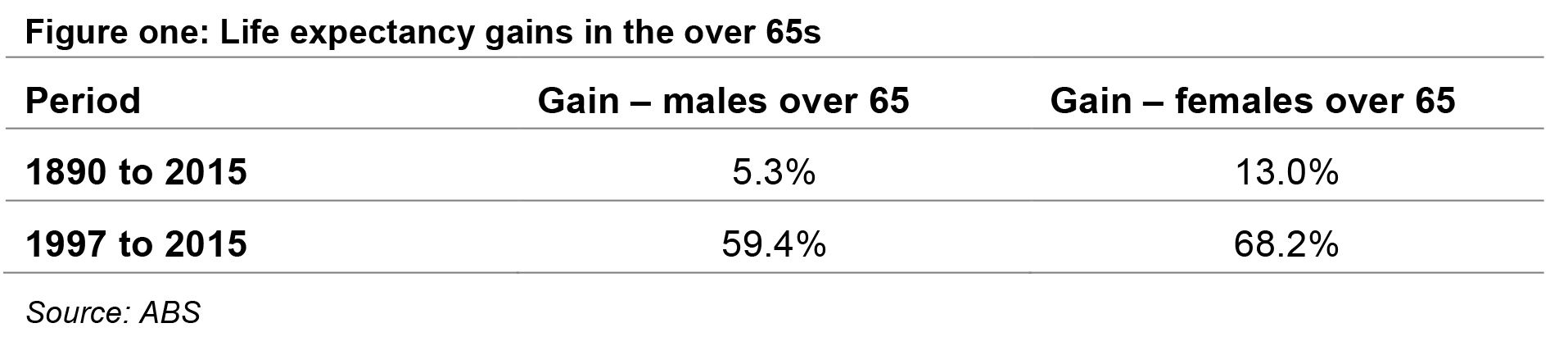

A better standard of living – good healthcare, nourishing food, access to dental care, exercise, housing – all contribute to the longevity being enjoyed by the Australian population. According to the Australian Bureau of Statistics (ABS)[1], such improvements, coupled with developments in social and economic standards, have resulted in larger gains in life expectancy over time for those aged 65 years and over – the traditional retirees. As illustrated in figure one, the gains in life expectancy over the last 20 years have been considerable.

The Treasury’s 2015 Intergenerational Report found that Australians will live have one of the longest life expectancies in the world; in 2054-55, life expectancy at birth is projected to be 95.1 years for men and 96.6 years for women, compared with 91.5 and 93.6 years today.

The structure of Australia’s population will also continue to change, with a greater proportion of the population aged 65 plus. This not only has implications for Australians saving for retirement, but also for the government, which supports those with insufficient savings.

The Productivity Commission Government Services Report, released January 2018, revealed that governments (state and federal) spent $17.4bn on aged care services in the 2016-17 fiscal year – a number that will surely grow as Australia ages, particularly if retirement savings aren’t sufficient to cover an addition twenty-five plus years post retirement.

Aware…but are they planning for it?

As illustrated in figure two, 85% of people aged 50+ surveyed by National Seniors Australia said they were aware that ‘life expectancy at age 65 had increased by around 6 years over the last 30 years’.

The research found that what mattered most to people about their finances in retirement was having regular, constant income to meet their essential needs. While the majority were aware of living longer, 22% of survey participants disclosed that they ‘hadn’t planned at all’ for an increasing lifespan, and only 50% had made financial plans for a longer life[2].

One of the more interesting findings was the median asset balance – of the 5,770 Australians aged 50+ surveyed, the median retirement savings balance was $300,000[3]. This is significantly lower than the Association of Superannuation Funds (ASFA) estimates of $545,000 ($600,000 for couples) for a comfortable lifestyle to age 90.

The ASFA retirement standard suggests that a single person would need $43,665 per year and a couple $59,971 to enjoy a ‘comfortable’ lifestyle. Retirement savings of $300,000 would be unlikely to generate those cash flows over the course of a ‘normal’ retirement, which can now span 25+ years.

Meanwhile, the 2016–17 Multipurpose Household Survey (MPHS)[4] undertaken by the ABS examined retirement intentions and retirement funding. The research found that of the 3.9 million persons in the labour force who indicated that they intended to retire, 40% did not know the age at which they would retire (36% of men and 44% of women). Those who did have a planned age of retirement fall into the categories:

- 20% intend to retire 70 years and older (22% of men and 18% of women)

- 50% intend to retire between 65 and 69 years (53% of men and 47% of women)

- 23% intended to retire between 60 and 64 years (19% of men and 27% of women)

- 7% intended to retire between 45 and 59 years (6% of men and 8% of women).

