Brad Potter

Summary

Volatility is back in a big way in 2018. A large increase in the VIX is showing an annual level not witnessed since 2007. The sell-off that started in October appears to have been triggered by a number of negative technical forces in the US coming into effect at the same time, which impacted global markets. Technical factors such as systematic selling, hedging of short gamma positions, buyout blackouts prior to reporting season, and record-low market depth all acted in unison. The uncertainties around various macro events — Brexit, China’s slowdown, rising rates in the US, to name a few — led to a collapse in confidence that exacerbated the situation, which had little market depth.

Liquidity in the market is being adversely impacted by a number of different factors that place more downward pressure when volatility rises:

- Market makers now only provide reasonable depth when conditions suit, i.e. low volatility and low-risk periods

- The increase in passive, index and ETFs means that in a falling market this cohort of investors are always selling to rebalance

- The reduction in active investors reduces the number of investors who are buying the dips and value

- The number of low volatility and other esoteric funds that sell when volatility rises has increased.

The selling has been completely disconnected from strong fundamentals in both the US and Australia, with earnings and the economy in both countries remaining resilient and quite strong, albeit with signs of slowing.

The correction during the sell-off looked a little strange compared with the typical ‘risk-off’ pattern (equities fall, bonds rally). A coincident bear market in both equities and bonds is rare. It hasn’t been since 1994, when a stark rise in interest rate expectations triggered equity selling. During the 1994 sell-off, commodity-exposed stocks outperformed as global inflation expectations rose, and the significant interest rate risk saw long-duration growth stocks collapse.

Perhaps the sell-off is a reflection of the need for valuations to adjust to the world of higher interest rates after a long period of low rates driven by government intervention.

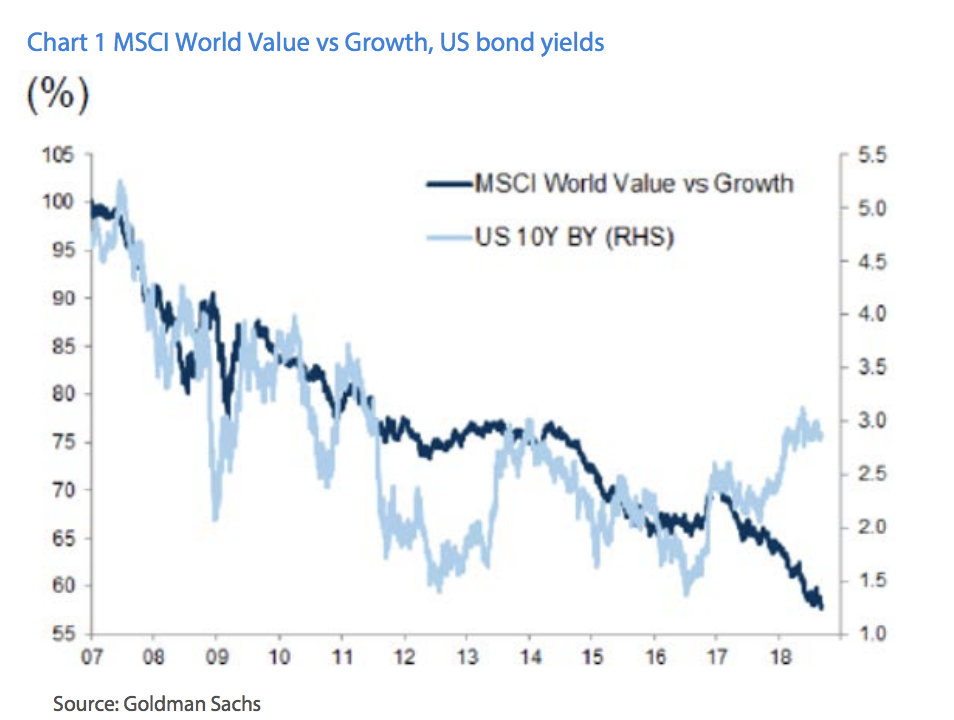

During the most recent sell-off, both growth and value fell with a significant rotation to defensive low volatility and quality stocks that were already priced in ‘bubble territory’. Despite the +16% correction in growth stocks, they are still trading 28% above the 25-year average. Typically, value stocks outperform during rises in bond yields as they tend to be more sensitive to better economic conditions. The relationship has broken down in the latest bond yield increases as illustrated below.

