Investors sticking to the traditionally high quality, conservative part of global bond markets may be surprised to learn that they are more exposed to riskier credit now than prior to the GFC.

Unlike high quality AAA-rated bonds, a BBB bond is only one or two downgrades away from ‘high-yield’ or ‘junk’ status. When the economy turns sour, these companies can quickly find themselves relegated.

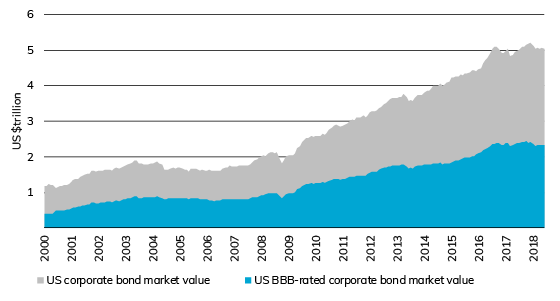

At the start of 2000, the BBB-rated market was worth around US$400 billion, or one third of the total investment grade market. By the end of June 2018, this had grown to $2.3 trillion, compared to a total market value of $5 trillion (see chart below).

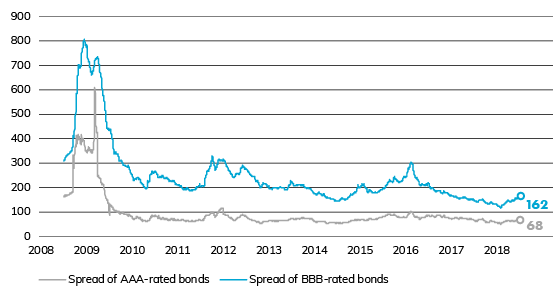

Globally, companies are increasingly prepared to push their debt ratios higher to fund expansion, and they have found an audience of investors keen to squeeze extra yield from their portfolios. This demand is reflected in US spreads on BBB bonds, which have moved lower and converged with AAA spreads over the past two years (see chart below).

Firms have also sought to lock in access to cheap finance for as long as they can, meaning investors are not only exposed to lower quality credit, but may also be exposed to bonds that are more sensitive to moves in both underlying yields and a widening in credit spreads. In contrast to the global landscape, Australia’s investment grade bond market is dominated by financials, meaning exposure to BBB bonds is comparatively lower.

Investment managers at the conservative end of the risk spectrum, such as pension funds and insurers, rely on the investment grade market for stable and predictable returns. But the ‘risking-in’ trend means that even the safest parts of an investor’s portfolio might not be as safe as they think, and could be exposed to ‘glittering junk’ – companies that appear to offer safe yields but are at risk of being crushed by debt when their equity value falls.