Weekly market update – week ending 15 March, 2019

Investment markets and key developments over the past week

Global share markets rose over the last week helped by benign economic data. Australian shares slipped though with consumer and financial shares down on worries about the economy. Bond yields were flat to up globally but fell in Australia with the 10-year bond yield falling back below 2% for the first time since 2016 as weakening economic data adds to expectations for RBA rate cuts. While gold and copper prices slipped oil and iron ore prices rose. The $A also rose slightly as the $US slipped.

It looks like the timing of a US China trade deal is slipping into April at the earliest on disagreements about enforcement, tariff reductions and a meeting between Presidents Trump and Xi (the Chinese side would naturally be worried that Trump may “walk”). But a deal is still likely as it’s in both sides interest with US Trade Rep Lightizer saying negotiations are in the final stage. The indications are that it’s likely to be more than just a superficial commitment by China to buy more US goods but include reduced tariffs, reduced non-tariff barriers, relaxed or eliminated joint venture requirements, better market access and bans on stealing intellectual property. While we ultimately expect a deal, news of setbacks or delays have the potential to trigger a pullback in shares with a deal looking like its already factored into markets.

Don’t panic! don’t panic! – while the UK parliament rejected PM May’s Brexit deal a second time, it has also voted down a no deal Brexit and supported a short extension to the Brexit date so it can have another go at voting on May’s twice rejected deal! Clearly May is trying to block the Brexiteers into supporting it as if they don’t parliament will take over increasing the odds of no Brexit. While the rejection of a no deal Brexit was positive the margin was low, the vote was non-binding and in any case there is no majority support in Parliament for any one deal. So while the British pound hit a 9-month high in the last week, the Brexit comedy has a long way to go yet to being resolved. The best solution would be to have another referendum – which would likely see Bremain win. For investors on the other side of the world though its all just an entertaining sideshow having little impact on global markets (beyond the UK itself).

Bigger tax cuts on the way in Australia in the April Budget. The Federal Government’s Mid-Year Economic and Fiscal Outlook set aside around $3bn a year in revenue “decisions taken but not yet announced” starting from next financial year and this presumably refers to tax cuts. On top of this, budget data up to January shows this year’s budget tracking around $3bn a year better than MYEFO projected and the rise in the iron ore price is likely to have added to this although it may be partly offset by a downgrade to economic growth, employment and wages assumptions for 2019-20. Overall though it looks like there is scope for around $6bn in extra fiscal stimulus in 2019-20 that would basically leave the budget projections into a surplus unchanged. It would make sense for the Government to do this given the loss of growth momentum in the economy, but it would only be around 0.3% of GDP so a pretty small stimulus and the election would add a bit of uncertainty as to its timing. That said this is on top of the $3bn in tax cuts already legislated from the May Budget last year. So, all up it would amount to a fiscal stimulus of around 0.5% of GDP, most of which would go to the household sector just at the time it needs it given falling house prices and a likely rise in unemployment. It won’t be enough to head off the need for RBA rate cuts, but it will help.

Was the Australian house price boom all due to lower interest rates? RBA researchers put out a great paper modelling the Australian housing market over the last week. Two things particularly are worth a mention. First the model suggests that most of the boom in Australian house prices since 2011 was due to lower interest rates. While I totally agree lower rates played a big role in the surge, the only problem is that Australian house price to income ratios ended up in 2017 being way way above those in comparable countries who have even lower interest rates. So despite the model – which is not fool proof – it seems clear to me that other factors have actually played a bigger role. These include the initially slow supply response, foreign buying, SMSF buying and aspects of the tax system all of which helped drive speculative buying ultimately culminating in a bubble in some cities. Second, the RBA paper highlights the risk that if home owners adjust their 10-year expected real house price gain from say 2.5% pa to zero, real house prices could fall by a third. Of course, rate cuts & other measures can help offset this, but the sensitivity analysis highlights the risk of FONGO (fear of not getting out) taking hold. Net rental yields of just 1 or 2% may be okay for investors when property prices are expected to rise at a decent rate, but they are not okay if investors revise down their capital growth expectations in response to now falling prices. If this occurs yields will need to adjust upwards via prices falling even further.

