The growth potential of global businesses is enormous; by investing in them, your clients can benefit from people like them, around the world, using their products and services each day.

Most investors understand the basics of diversification, or at least understand the adage ‘don’t put all your eggs in one basket.’ However, many investors don’t understand the diversification benefits that arise from each and every asset class. Using global equities as an example, Perpetual explores the way an individual asset class can provide a range of diversification benefits to your clients.

There are many sound reasons to invest in global equities:

- Australian companies comprise less than 2% of global sharemarkets

- Access to different markets, sectors and geographies

- Access to industries not represented in the local market

- Benefit from demographic trends across the globe.

What’s generally not considered are the myriad of diversification benefits that can be derived from investing in global equities.

Portfolio diversification is no longer as simple as allocating investments across asset classes, such as domestic and global equities and fixed income, property, cash and perhaps some alternatives. To reap the benefits of a truly diversified portfolio, advisers also need to diversify within each asset class.

Investment style

Fund managers have variety of lens through which to view companies and can adopt a range of investment approaches and styles when managing global equity funds. In allocating to funds, a balanced approach is critical; markets can be unpredictable and there will be periods when different investment styles have markedly different performance outcomes. Ultimately, a mix of different investment styles can best help your clients achieve their investment objectives. The investment styles most common to global equity funds are summarised in figure one.

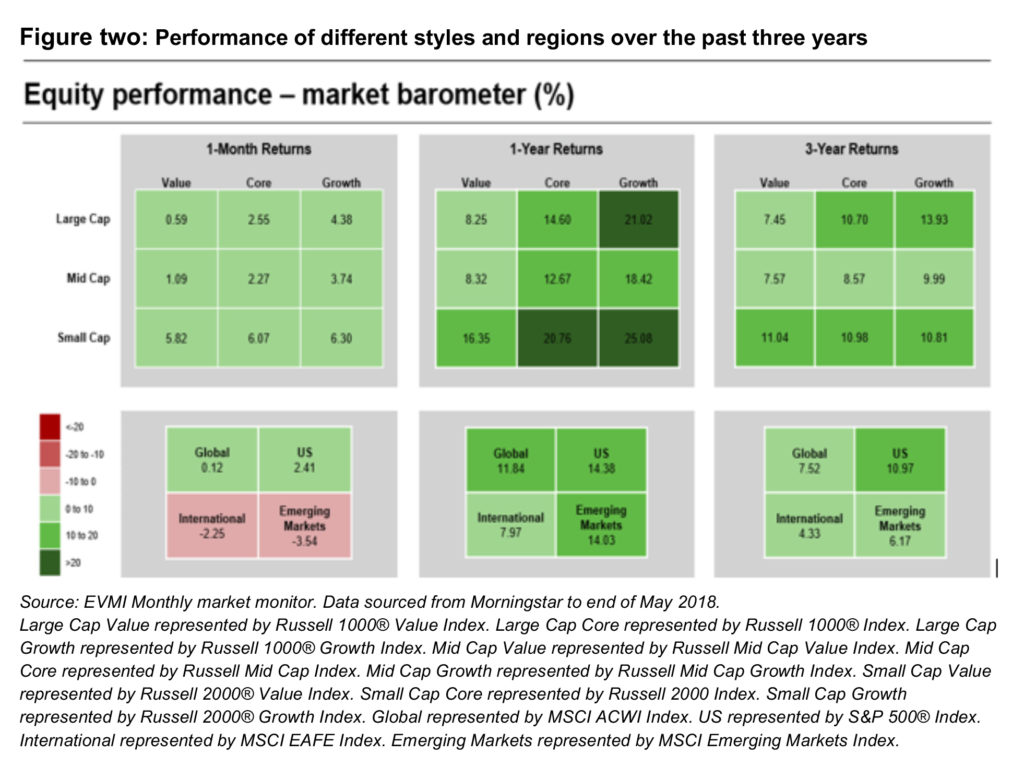

That each of these investment styles performs differently at various times within a market cycle is illustrated by the market barometer in figure two, which provides one month, one year and three year returns for global equity value, core and growth managers. As would be expected at this stage of a prolonged bull market, growth managers are outperforming.

While clients may look at this and think they should be invested in growth funds, it’s important to diversify across investment styles to benefit from each stage of a market cycle. Once the current bull market in equities ends, it may be a while before growth funds top the charts again.

Geographic diversification

A geographically diverse portfolio invests across different geographic regions to reduce the risk and return profile of the overall portfolio. Investment in different countries enables your clients to benefit from differing economic cycles in both developed and developing economies.

The booming US economy, helped along by President Trump’s corporate tax cuts in late 2017, has pushed the US market to new highs. As illustrated in figure two, it’s been a standout performer. However the US economy faces potential headwinds – rising inflation, the prospect of further interest rate hikes, the risk of a trade war – so, as is the cyclical nature of investments, the US market will cede to others.

