Mobile adoption curve and 5G – a unique opportunity in global listed infrastructure investment

Communications infrastructure, a sub-segment of the infrastructure asset class, is enjoying rapid growth driven by a huge expansion in data demand.

Communications infrastructure, a sub-segment of the infrastructure asset class, is enjoying rapid growth driven by a huge expansion in data demand.

For global listed infrastructure in particular, there is a unique opportunity to provide investor access to mobile wireless infrastructure companies across both developed and emerging markets. Their appeal comes from the strong infrastructure characteristics of mobile wireless infrastructure stocks combined with exposure to the growth this sector will enjoy from increased mobile subscription penetration and mobile technology evolution (5G).

Mark Jones, Senior Investment Analyst from 4D Infrastructure, explores the appeal of communications infrastructure, the difference between developed and emerging markets, and the possible upside from the transition to 5G.

Introduction

One of the most prevalent trends over the past 10 years has been the growth in internet data demand, as demonstrated by Cisco Systems’ visual networking index (VNI)[1]. According to Cisco, internet data demand will reach 278 exabytes per month in 2021 (compared to 96 exabytes per month in 2016 and 31 exabytes per month in 2011) and will grow at 23% compound annual growth rate (CAGR) from 2016 to 2021.

A key consequence of this is the future need for communications infrastructure investment, the majority of which will be privately funded. Communications infrastructure embodies the facilities and networks employed to transmit and receive information by electrical or electronic means. It is typically represented by physical assets such as copper and/or fibre optic cables (onshore and offshore), wireless towers and data centres.

Communications infrastructure is very well represented in the global listed infrastructure universe, particularly in wireless tower stocks. Wireless towers facilitate mobile telephony by providing access for antennae and electronic communications equipment on a radio mast (typically galvanised steel) or other raised structure (e.g. rooftop). Mobile telephony is expected to be the strongest source of internet data demand, with Cisco formulating it will account for 63% of all internet traffic in 2021 (up from 49% in 2016).

This is driven by:

- ongoing smartphone penetration around the world: and

- increase in bandwidth and capacity as mobile technology transitions to 5G.

Walk down any street, enter any restaurant, sit on any bus, and you are sure to find people on their mobile phone. Whether it’s messaging, surfing the internet or watching video, the mobile device is now a ubiquitous fixture of modern living – and this ignores future possibilities such as ‘internet of things (IOT)’ (i.e. interconnection via the internet of computing devices embedded in everyday objects such as a car, TV, street lights, etc).

With ever-increasing mobile internet data demand, there are two primary ways of adding capacity to a network:

- buy more spectrum and/or make spectrum more efficient; and/or

- densify a network by adding more wireless towers.

As highlighted by GSMA[2]: ‘With more than 5 billion unique mobile subscribers at the end of 2017, mobile has a greater reach than any other technology’.

Benefiting from these underlying themes, the global listed infrastructure asset class is in a unique position to participate in this growth with wireless tower companies well represented in both developed and emerging markets. It offers an important point of difference when considering listed global infrastructure as a portfolio allocation option.

What is the investment attraction of wireless towers?

Economies of scale

Wireless towers facilitate mobile telephony by hosting radio antenna, transmitters, and receivers which allow data to be requested and responded to from a mobile device. They are typically self-supported or free-standing, located on monopole / lattice galvanised steel or on rooftops, often with backup power, and connected by fibre / coaxial backhaul to a base station. The capacity of a network is broadly dependent on two variables:

- spectrum; and

- the density of the network of wireless towers.

Spectrum plays a key role in wireless communications given its propagation qualities, sending or receiving the signal from the antenna at the speed of light. The density of the network of wireless towers allows the spectrum to be accessed.

As population density and mobile subscription increases, there is a positive correlation to data demand. The value proposition of wireless towers, like many other infrastructure assets, is in providing economies of scale. That is, it is more efficient and cost effective to build one-to-many shared infrastructure wireless towers in a particular area; rather than many-to-many standalone wireless towers.

Wireless towers achieve a positive return on invested capital when there is more than one tenant being hosted (often referred to as a tenancy ratio > 1). Counterparties, which are typically large telecommunication players, are incentivised to co-locate on independent wireless towers: firstly, to remove redundancy (of multiple towers in a particular area) and optimise operating costs; and secondly, to recycle capital for other purposes (e.g. acquire additional spectrum).

On the right is an example of a wireless tower hosting two sets of radio antenna suggesting it is co-located by two tenants (i.e. a tenancy ratio of 2 – see the two bands of equipment on top of the tower).