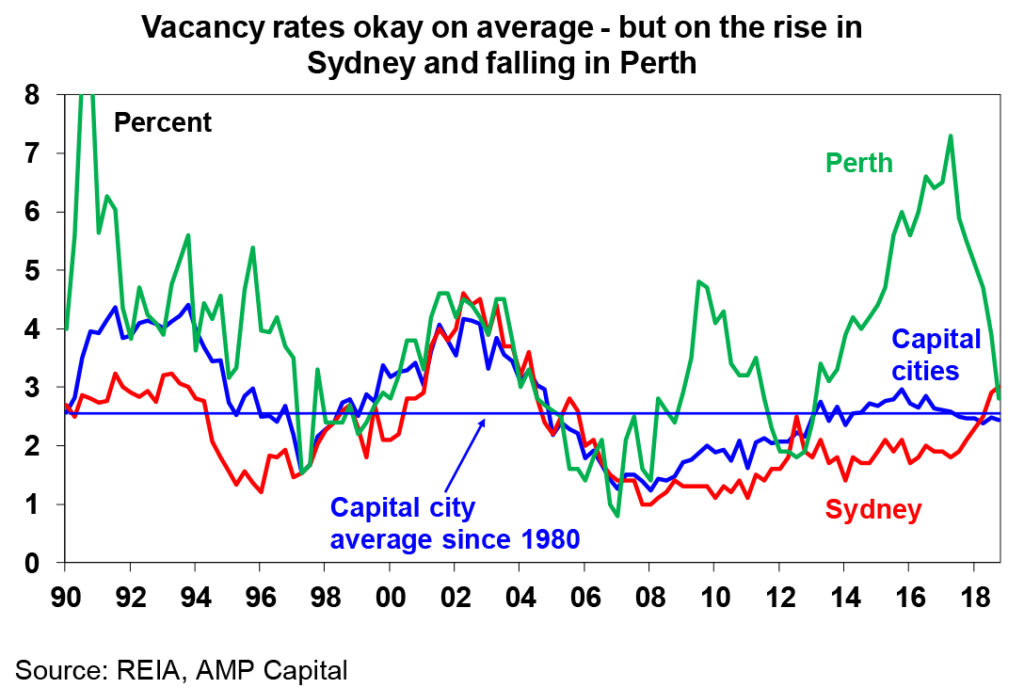

Meanwhile the divergence in the Australian property market is highlighted by rental property vacancy rates which are pushing higher in Sydney and plunging in Perth which explains why rents are falling in Sydney and starting to rise in Perth all of which is consistent with further falls in Sydney property prices but a (slowly!) improving outlook for Perth property prices after their plunge since 2014.

Major global economic events and implications

US data releases mostly pointed up over the last week with retail sales, capital goods orders, construction spending all bouncing back in January and small business optimism up a bit in February. Despite this March quarter GDP growth looks to be very weak (with the Atlanta Fed’s GDP Now estimating growth of just 0.4% annualised) not helped by the weak base set in December with eg December retail sales revised down even further. However, the March quarter is well known for soft growth which may be partly weather related and at least growth indicators are pointing to a rebound. Meanwhile, inflation remains benign with core CPI inflation falling to 2.1% year on year in February which translates to inflation of around 1.8%yoy on the Fed’s preferred measure. All of which remains consistent with the Fed remaining in pause mode on rates.

Eurozone industrial production also perked up in January, with Germany still weak but production up in France, Italy & Spain.

The Bank of Japan maintained its ultra-easy monetary policy as widely expected & downgraded its economic outlook.

Chinese January/February activity data was on the soft side with a further slowdown in industrial production to 5.3% year on year, a rise in unemployment to 5.3%, unchanged growth in retail sales of 8.2%yoy and just a slight acceleration in investment growth to 6.1%. Chinese GDP growth is likely to have slowed a bit further this quarter but should pick up into the second half as policy stimulus impacts and there are already signs of this in the pick up in investment growth and credit growth averaged over January and February.

Australian economic events and implications

Australian data was soft over the last week with falls in business confidence, consumer confidence and housing finance. The ongoing fall in housing finance indicates that tight credit conditions are continuing. The housing downturn along with weak economic news generally looks to be feeding into consumer confidence. The risk is that weakening business conditions will damage the nascent recovery in business investment which is a source of growth for the economy.

What to watch over the next week?

In the US, expect the Fed (Wednesday) to leave interest rates on hold and indicate that the pause will continue for some time yet. But even more significantly its likely to make some reference to moving to a framework that targets average inflation over time with the implication that it will allow a period of inflation above 2% to make up for all the years below) and there is a good chance that it will indicate a tapering in its process of balance sheet reduction (or quantitative tightening) in the second half ahead of ending it early next year. All of this is likely to be taken as dovish by investment markets.

On the data front in the US expect a further slight rise in home builder conditions (Monday), some improvement in the Philadelphia Fed’s manufacturing conditions index (Wednesday) and solid readings for March business conditions PMIs (Friday) and a rise in existing home sales (also Friday).

Eurozone manufacturing conditions PMIs (Friday) will likely show a rise after falling below 50 in February.

Japanese core inflation for February (Friday) is expected to remain weak at 0.4% year on year keeping the BoJ ultra easy.

In Australia, expect ABS data to show a 2% fall in house prices (Tuesday) for the December quarter consistent with private sector surveys and February labour force data (Thursday) to show a 5000 gain in jobs and unemployment rising to 5.1%. The CBA business conditions composite PMI for March is likely to have remained weak. The minutes from the last RBA board meeting (Tuesday) will likely maintain a neutral bias on interest rates.

Outlook for investment markets

Share markets – globally & in Australia – have run hard and fast from their December lows and, with global economic data still soft, they are vulnerable to a short-term pullback. But valuations are okay, and reasonable growth and profits should support decent gains through 2019 as a whole helped by more policy stimulus in China, Europe and Australia and the Fed pausing.

Low yields are likely to see low returns from bonds, but they continue to provide an excellent portfolio diversifier. Expect Australian bonds to outperform global bonds.

Unlisted commercial property and infrastructure are likely to see a slowing in returns over the year ahead. This is likely to be particularly the case for Australian retail property.

National capital city house prices are expected to fall another 5-10% into 2020 led again by 15% or so price falls in Sydney and Melbourne on the back of tight credit, rising supply, reduced foreign demand, price falls feeding on themselves and uncertainty around the impact of tax changes under a Labor Government.

Cash and bank deposits are likely to provide poor returns as the RBA cuts the official cash rate to 1% by end 2019.

The $A is likely to fall into the $US0.60s as the gap between the RBA’s cash rate and the US Fed Funds rate will likely push further into negative territory as the RBA moves to cut rates. Being short the $A remains a good hedge against things going wrong globally.

By Shane Oliver