Is infrastructure a bond proxy?

Interest rates heading north have significant implications for global equity markets.

Inflation looks to be very slowly emerging from a long slumber and interest rates are heading north. This has significant implications for the world’s economy and global equity markets.

For global listed infrastructure in particular, the prevailing ‘wisdom’ is that infrastructure as an asset class is no more than a ‘bond proxy’. The rationale is that, just like bonds, infrastructure is a yield story – in particular, a relative yield story against bond yields. Therefore, if interest rates rise and bond prices fall, so too must global listed infrastructure asset prices in order to retain the same relative relationship between the dividend yield and the bond yield.

Greg Goodsell, Global Equity Strategist and Chris James, Investment Analyst from 4D Infrastructure, investigate this issue and conclude there is much more to the story than meets the eye. The answer lies in looking more closely at infrastructure as an asset class, its constituents and their characteristics, and understanding that, with active management, an infrastructure portfolio can be positioned to perform well in a rising rate environment.

The first step in understanding the potential implications of a rising interest rate environment for an infrastructure portfolio is to break down the infrastructure asset class into its two broad constituents: User Pay and Regulated Utilities.

1. User Pay vs Regulated Utility assets: a key distinction

User Pay

By their very function, User Pay assets are geared to capture GDP growth and wealth creation. Typical User Pay assets are toll roads, airports and ports, whereby the user pays to use the asset. These stocks have a direct positive correlation with GDP growth (volumes) and often have built-in inflation protection mechanisms in their business models (tariffs). As interest rates/inflation increase over time, these protection mechanisms begin to kick in and positively impact earnings. This is then reflected in the relevant stock price and performance.

In addition, management at these companies have generally been actively locking in medium to longer-dated borrowings over the past several years during this extraordinarily long period of very low global interest rates. As a result of these borrowings, higher interest rates do not have an immediate earnings impact.

Regulated Utilities

In contrast Regulated Utilities, such as electricity, water and gas providers, are more immediately adversely impacted by rising interest rates/inflation because of the regulated nature of their business. For a regulated utility to recover the cost of higher inflation or interest costs, it must first go through its regulatory review process. This involves making submissions to the regulator arguing that prevailing economic conditions have changed and they should be entitled to recover those increased costs via increased rate charges to their client base. While a regulator is required to have regard for the changing cost environment the utility faces, the process of submission, review and approval can take some time. In addition, the whole environment surrounding costs, household rates and utility profitability can be highly politically charged. As a result, both the regulatory review process and the final outcome can be quite unpredictable.

2. How do User Pay & Regulated Utility assets perform during rising interest rates?

Having established the premise that User Pay assets offer some protection from rising interest rates and inflation while Regulated Utilities are more vulnerable, we can test this thesis by examining how these two distinct asset sub-sectors have performed during previous periods of rising interest rates. We therefore look at two scenarios:

- how User Pay and Regulated Utility stocks performed following: a) a rising US Federal Funds (Fed Funds) rate, and b) rising 10-year US Government Treasury Bond (T-Bond) yields; and

- what impact a 1% increase in the assumed bond yield (and hence inflation rate) has on a User Pay stock’s expected earnings. We explore this question via a case study on the Australian toll road operator Transurban Group (TCL AU).