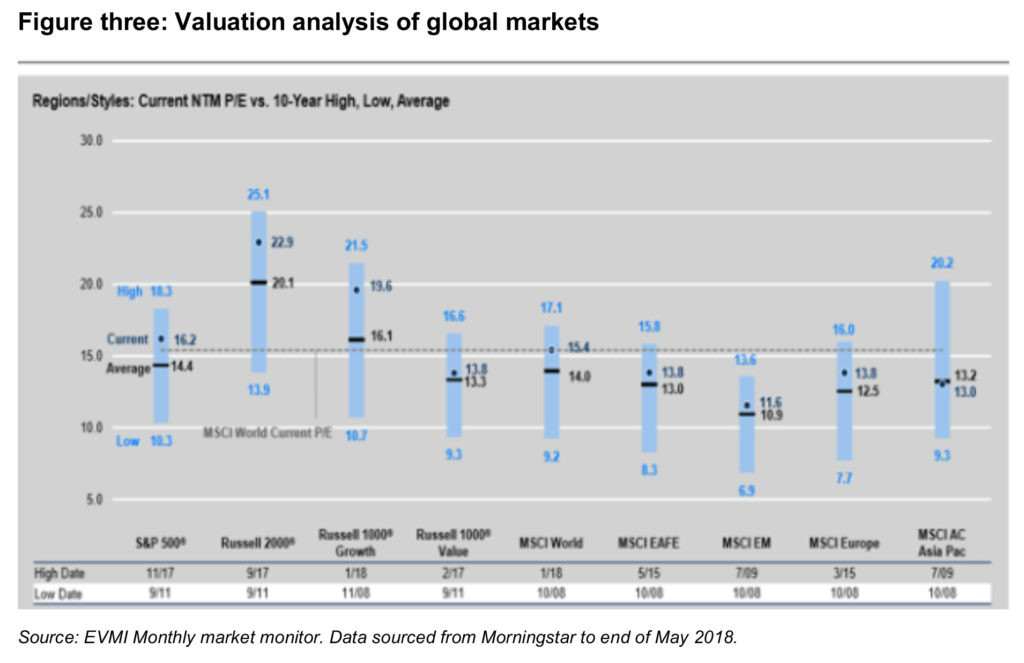

Figure three examines the current average price to earnings (P/E) multiple of the MSCI World Index versus a number of markets measured over 10 years. The current P/E of this index is 16.2, higher than the 10-year average for most regions. Although P/E multiples are above 10-year averages in the US, Europe and a number of emerging markets, they are in line with historical averages in Asia. This variation in valuation further highlights the importance of being diversified across geographic lines.

Sector diversification

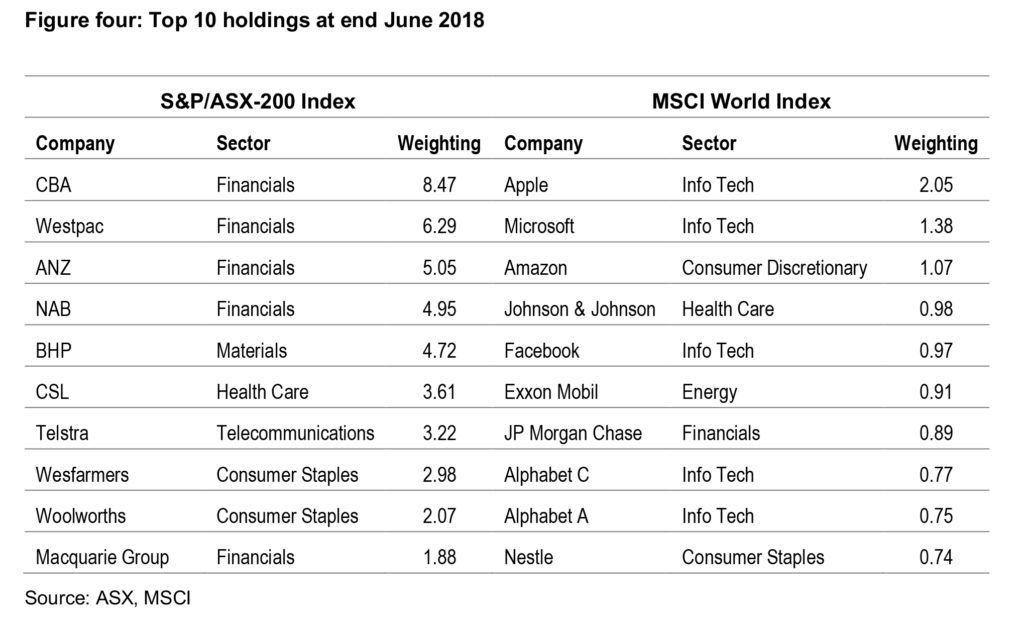

An essential element of diversification for Australian investors is sector diversification. The Australian market is very concentrated; the top 20 stocks of the S&P/ASX200 comprise 55% of that index. Within that, the financials and materials sectors dominate.