The heavily stretched valuation gap between value and defensive low volatility stocks implies the market is pricing either recession or further deflation concerns. Given our view is that neither is likely in the short to medium term, this provides an attractive entry for rotation in cheap cyclicals.

The combination of the technical factors mentioned, nervousness around both a late cycle slowdown, and a number of global political issues has resulted in the market massively over reacting across many stocks and sectors that display strong fundamentals. The signs continue to point to global growth slowing. However, given the typical drivers of recession, such as an overheating economy or financial imbalances are not evident — expansion in both US and Australia are expected to remain.

The Australian economy continues to have the tailwinds of easy financial conditions with the RBA unlikely to raise rates for at least 12 months. The “chicken little” doomsday scenarios being postulated around credit crunches and housing crashes is highly overstated. The housing correction is healthy after a prolonged rise and, as the RBA pointed out in the most recent Financial Stability Review, households have built up decent buffers, and have generally borrowed less then they need. Given a tight labour market and further fiscal stimulus from the forthcoming election cycle, we expect consumer income to rise.

Fundamental active value managers often struggle during periods of bubble like conditions and/or when the market ignores fundamentals. The current conditions are a combination of both where growth has outperformed value for the longest time in history and is thus in bubble territory, and nervousness around global growth and political instability is resulting in stocks overreacting on the downside.

PE expansion in the expensive stocks has endured for some time, as shown in Chart 2. In fact from early 2017, while growth stock PEs re-rated upwards, value stocks have had their PEs de-rated. This is not driven by earnings growth, but concerns about subdued economic growth driving the market to sell down economically sensitive stocks (in the value bucket), and buying up growth stocks that are perceived to be immune to the economic cycle. The differential in PE ratios is currently about double the historical norms, and is clearly not sustainable.

By Brad Potter, Head of Australian Equities

———–

This document is prepared by Nikko Asset Management Co., Ltd. and/or its affiliates (Nikko AM) and is for distribution only under such circumstances as may be permitted by applicable laws. This document does not constitute investment advice or a personal recommendation and it does not consider in any way the suitability or appropriateness of the subject matter for the individual circumstances of any recipient. This document is for information purposes only and is not intended to be an offer, or a solicitation of an offer, to buy or sell any investments or participate in any trading strategy. Moreover, the information in this material will not affect Nikko AM’s investment strategy in any way. The information and opinions in this document have been derived from or reached from sources believed in good faith to be reliable but have not been independently verified. Nikko AM makes no guarantee, representation or warranty, express or implied, and accepts no responsibility or liability for the accuracy or completeness of this document. No reliance should be placed on any assumptions, forecasts, projections, estimates or prospects contained within this document. This document should not be regarded by recipients as a substitute for the exercise of their own judgment. Opinions stated in this document may change without notice. In any investment, past performance is neither an indication nor guarantee of future performance and a loss of capital may occur. Estimates of future performance are based on assumptions that may not be realised. Investors should be able to withstand the loss of any principal investment. The mention of individual stocks, sectors, regions or countries within this document does not imply a recommendation to buy or sell. Nikko AM accepts no liability whatsoever for any loss or damage of any kind arising out of the use of all or any part of this document, provided that nothing herein excludes or restricts any liability of Nikko AM under applicable regulatory rules or requirements. All information contained in this document is solely for the attention and use of the intended recipients. Any use beyond that intended by Nikko AM is strictly prohibited. Nikko AM Limited ABN 99 003 376 252 (Nikko AM Australia) is responsible for the distribution of this information in Australia. Nikko AM Australia holds Australian Financial Services Licence No. 237563 and is part of the Nikko AM Group. This material and any offer to provide financial services are for information purposes only. This material does not take into account the objectives, financial situation or needs of any individual and is not intended to constitute STOP MAKING SENSE: THE STATE OF VOLATILITY IN MARKETS en.nikkoam.com 4 personal advice, nor can it be relied upon as such. This material is intended for, and can only be provided and made available to, persons who are regarded as Wholesale Clients for the purposes of section 761G of the Corporations Act 2001 (Cth) and must not be made available or passed on to persons who are regarded as Retail Clients for the purposes of this Act. If you are in any doubt about any of the contents, you should obtain independent professional advice.