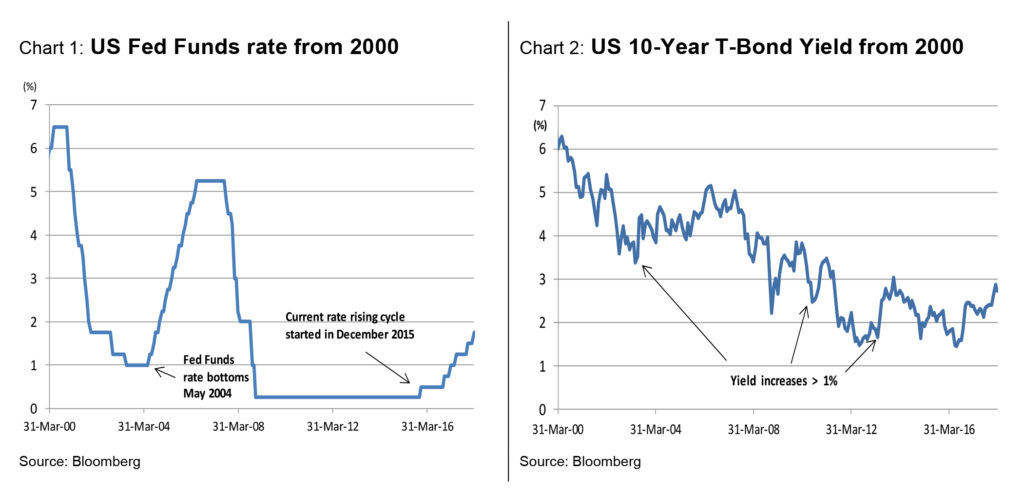

Rising interest rate cycles in the US since 2000

Since 2000 there have been two Fed Funds rate hike cycles (Chart 1) and three periods during which the US T-Bond yield rose by more than 1% over consecutive months (Chart 2).

3. Can User Pays outperform in periods of rising interest rates?

To test the thesis that User Pay assets can outperform in periods of rising interest rates/inflation, we:

- segregated 4D Infrastructure’s investible universe[1] of 327 global listed infrastructure stocks into User Pays (141 stocks: the ‘4DUP’ index) and Regulated Utilities (186 stocks: the ‘4DUts’ index);

- and then examined how these two indices, as well as the S&P Global Infrastructure Index (‘S&PI’), performed versus the MSCI World Index (‘MSCI’ – as a proxy for global equity market performance) during the periods identified above – namely, a rising Fed Funds rate and rising US 10-year T-Bond yields.

To better understand the performance behaviour of the indices, we separate performance of the first six months and second six months (i.e. months 7–12) after rates start increasing. The results of our analysis are also illustrated in the attached charts.

