A long life shouldn’t have to be a bad life. In fact, it’s almost always better than the alternative – premature death – but the financial services industry has people thinking otherwise.

Longevity risk, we’re told, is the problem. Boys and girls born in 2013–2015 can expect to live around 33 and 34 years longer than their ancestors born in 1881–1890, according to a government analysis.

But dig a little deeper and the underlying data suggests it’s a faulty diagnosis.

Living a long life isn’t a problem for individuals – their problem is that they don’t know how much their lifestyle costs and how that expenditure is likely to change over the course of their retirement.

Uncertainty: lifespans or expenditure?

Longevity risk is a problem for governments, which bear that risk directly via defined benefit fund liabilities and the Age Pension. It’s also a problem for the financial services industry, which offers products such as life insurance and various types of annuities.

But ordinary Australians think differently. Too many are worried they’ll run out of money in retirement but this issue may be solved, like any other asset-liability problem, with the correct data.

The missing data has been accurate personal expenditure which underpins retirement lifestyles. Until recently, the industry has rarely even attempted to measure actual expenditure in retirement, instead relying on limited surveys based on individuals’ memories and estimates.

There’s an old joke about a physicist, an engineer and an economist stranded on a desert island with nothing to eat except a can of baked beans. The physicist and engineer argue about how to get the beans out of the can without wasting any. The economist advises them: “It’s simple. Assume a can opener.”

Look at any pension or annuity product forecast and you’re likely to find a similar glaring assumption: that retiree costs are based on their current expenditure rising in line with inflation each year. The cost of this assumption is borne by retirees having lower standards of living.

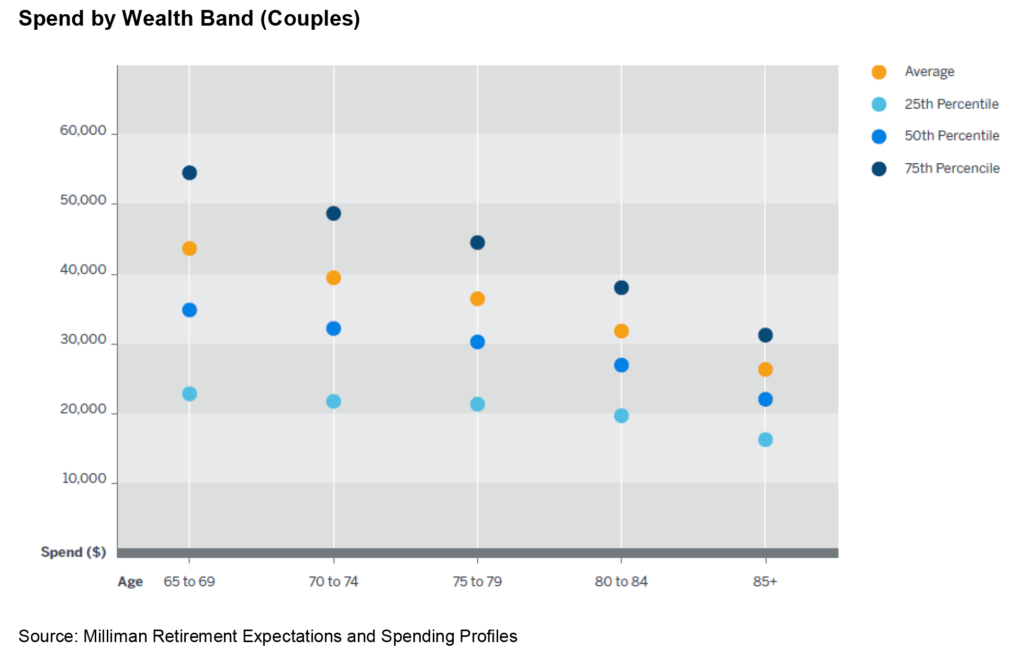

Data pinpoints the misdiagnosis Real-world big data, captured and analysed through Milliman Retirement Expectations and Spending Profiles (ESP), shows that spending consistently declines over retirement by about 6-8% in each four year age band before plummeting from age 80.

A number of overseas studies have produced similar results.

The Center for Retirement Research analysed multiple age cohorts using US government Consumer Expenditure Survey data and found that retirement spending drops by about 1% a year. Other US studies have also found declining retiree expenditure.

A study by the International Longevity Centre – UK found that a household headed by someone aged 80 and over spends, on average, 43% (or £131) less than a household headed by a 50 year-old.

However, typical industry-produced retirement simulations that assume expenditure increases with inflation would have a female retiree saving for peak spending in her final year of life, age 85 – when her spending is around its lowest.

This flawed assumption encourages retirees to be over-conservative with their spending. The many retirees who take out account-based pensions and then live frugally by drawing down the minimum allowable rate, is the classic case. Unfortunately they’re banking on a higher cost lifestyle that will never arrive.

We need to start to address this problem through the customer’s eyes and not through the industry’s lens.

A deeper understanding of real-world data and behaviour is the starting point. It allows us to segment different types of retirees based on multiple facets such as wealth band, postcode, home ownership – the options are endless.

A future edition of the Milliman Retirement ESP, which analyses the bank account expenditure of more than 300,000 retirees, will delve further into the retiree spending categories that have high degrees of uncertainty or variation.

If we can diagnose the true problem, retirees living a long life stand to enjoy a better life.