In the past year there have been several changes that may have impacted your clients’ estate planning strategies

There’s nothing certain in life but death and taxes, so the adage goes…however, another certainty is change – particularly when it comes to the financial services regulatory landscape.

In the past year there have been several changes that may have impacted your clients’ estate planning strategies, and more change is in the wings. In this article, Centuria explores those changes and the potential impacts for clients.

The importance of estate planning

Regardless of change, nothing impacts the importance of a sound estate plan. While a financial plan focuses on creating and preserving wealth, an estate plan defines how an investor wants their assets to be managed during their lifetime, and importantly, how they want them disbursed after death. The plan also deals with the weighty decision as to who will look after your clients’ estate.

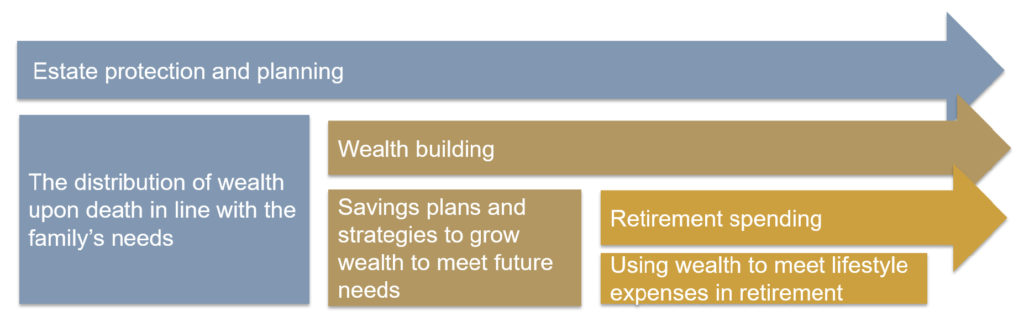

Estate planning should be considered early in the financial planning process. As illustrated, the phases of the financial planning and estate planning processes overlap. For example, wealth building plays a significant role throughout retirement to help manage longevity and inflation risks.

Poor estate planning can have a significant impact on the value of the estate and the beneficiaries:

- the estate could be distributed to unintended beneficiaries

- high legal fees could be incurred to collect all the assets

- any disputes can result in lengthy delays in accessing estate proceeds

- erosion of wealth due to tax implications, reducing the value of the estate.

Such consequences can result from having no estate plan, or when estate protection and planning is considered as the final phase, once investment decisions have been made.

Change and its impact

A range of changes, both implemented and proposed, can and will impact estate planning. This reinforces the fact that estate planning is not a ‘set and forget’ strategy, rather it’s one that should form part of your regular client review.

Super changes 2017

Last year the Federal Government introduced a range of changes; these changes not only had consequences for your clients’ retirement, but also for their estate planning.

1. The transfer balance cap of $1.6 million on retirement balances

Following the introduction of these amendments, an individual can now transfer only $1.6 million into retirement phase accounts; any excess had to be withdrawn and invested elsewhere. The changes not only impose limits on the amount a person can have in their superannuation retirement pension account, but also limits the amount a member can receive from their deceased spouse’s pension account. This is because the deceased’s pension now counts towards the surviving spouse’s transfer balance cap, something which has to be considered when developing an estate plan.

2. Changes to concessional and non-concessional contribution caps

Three key changes came into effect on 1 July 2017:

- a reduction in concessional (pre-tax) contributions from $30,000 to $25,000

- higher concessional caps for the over 50s no longer exist

- the annual non-concessional (after-tax) contributions cap has been cut to $100,000; it is only possible for investors to make non-concessional contributions if their super balance is less than $1.6 million.

3. Lowering of the income threshold from $300,000 to $250,000 for 30% rather than 15% tax on contributions

This means that any Australian with an income of $250,000 p.a. or more now pays 30%, double the usual tax rate of 15%, on contributions into super.

4. The tax-exemption for transition to retirement pensions (TRIP) will be removed

The upshot of this change is that super fund earnings supporting a transition to retirement pension is no longer be tax-exempt.

These changes have particularly impacted higher net worth individuals and have seriously curtailed the ability to contribute lump sums into super. Finding an effective wealth building vehicle that also provides estate protection and estate planning opportunities is important.

Proposed changes to super

It seems that last year’s changes to super may not be the last. A recent keynote address[1] delivered by Senator Hon Kristina Keneally at the FSC BT Political Series Breakfast suggest a Labor government has several policies directly targeted at superannuation. As with the changes introduced in 2017, each has the potential to impact your clients’ retirement and estate planning strategies. The changes flagged by Keneally include:

- Changes to the dividend imputation system, which have already received significant media attention.