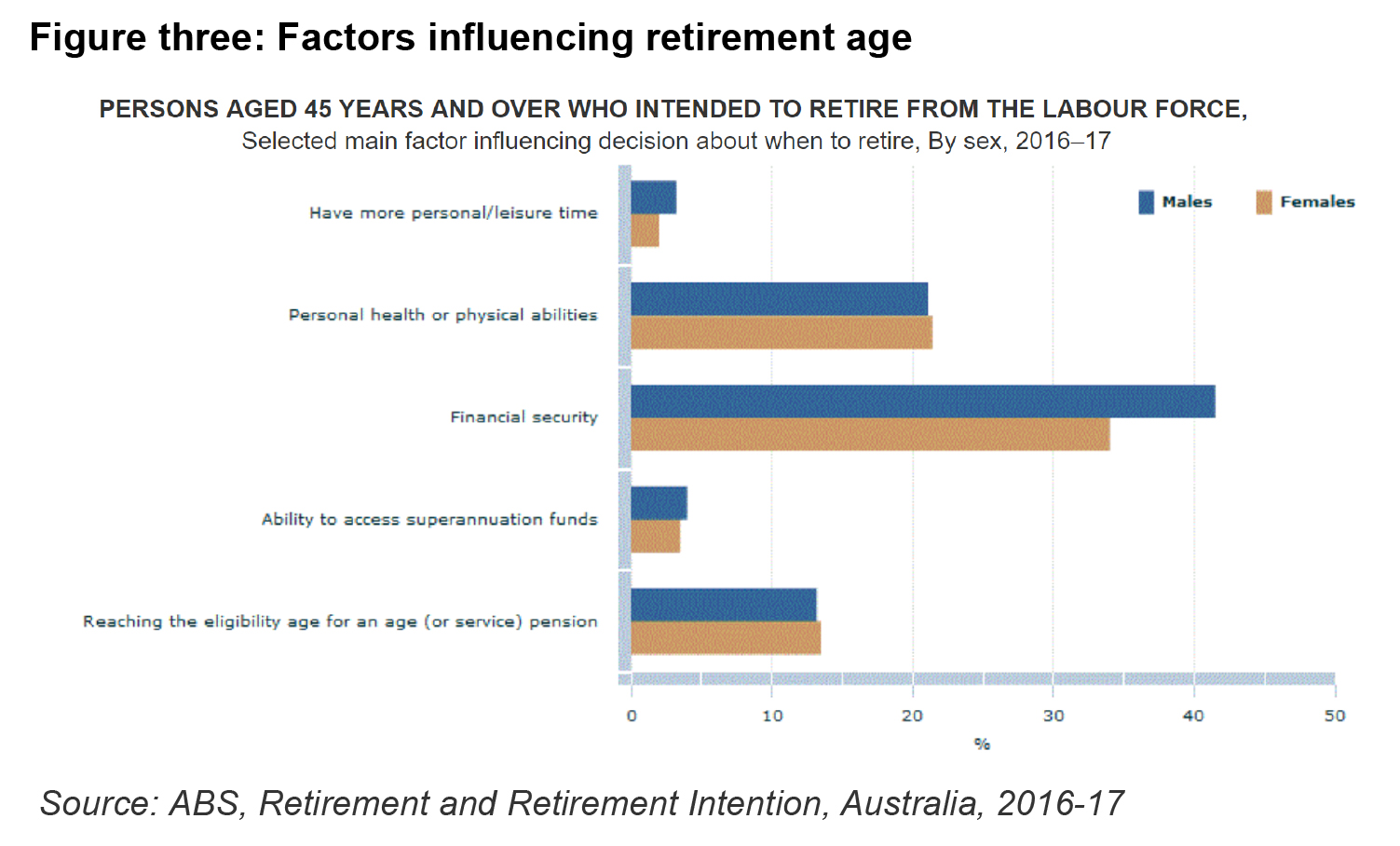

The average age at which persons intended to retire was 65 years (65.5 years for men and 64.4 years for women). These retirement intentions are evidently driven by issues of financial security, as illustrated in figure three.

So, Australians are living longer, are concerned about financial security but typically, not all that good at planning for their post-retirement lifestyle – particularly when it comes to the later years, which are often characterised by the need for increased spending on medical care or residential facilities. National Seniors Australia’s research found the intention to spend retirement income paid little or no attention to later old age where there can be significant costs.

Last year’s changes not so super

The changes to superannuation introduced on 1 July 2017 have made it harder for people, particularly those approaching retirement, to load up their super savings and take advantage of super’s tax effective environment.

From that date, the federal government imposed limits on the amount that can be contributed to super in each financial year before extra tax is payable. For those clients who haven’t yet reached the $1.6 million transfer balance cap, they have a $25,000 concessional cap and a $100,000 non-concessional cap per annum. If they are close to retirement and looking to fund an additional 25+ years of a ‘comfortable’ lifestyle, they may need additional savings.

How then, can a client who needs to build up retirement savings, do so in a tax effective way?

Investment bonds – a tax effective way to save for retirement

An investment bond is a tax effective structure. Like superannuation, tax is paid within the investment bond rather than personally by the investor. The maximum tax paid on the earnings and capital gains within an investment bond is 30%, although franking credits and tax deductions can reduce this effective tax rate. This, along with the following benefits, make investment bonds an attractive investment option, particularly for high income earners.