Earnings resilience and growth

Wireless tower businesses demonstrate many of the classic infrastructure asset characteristics that we look for at 4D, including high barriers to market entry; inbuilt inflation hedge; visible and resilient cash flows and earnings; strong contracts; and long dated assets.

Extrapolating these general characteristics to the wireless mobile tower assets, the following can be found:

- Long-term tenant leases with contractual rent escalators and minimum churn. Large telecommunication players will typically agree to a master service or master lease agreements (MSAs / MLAs) varying in duration from five to 10+ years. Churn is low because it is in the interest of all telecommunication players to: 1) optimise network topology and capacity; and 2) provide the most stable coverage possible.

- Barriers to entry. The barriers to switching are twofold: firstly, there are often regulatory, environmental, or social constraints on wireless tower density in any particular area; and secondly, repositioning radio antenna equipment may be expensive and adversely affect the quality of its network.

- High proportion of fixed costs, high operating margins and low maintenance capital expenditures. The incremental variable and maintenance costs of additional tenants are relatively minimal, allowing for increasing margins as the tenancy ratio increases (with no constraint on the number of tenants in most markets, Italy being an exception to this general rule).

- Growth opportunities. Independent wireless tower companies will specialise in acquisition, building, de-commissioning and maintenance. This allows for incremental opportunities to increase and/or rationalise the number of wireless towers in a portfolio and further benefit from economies of scale.

Opportunity set

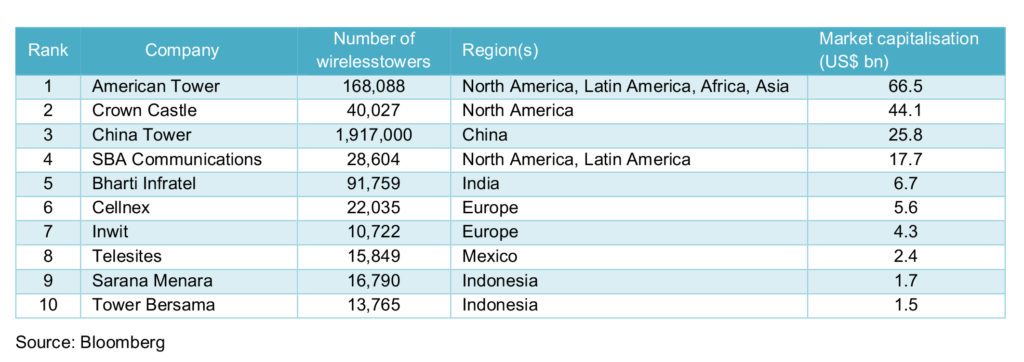

Following the recent initial public offering of China Mobile (788 HK) on the Hong Kong stock exchange on 8 August 2018, global listed communications infrastructure companies’ market capitalisation now represents approximately 7% of the total market capitalisation of global listed infrastructure, with representation across both developed and emerging markets.

There is also potential for further wireless tower portfolios to be acquired, most notably in Europe, with almost 100,000 wireless towers being collectively owned by the major telecom companies Vodafone, Deutsche Telecom, and BT: all being potentially for sale, or IPO

Long-run, bigger opportunity in emerging vs developed markets

Growth in mobile subscriptions

Different countries’ markets offer different growth rates in mobile internet data demand, depending on the:

- number of mobile subscribers in the population; and

- level of mobile technology penetration (e.g. 3G, 4G, or 5G) and concomitant demand for data.

Simplistically, the lower the number of existing mobile subscribers and/or technology penetration, the higher the potential future growth rate, with mobile technology adoption positively correlated to GDP per capita. This has led to higher growth rates in emerging markets (EM) communications infrastructure as seen in other infrastructure assets such as airports, because:

- Larger populations such as the BRICs (Brazil, Russia, India, and China) have required much larger wireless tower buildouts;

- Governments are increasingly becoming involved (accelerating buildouts) due to the importance of mobile telephony for competitiveness (e.g. Ghana’s Minister of Communications announced the country is targeting 100% population wireless coverage by 2020);

- Later adoption of mobile technology has led to improved economics on smartphones. Low cost smartphones (e.g. 4G compatible) entering the market now have a purchase cost of below US$100 and pre-paid data packages increase accessibility for the wider population; and

- The growth of the middle class, especially in EMs, is a very important ongoing investment theme. As individual wealth increases in a country – reflected by a growing middle class – consumption patterns tend to change towards more services and experience-based spending (such as mobile phone use).