Figure four compares the top 10 stocks of both the S&P/ASX200 Index and the MSCI World Index. The top 10 ASX200 stocks represent 42% of that index, the MSCI’s top 10 just 12%. Both indices have five stocks within a single sector – Australia has five companies in the financial sector, which combined, represents 23.8% of the index. The MSCI World Index has more than 1,600 constituents; so while US-based information technology giants may dominate the index’s top 10 stocks, they represent just 7% of the total index. In other words, the concentration of each stock, as well as sectors, is much lower in the MSCI World Index despite the vast size of these companies.

Diversification by industry

There are a range of industries that aren’t available, or have limited availability, through the Australian share market:

- Technology giants Apple, Microsoft and Alphabet (parent company of Google)

- Aircraft manufacturers Boeing and Lockheed Martin

- Healthcare, with household names such as Johnson & Johnson and GlaxoSmithKline, manufacturer of Panadol

- Multinationals such as Nestle, Unilever and Proctor & Gamble, producers of everyday food and personal product brands.

Because there is such diversity and a large number of companies, broker coverage of index stocks is not as fulsome as in the Australian market. As such, there is more opportunity for investment managers to identify companies that are mis-priced or overlooked. The following case study provides a ‘deep dive’ into a stock that was under-covered and therefore undervalued, in a sector that’s underrepresented in Australian stocks.

Case study one – Nomad foods

Garry Laurence, portfolio manager of Perpetual’s global equities strategies, recently visited Nomad Foods (Nomad), one of Perpetual’s holdings. According to Garry, the management team at Nomad continues to impress under the direction of Stefan Drescheemaeker. Nomad has strengthened its market share in the UK frozen foods market, with around 20% market share. It is slowly being re-rated by the US market as the word gets around that Nomad is building a European foods powerhouse.

As a consumer staples business, it’s expected to perform well when economic growth eventually starts to weaken. Perpetual believes Nomad has the right structure and fundamentals to grow its earnings and share price over the next decade.

What initially drew Perpetual to the business was the heavily discounted valuation multiple the stock was trading on relative to its peer group. Early on, when Perpetual first invested, the stock was trading at only 10x earnings because the market was giving management no credit for being able to grow the business. There was also a lack of awareness about the business as only one or two investment banks covered the stock.

Perpetual looked through the history of the businesses and quickly realised that some previous market share losses and underperformance were due to strategy issues. Perpetual spoke to the previous CEO of the business, buying managers at their larger retail customers, and senior management of several competing businesses to gain a better understanding of the potential outcomes from the new CEO’s strategy of refocusing on the core business and ‘must win battles’.

Perpetual also spoke to Nomad management and quickly realised that the actions they were taking to re-invigorate the core brands made perfect sense and would accelerate sales growth. The fruits of these actions are becoming evident, with organic revenue growth of 3% in the last quarter and operating earnings growth of 16%.

Nomad has moved from being about turning around underperforming brands to one which is on firm footing where the core brands are delivering. They have recently been on the acquisition trail in the UK, purchasing Aunt Bessie’s and Goodfella’s. These brands are the leaders in frozen Yorkshire puddings, potatoes and pizza in the UK and are strategically important, as the acquisitions increase Nomad’s market share to 20% in the UK frozen foods market, which also increases the company’s bargaining power with its core retail customers.

Disruption and demographics

Disruption through technological advancements is a global trend. Australia has witnessed the rise in Fintech, clients have no doubt asked you about bitcoin and other cryptocurrencies, and most of us have used platforms such as Uber, Airbnb or Netflix, each of which has turned a traditional business model on its head.

Australia’s population is small by global standards; diversifying into global markets can enable your clients to take advantage of these disruptors as well as demographic trends such as:

- Growth in emerging markets including China and India, countries with large populations, high economic growth and a rising middle class with a vast appetite for consumer goods and luxury brands

- The ageing population in developed markets, which creates a growing need for aged care facilities, health care and in-home support

- Continued automation across a range of industries, which spawns new technologies and evolving industries.

While some Australian businesses successfully tap into these global trends, many of the companies that are best positioned to benefit are based in other parts of the globe. Case study two looks at the automation of cars; there may be Australian components businesses that benefit from this trend, but they are generally not listed companies.

Case study two – Automated cars

There are numerous stages that will emerge over next decade before ‘every day’ cars become completely driverless; presently, the most advanced cars are at level 2 autonomy, where a car provides partial driving assistance and might automatically brake if it senses a collision. For example, the BMW 5 series has 23 sensors in the car with cameras, lidars and radars.

The next stage of autonomy is level 3, where the car can self-drive in ‘safe’ conditions; it will signal to the driver when self-drive isn’t possible. High definition mapping will be added to vehicles on top of cameras and sensors.

Level 4 is the stage of robo taxis; you will still need the driver in the car, but the car will be in effective control. BMW expects to get to this level by 2025.

Level 5 is completely autonomous driving; this however, is dependent on governments having the confidence to regulate in favour of it.

Manufacturers of cars, components and technology will benefit from this shift.

The growth potential of global businesses is enormous; by investing in them, your clients can benefit from people like them, around the world, using their products and services each day. Importantly, they can also benefit from the myriad of diversification opportunities that global investments can add to their portfolio.