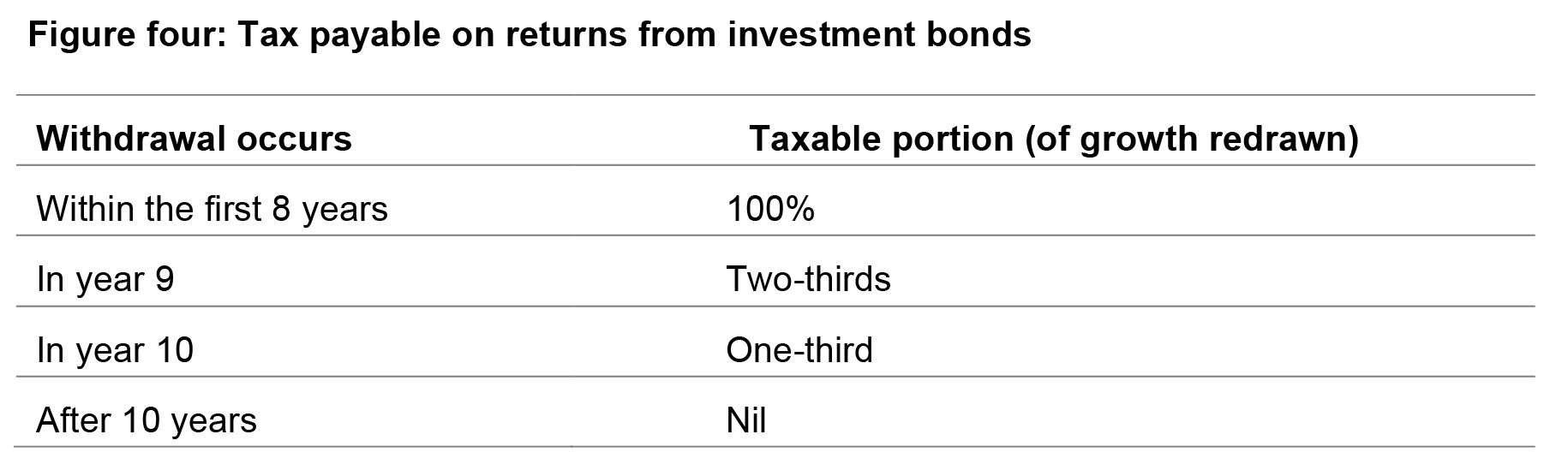

#1 Tax free after 10 years

If an investment bond is held for 10 years, no personal tax is payable by the investor. However, if the investment is redeemed within the first 10 years, the investor will pay tax on the assessable portion of growth as shown in figure four.

Investment bonds could be established to mature at different milestones in retirement – five years in, seven years in, 10 years in…this way, your client can be sure of regular sums at regular intervals to supplement their superannuation and fund a comfortable retirement and allow for changing needs at different life stages.

#2 No limit on contributions

To contribute to superannuation an investor needs to meet eligibility rules. This requires the investor to be under age 65 or, if aged 65 to 75, they need to meet a work test. If eligible, contribution caps will limit the amount of contributions that can be made to superannuation.

There is no limit on the amount that can be invested to establish an investment bond, and investors can make subsequent investments up to maximum of 125% of the previous year’s contribution without restarting the ten-year period. Investors can choose to start a new investment bond if higher amounts are to be subsequently invested – or if they would like to target specific maturity dates throughout their retirement.

Investment bonds can provide a tax effective means of investing and avoid excess contributions tax that may otherwise apply in the case of superannuation contributions post 1 July 2017.

#3 No access restrictions

Unlike superannuation investments, investment bonds are not subject to preservation. This means that investors can access savings before age 55; this makes investment bonds an ideal vehicle if a client is looking to fund an early retirement and doesn’t want to incur the penalties associated with early access to superannuation.

#4 Tax free for beneficiaries

Investment bonds provide investors with the freedom to nominate anyone as a beneficiary in the event of their death. Beneficiaries are not limited to ‘dependants’, as is typically required for superannuation investments and importantly, receive the proceeds of an investment bond tax free, regardless of the length of time it has been invested – no need to wait for the 10 years to be up.

When compared to other investment vehicles, investment bonds are an ideal means through which clients can save in a tax effective manner to supplement their superannuation. Using investment bonds, your clients can build up savings to fund each stage of retirement, to ensure it is enjoyable and comfortable, however long they may live

———

[1] 3302.0.55.001 – Life Tables, States, Territories and Australia, 2014-2016

[2] Hope for the best, plan for the worst? Insights into our planning for a longer life – February 2018

[3] Hope for the best, plan for the worst? Insights into our planning for a longer life – February 2018

[4] http://www.abs.gov.au/ausstats/[email protected]/mf/6238.0

———