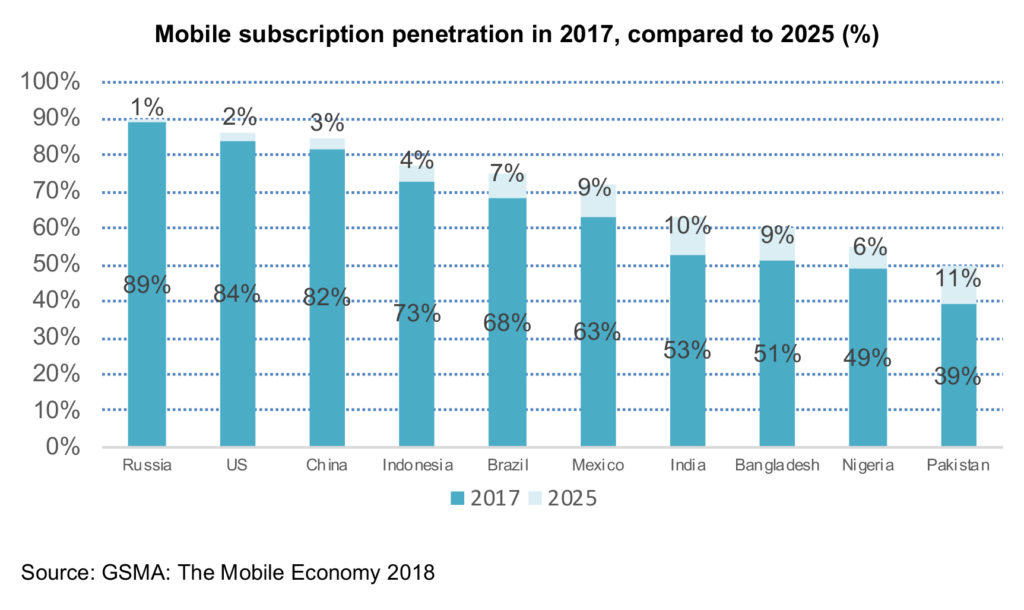

This is reflected when mobile subscription penetration is compared globally across the 10 largest populations. According to GSMA, the strongest growth in mobile subscribers to 2025 will be EMs: Asia – Pakistan (11%) and India (10%), followed by Latin America – Mexico (9%) and Brazil (7%), and Africa – Nigeria (6%).

A perfect illustration of an emerging market mobile wireless tower company is represented by the example of Telesites

Case study 1: Telesites from Mexico

Telesites (SITESB1 MM) was formed due to regulatory change in Mexico. Constitutional reform of the telecommunications sector, approved in 2013 (the ‘telecom reform law’), established telecommunications and broadcasting services as public services of general interest, meaning the government guarantees these services meet certain criteria, including standards relating to quality and competition. The aim of the reform was to address lack of competition and transparency, all of which resulted in high prices, low market penetration, and importantly insufficient infrastructure development.

OECD studies had suggested mobile data prices were relatively high in Mexico (OECD, 2012a) and, in terms of investment in public telecommunications per capita, Mexico ranked last out of the 34 countries of the OECD. From 2000 to 2009 the sum of public telecommunication investment per capita in Mexico amounted to only US$326 compared to the OECD average of US$1,447. Moreover, revenue from the telecommunications sector as a percent of GDP had also been consistently lower in Mexico compared to the average of all OECD countries.

The telecom reform law forced Mexico’s largest telecommunications player, America Móvil, to either reduce its market share or comply with the asymmetric regulation necessary to enable the entrance of new competitors (e.g. by obliging dominant players to share their infrastructure). This pre-empted America Móvil to divest its mobile wireless towers into a separate entity, Telesites, which was listed on the Mexican stock exchange in December 2015. At the time of the IPO, Telesites was made up of 10,800 mobile wireless towers (representing approximately 40% of the total mobile wireless towers in Mexico). On each of its wireless towers, it had only one tenant: America Móvil (i.e. tenancy ratio = 1).

Since then, there have been significant changes to the Mexico telecommunications market. Following the thematic of mobile telephony and competitiveness, the Mexican government decided to fully fund a wholesale mobile network, Red Compartida, to incentivise new retail mobile players. Red Compartida had exclusive access to the 90 MHz of 700 MHz spectrum, and was mandated to cover at least 30% of the country’s population by year-end 2017, and 92% by year-end 2023. Aligned to the benefits of shared wireless, Red Compartida will facilitate the deployment of radio antenna, transmitters and receivers across many wireless towers over the next five years. If successful, it will be the first fully wholesale mobile network deployed anywhere in the world.