4. Rising rates 1: Two Fed Fund rate hike cycles since 2000

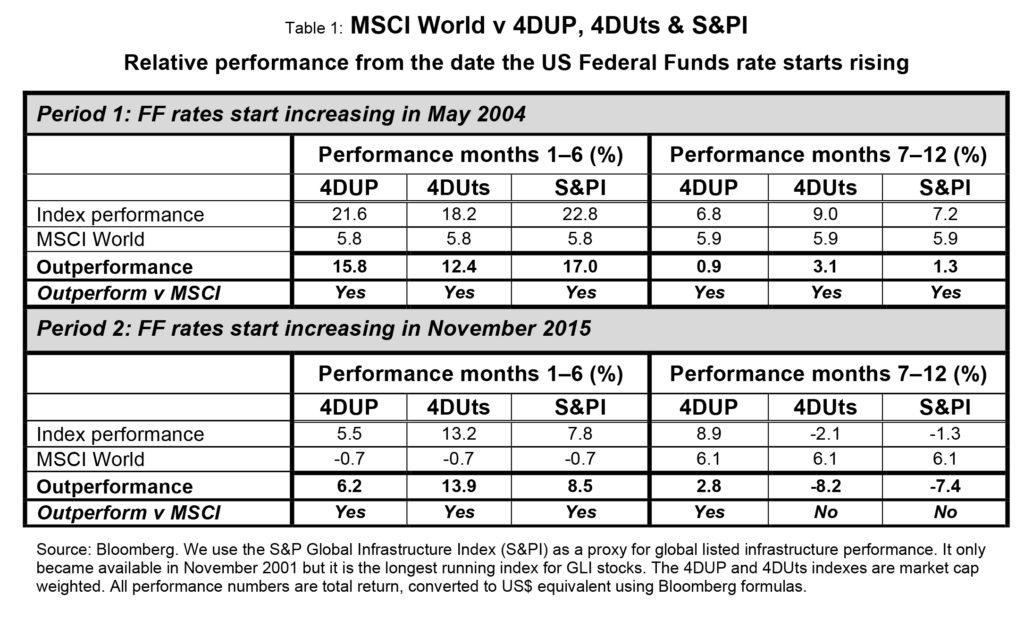

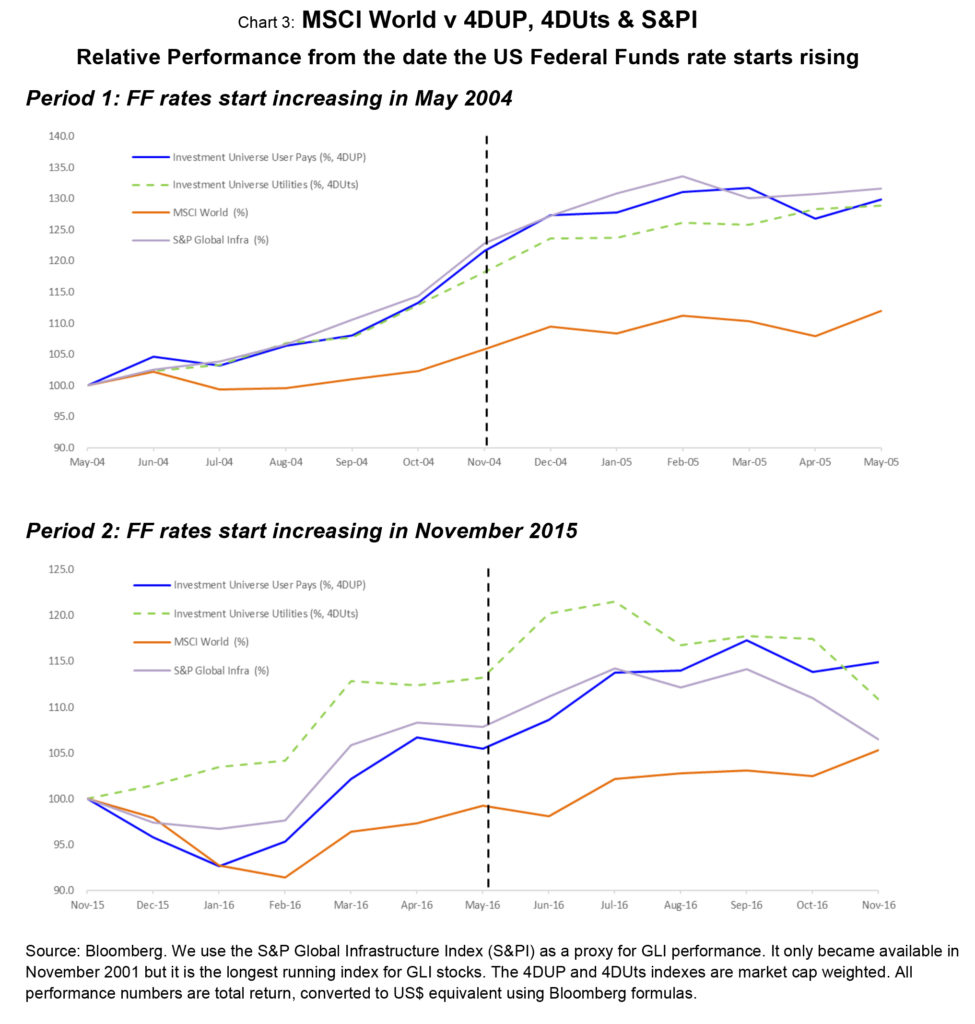

As shown in Chart 1, since 2000 there have been two periods in which the US Fed Funds rate rose by more than 1% over consecutive months. The performances of our infrastructure indices vs the MSCI over these periods are shown in Table 1 below.