- Discretionary trust reform – discretionary trusts are used by many investors as estate planning vehicles. While the quantum of change has not yet been declared, it’s a structure that’s on the ALPs radar.

- Changes to catch up concessional contributions – the speech mentioned opposition to these measures, however it’s not clear whether catch up contributions will be reduced or eliminated.

- Lower the non-concessional contribution cap further, from $100,000 to $75,000

- Lowering the income threshold further, from $250,000 to $200,000 for which 30% rather than 15% tax on contributions is paid.

While there’s no timeline in place, and of course, an election to occur and legislation to be passed, it’s reasonable to expect further change, whichever party is elected.

The ‘Marriage Amendment (Definition and Religious Freedoms) Act 2017’

Changes to the Marriage Act late last year allow same sex couples to marry; it also recognises those marriages legally enacted overseas. In all Australian states and territories, marriage renders any previous Will invalid, and in all but Queensland, also nullifies Powers of Attorney.

If a new Will is not written once the couple has married, in the event of the death of one partner, they will be deemed as being intestate. This may result in that person’s assets being distributed to unintended beneficiaries, rather than in line with the intentions of the deceased.

Prior to the change in the Marriage Act, many same-sex couples in long-term relationships had drawn up legal and financial agreements to cover all eventualities; such agreements should also be reviewed to ensure their validity and that the estate planning needs of the couple are met.

Investment bonds and estate planning

An investment bond is an insurance policy, with a life insured and a beneficiary; however, it operates like a tax-paid managed fund. And as with a managed fund, you can make recommendations to your client from a broad range of underlying investment portfolios. These typically range from growth-oriented assets, such as equities, to defensive assets such as fixed interest. They can also include other asset classes and combinations of assets.

Tax effective

Importantly for estate planning, an investment bond is a tax effective structure. With most other investment structures however, when a beneficiary takes an inheritance in their name, tax is generally payable on income generated from the inheritance at their personal marginal tax rate.

With investment bonds, tax is paid within the investment bond rather than personally by the investor. The maximum tax paid on the earnings and capital gains within an investment bond is 30%, although franking credits and tax deductions can reduce this effective tax rate. This makes them an attractive investment option for high income earners.

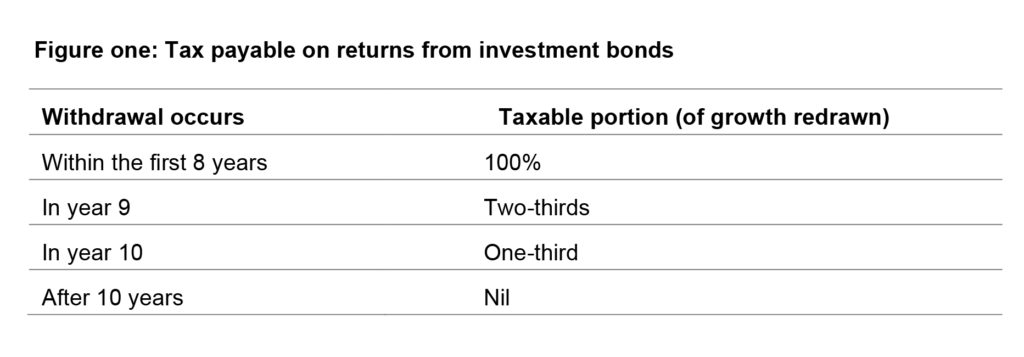

A key feature of investment bonds is that if the investment is held for 10 years, no personal tax is paid by the investor. However, if the investment is redeemed within the first 10 years, the investor will pay tax on the assessable portion of growth as shown in figure one.

Transfer of ownership

The ownership of the investment bond can be easily assigned or transferred at any time. The original start date is retained for tax purposes. This may not be achieved within a company structure without creating tax liabilities.

Beneficiaries

Investment bonds provide investors with freedom to nominate anyone as a beneficiary in the event of their death. They fall outside of the estate, so are not distributed according to the will, nor are they affected if the owner dies intestate.

Tax-free to nominated beneficiary/ies

Investment bonds are paid tax-free to the nominated beneficiary/ies. Depending on the age and life stage of the beneficiary/ies, the funds can then be:

- reinvested in a new investment bond

- transferred into the recipient’s retirement phase superannuation account, as long as it will not exceed the $1.6 million transfer balance cap

- used to make additional superannuation contributions up to the recipient’s relevant contributions cap.

Investment bonds versus other investments

An investment bond may provide greater simplicity and control over death benefits than other investment products such as unit trusts, shares or term deposits.