Telesites will continue to benefit from this deployment and the competitive dynamic that will ensue, with all telecommunication players in Mexico (America Móvil, AT&T and Telefonica) looking to improve speed, bandwidth, and capacity. Below is Telesites’ growth in earnings (as represented by EBITDA[3]) and tenancy ratio since 2016. It has had ~9% growth in number of wireless towers, +5% growth in tenants and +15% growth p.a. in earnings since 2016.

Evolution in mobile technology: all roads lead to 5G

If growth in communications infrastructure was only a function of the number of subscribers, there wouldn’t be much appeal in markets such as the US and Europe. However, the other important variable to consider is the level of mobile technology adoption. Earlier this year, the third and fourth largest telecommunication players in the US proposed a merger, with one of the rationales for the US to extend its global leadership in 5G mobile technology. Deloitte serendipitously highlighted that since 2015, China had outspent the US by approximately US$24 billion in wireless communications infrastructure, and built 350,000 new wireless tower sites while the US built fewer than 30,000[4].

Changes in mobile technology evolution also precipitate growth in communications infrastructure. This can occur through the buildout of additional towers to increase the density of network topology or from amendments to existing towers, with telecommunication players having to upgrade radio antenna, transmitters and receivers which can lead to higher leasing rates (due to the additional weight of new equipment).

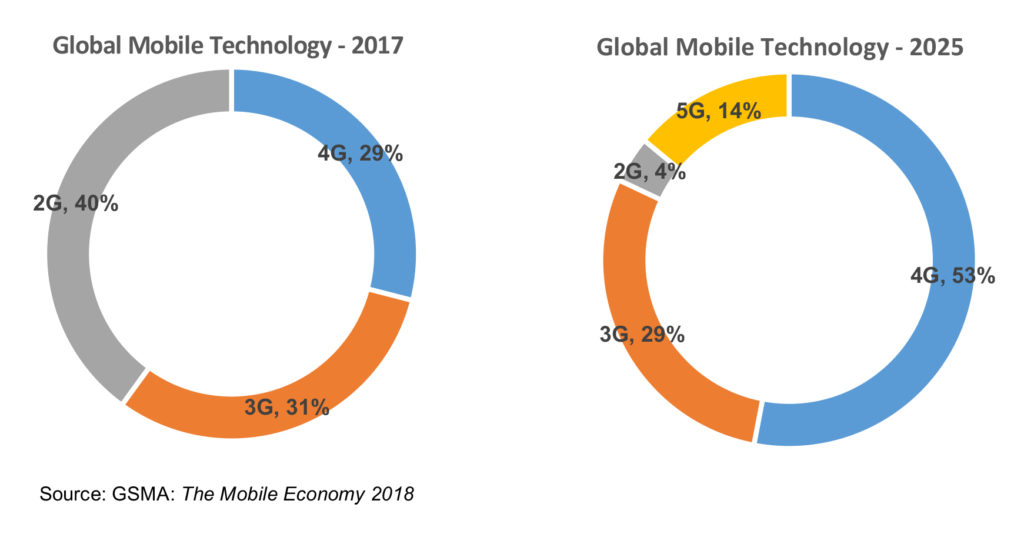

According to GSMA, mobile technology adoption will continue to progress, namely through increased penetration of 4G and transition from 4G to 5G. Clearly this is good for the wireless tower companies.

Developed markets will benefit from the transition from 4G to 5G. First-mover advantage is being competed for both within developed markets (e.g. Verizon vs. AT&T in the US) and across developed markets (e.g. US vs China vs Japan vs South Korea). 5G is being used by cities as a competitive and economic differentiator. This leads to the question: what is 5G

5G is the latest mobile technology evolution. Mobile technology has evolved with each generation providing additional functionality as shown below.

What are the key features of 5G?

The most notable characteristic of 5G, and indeed any later generations of mobile technology, is that the evolution mainly brings improvements in speed, bandwidth, and capacity, highlighting the increasing demand for mobile data. Because 5G will be able to connect a lot more devices at once, it will facilitate a myriad of use cases (e.g. smart cities, augmented reality, etc). At a recent town hall, CEO of T-Mobile US John Legard stated that ‘we are not able to imagine exactly what will happen’, highlighting 5G as an enabler for many new applications.

From a communications infrastructure perspective, 5G relies on network densification, which requires the addition of wireless towers, both in the form of macro cells and small cells. According to US wireless tower company Crown Castle (CCI US), which specialises in small cells, 5G is a ‘megatrend’ with US telecommunication players expected to lead the way and be among the first operators in the world to deploy commercial 5G services (requiring additional macro and small cell infrastructure).