Conclusion re Fed Funds performance: User Pays (4DUP) strong, Regulated Utilities (4DUts / S&PI) mixed

As evident in Table 1, a rising US Federal Funds rate did not seem to significantly impact the performance of the 4DUP, which outperformed the MSCI in all four measured periods. However, the performance of the 4DUts and S&PI were not as strong, significantly underperforming the MSCI during months 7-12 of the November 2015 rate hike cycle.

This is also illustrated in the following charts.

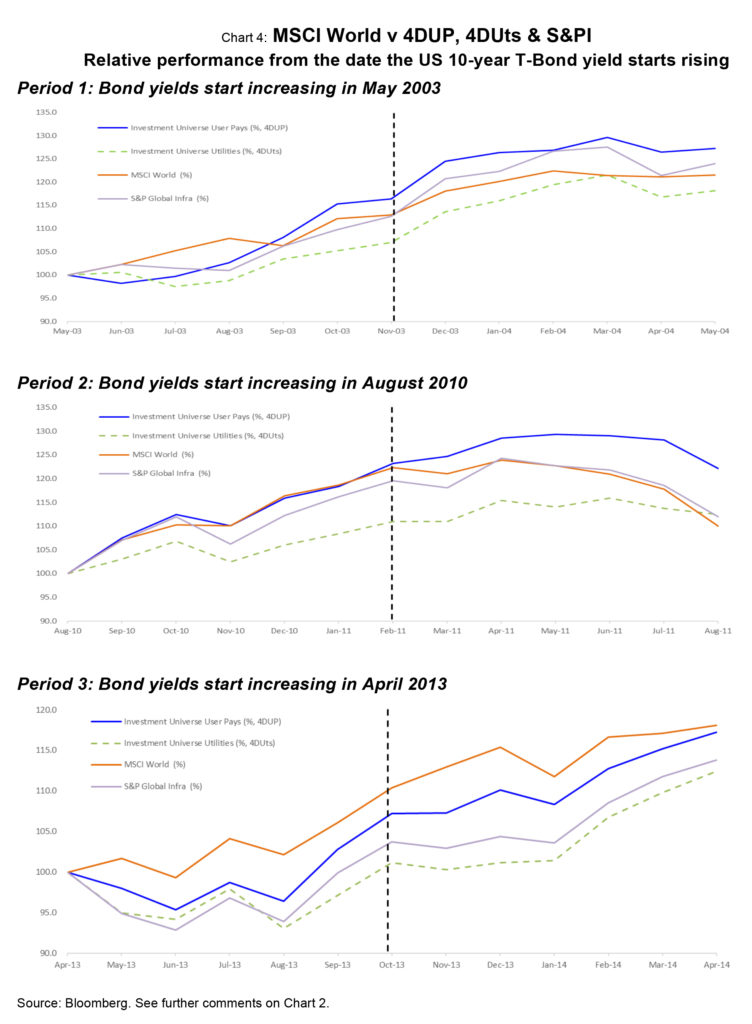

5. Rising rates 2: Three periods where the US 10-year T-Bond yield rose by 1%

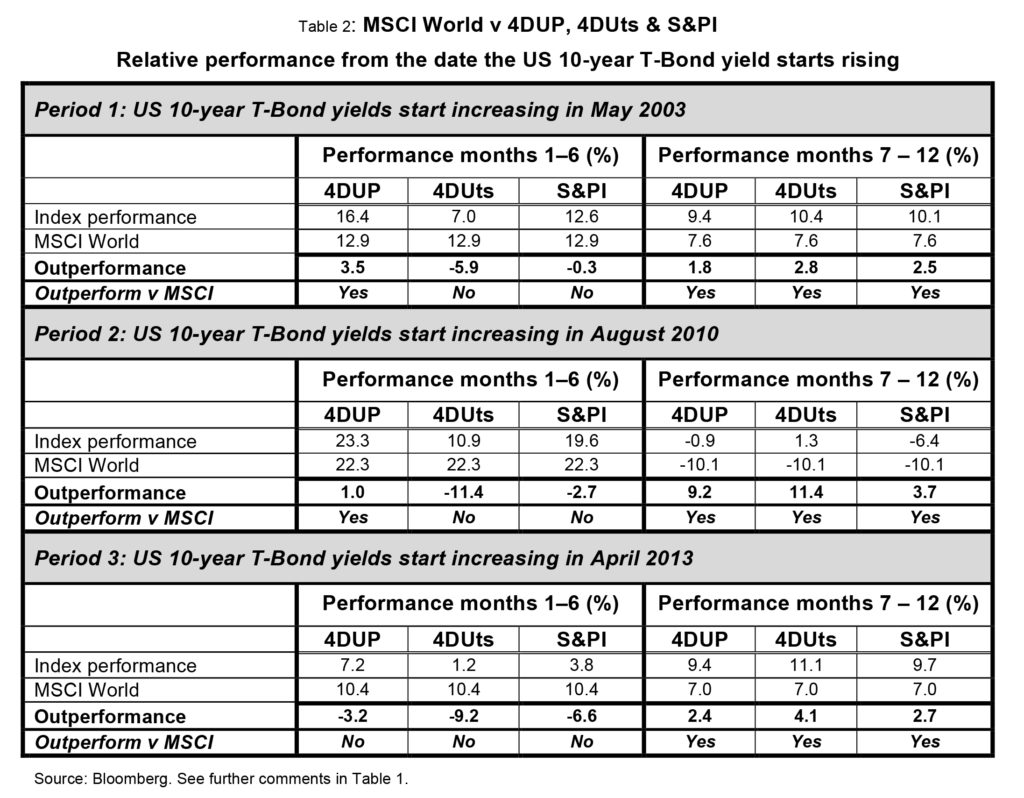

As shown in Chart 2, since 2000 there have been three periods during which the US T-Bond yield rose by 1% over consecutive months. The performance of our infrastructure indices over these periods is in Table 2 below.

Conclusion re US 10-year bond performance: User Pays strong, Regulated Utilities / S&PI initially negative

Table 2 suggests that rising US bond yields are far more influential for listed infrastructure equity market performance than are increases in the US Fed Funds rate. Notably:

- the 4DUP outperformed the MSCI over five of the six measured time periods, underperforming only during the first six months of Period 3 and recovering much of that underperformance during months 7-12;

- both the 4DUts and the S&PI underperformed the MSCI during the first six months of each of the three periods of rising yields, then outperformed during months 7-12; and

- over each of the three 12-month periods following bond yields increasing, the 4DUP outperformed both the 4DUts and the S&PI.

This suggests to us that, in a rising rate environment, a portfolio should be weighted to User Pays.

These outcomes are illustrated in Chart 4 below.