Upon death, most investment products form part of the estate and may be caught up in any actions taken against the estate. It is also left to the executor to make decisions about the distribution in accordance with the terms of the will.

These actions usually cannot be undertaken until probate or letters of administration are obtained, which means the entire process can take months or even years if the estate is complicated or being disputed.

Once distributions are made, tax may be payable by either the estate (if assets are sold) or the beneficiary when assets that are received in-specie from the estate are subsequently sold.

In contrast, the death benefits from an investment bond can be directed to a nominated beneficiary. Investment proceeds are paid tax-free to dependant and non-dependant beneficiaries, regardless of how long the investment has been held.

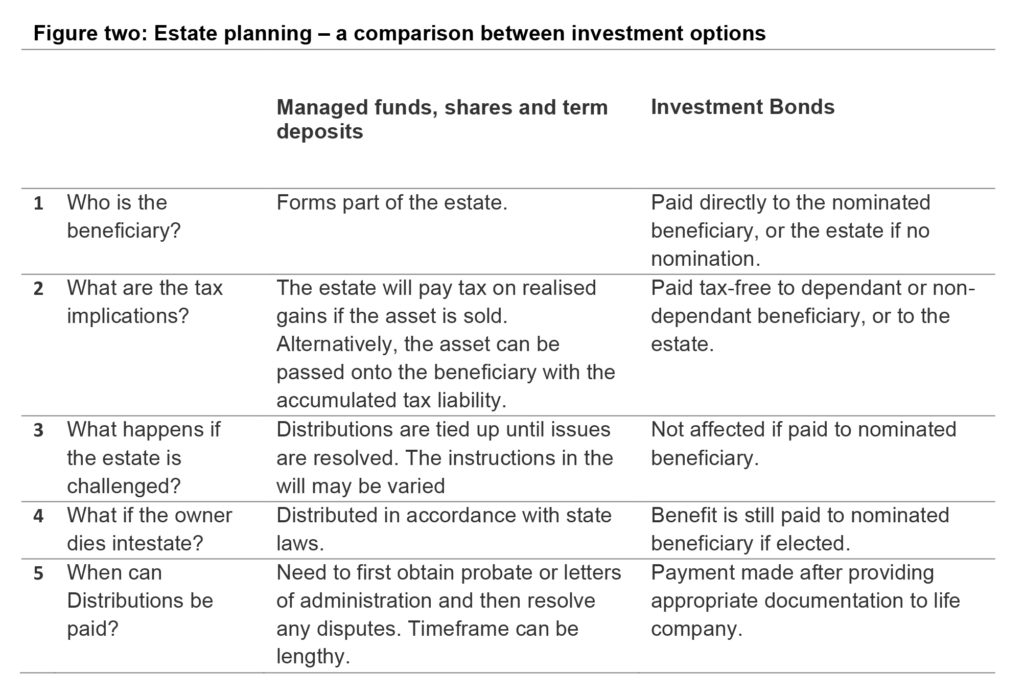

Building wealth in an investment bond may reduce the risk of disputes over estates and enable the benefits to be paid more quickly. The advantages of an investment bond in an estate protection and planning strategy are summarised in figure two.

Blended families

Investment bonds are suitable for blended families that have separate estate planning needs, as outlined in the following case study. The investment structure gives parents certainty that their nominated beneficiaries will receive their bequest without challenge from other family members.

Case study – a blended family

Lisa (67) and Andrew (72) are married. For both it is their second marriage, and each have children from their first marriage; Joan has three children and Brian has two.

Lisa’s main estate planning issue is to leave her non-superannuation assets, which were accumulated during her first marriage, to her three children. She considers investing her non-super assets into an investment bond, with those three children as beneficiaries.

Lisa remains the owner and life insured, and because investment bonds provide the flexibility to withdraw funds at any time, she continues to have access to the funds if necessary.

If Lisa is alive when the investment bond matures, she can reinvest the proceeds for a further ten years, knowing that upon her death, the funds are paid tax free to the beneficiaries, her three children.

While unit trusts, shares or term deposits are traditional options for wealth building, they form part of the estate upon death, and distribution can be complex and open to dispute from other parties, such as Andrew’s children. Investment bonds however, provide greater simplicity and control over death benefits.

For those concerned with estate planning, investment bonds are structured to allow investors to create certainty with respect to their wishes about passing on wealth. Investors can nominate beneficiaries who then receive benefits directly and free of personal income tax liability. Investment bonds enable your clients to combine wealth building and estate planning to ensure they get the right assets, into the right hands, at the right time, irrespective of regulatory change.