The difference between macro cells and small cells is form factor, size and the radio antenna being used. Macro cells are equivalent to the wireless tower illustrated previously, characterised by large radio antenna equipment on the tower. Small cells are characterised by smaller, less visible radio antenna equipment often retrofitted into existing urban infrastructure such as electricity poles or street lights. This bifurcation of wireless towers into macro cells and small cells is driven by 5G. Because 5G will typically be facilitated by higher spectrum characterised by shorter propagation but higher bandwidth, there will need to be many, many small cells, particularly in areas of high demand such as urban areas.

While it is difficult to size the opportunity before communication infrastructure companies, commentary from US telecommunication player T-Mobile implies an increased level of spend for wireless networks, highlighting (in its potential merger with Sprint) that 5G will require an additional 10,000 (macro) wireless towers in the US. It has commissioned 25,000 (small) wireless towers in 2019 alone. A recent report from industry trade group CTIA[5] said 80% of future wireless deployments will be small cells, leading to the number of small cells installed in the US to grow to more than 800,000 by 2026 (compared to ~100,000 currently).

Similarly, in China, according to Ernst & Young, 5G is a top-down national agenda item, with commercial deployment beginning in 2019 and 5G mobile connections potentially reaching 576 million by 2025. To highlight the scale of the buildout ahead, China Tower currently only had 17,000 small cells as at the end of 2017 (compared to 1,850,000 macro cells).

Outside the US and China, the other leading markets for 5G include developed Asia, such as Japan and South Korea, and developed Europe, with emphasis on Italy as one of the only countries that has already auctioned 5G spectrum. A perfect illustration of a developed markets wireless mobile tower company is represented by the example of Cellnex.

Case study 2: Cellnex

Cellnex (CLNX MM) is an independent communications infrastructure provider with a portfolio of more than 22,000 mobile wireless towers across many jurisdictions in Europe. Cellnex was one of the first movers to own and manage mobile wireless towers in Europe, in 2012 acquiring a portfolio of mobile wireless towers from Spain’s largest telecommunication player, Telefonica. Since then it has grown significantly, benefiting from capital recycling in mobile wireless towers from telecommunication players, and is represented in six European markets: Spain, Italy, France, United Kingdom, Netherlands and Switzerland. Cellnex will be a noteworthy beneficiary of mobile technology evolving to 5G due to the following:

- Economies of scale. Cellnex continues to build scale across all markets, but has been particularly successful in Italy. Italy is arguably leading the race to 5G in Europe, having successfully auctioned the 3.6 GHz to 3.8 GHz spectrum recently and with the government declaring five 5G technology pilot cities: Milan, Prato, L’Aquila, Bari and Matera. Through acquisition and organic growth of mobile wireless towers in Italy, Cellnex has grown the tenancy ratio from under 1.20 to 1.39 and has more than 20% market share of total mobile wireless towers.

- High operating margins. Cellnex has established a proprietary master services agreement with some of Europe’s largest telecommunication players, including Telefonica, Wind Tre, Bouygues and Sunrise, which embodies engineering services, network planning and execution, and active equipment management. Cellnex actively tries to increase its margins (and lower rents to its telecommunication counterparties) through land management (either lease re-negotiation or through purchasing land outright), dismantling sites (consolidating the number of mobile wireless towers) and energy efficiencies.

- Growth opportunities. In addition to managing new build of mobile wireless towers (both macro and small cells) to densify the network, Cellnex is actively engaged in fibre backhaul, edge computing and smart cities initiatives. This is illustrated by Cellnex’s joint venture with JCDecaux. Under the JV, Cellnex and JCDecaux facilitate network densification in the form of small cells embedded in street furniture as well as other assets managed by JCDecaux, such as airports, shopping centres, and railway and coach stations.

Conclusion: Communications can be a very attractive infrastructure sub-sector

Clearly, communications is a compelling infrastructure sub-segment, with strong investment demand expected in both developed and emerging markets. Listed communication infrastructure stocks are present in key regions globally, including North America, Latin America, Europe and Asia. In markets such as US and China, listed communication infrastructure have the dominant market share. This is important because it potentially allows investors exposure to different countries, markets and growth rates.

We expect listed wireless mobile tower stocks will offer both developed and emerging markets investment opportunities:

- Developed markets opportunities will present via the transition in mobile technology, namely the transition from 4G to 5G.

- Emerging markets initial investment opportunities will present via increased mobile penetration, with evolution in developed markets (such as 4G to 5G) eventually cascading through to EMs.

Communications infrastructure and mobile wireless towers companies offer a relatively defensive alternative way to participate in increasing global data demand. Active management remains important to appropriately position a portfolio in high quality companies, presenting the strongest infrastructure characteristics such as earnings certainty, inflation protection, high operating margins and sustainable growth.

————