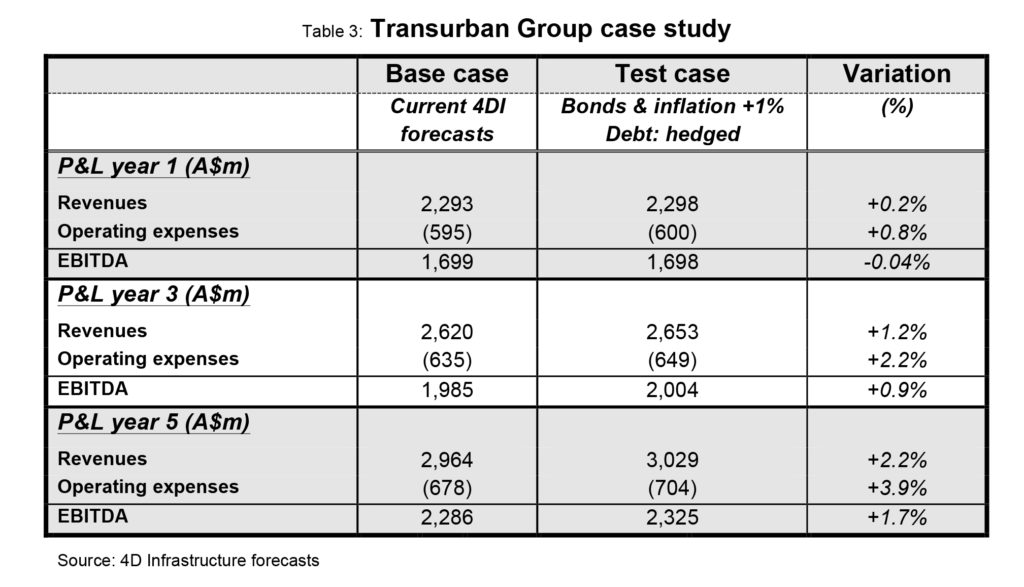

Case study: User Pays stock – Transurban Group (TCL AU)

This case study explores the impact of an assumed increase in Australian and US government bond yields of 1%, and – as rising bond yields normally accompany rising inflation – an assumed 1% increase in inflation. How do these impact 4D’s base case (current) five-year earnings forecast for a User Pays stock such as TCL?

The results (summarised in Table 3 below) show that our forecasts for TCL’s earnings before interest, tax, depreciation and amortisation (EBITDA) improve when interest rates and inflation rise.

Revenue and operating expenses

By year five, both revenues (+2.2%) and operating expenses (+3.9%) are higher in the test case. Forecast revenues increase because in approximately 80% of TCL’s toll road concessions they have the right to pass through inflation increases via toll escalations.[2] On the other 20% of TCL’s road concessions they have the right to increase tolls by the higher of an agreed percentage, or actual inflation. In our test case we don’t change the base case revenue assumptions on the smaller portion of their portfolio, as we have assumed the allowed toll escalation under the concession deeds exceeds our assumed inflation increase. Forecast operational expenditure increases due to the assumed inflation impact on costs.

EBITDA

Significantly, by year five, even though revenue and operational expenditure are both up by 2-4% in the test case, EBITDA has also increased strongly by 1.7%. This reflects TCL’s powerful EBITDA leverage, whereby EBITDA/revenue is approximately 80% – hence a substantial component of any revenue growth flows through to EBITDA.

Conclusion

Clearly there is more to the relationship between rising interest rates/inflation and the performance of infrastructure stocks than is commonly perceived.

- User Pay stocks have generally performed well during such periods. A rising US Federal Funds rate did not adversely impact the performance of the 4DUP, which outperformed. However, the performance of the 4DUts and S&PI were not as strong, significantly underperforming the MSCI during one period.

- Rising US bond yields look to be more influential for listed infrastructure equity performance than increases in the US Fed Funds rate. However, the 4DUP still outperformed the MSCI over five of six measured time periods (recovering much of that one period of underperformance in the subsequent period). In contrast, both the 4DUts and the S&PI underperformed the MSCI during the first six months of each of the three periods of rising yields, then outperformed during the later months. Rising bond yields seem more closely correlated to the performance of Regulated Utilities.

- In addition, over each of the three 12-month periods following bond yields increasing, the 4DUP outperformed both the 4DUts and the S&PI.

This suggests to us that User Pay assets should be the preferred holding over Regulated Utilities in periods of rising interest rates and strong growth.

Finally, the varied asset characteristics and performance that we have observed across differing macro-economic backdrops demonstrate the importance of active portfolio management, and the ability to appropriately position an equity portfolio for the economic circumstances of the day.

Infrastructure: an asset class for all stages of a market cycle

So, to conclude: is infrastructure a bond proxy?

We believe this notion is far too simplistic. The inherently different asset characteristics of User Pays vs Regulated Utilities, and the performance they deliver, mean infrastructure is an asset class that can be tailored to all stages of a market cycle. User Pay assets facilitate a portfolio being positioned for a GDP growth/rising interest rate/inflationary environment. Conversely, in more difficult economic times, possibly incorporating falling interest rates, Regulated Utilities offer an ideal defensive home given their earnings certainty, which are largely immune to the macro cycle.