Relationship breakdowns require financial advice and a strategy to provide for both the short and longer term financial future.

When a couple separate with the intention of divorce, the importance of both parties seeking legal advice is well established. However, arguably it is just as vital that both members of the couple obtain financial advice including reviewing and revising their financial position and objectives and establishing a financial strategy to provide for both the short and longer term future.

In this article, we outline how a financial adviser could assist their client through this difficult phase in their life.

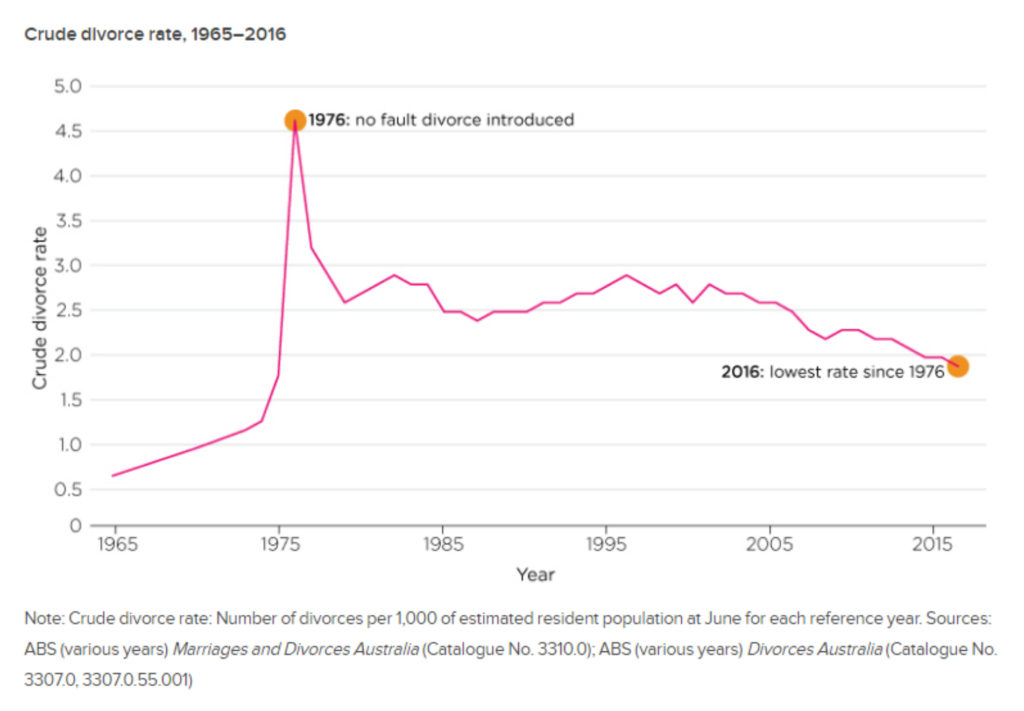

Interestingly, the divorce rate in Australia has been generally reducing since 1976, reaching the lowest rate of 1.9 divorces per 1,000 individuals in 2016. This rose slightly to 2 divorces per 1,000 people in 2017.

For those marriages that ended in divorce in 2017, the median age of males at divorce was 45.5 years of age and 42.9 years of age for females. The median duration of marriage to divorce was 12.0 years in 2017.[1]

These statistics suggest that couples separating are likely to have built up a stock of shared assets during their marriage and young children may be involved, making the separation process more complex and the need for advice more critical.

Independent financial advice

For existing clients, it is unlikely to be appropriate for both parties to retain the same financial adviser. Having separate advisers is generally preferable to maintain privacy and minimise conflict. One member of a couple may therefore need to seek an alternative financial adviser for their needs during the separation process.

Often in relationships, there is one member of the couple who has a greater understanding and interest in managing the finances. However, upon separation, both parties need to appreciate and understand their financial position and asset ownership structures. The financial adviser can assist with this education piece.

Is there a binding financial agreement?

A binding financial agreement (BFA) is a legal agreement made between parties to a marriage or de facto relationship about financial arrangements should that marriage or relationship breakdown. Able to be made before, during or after a marriage or de facto relationship, a BFA can state how assets, liabilities and financial resources will be divided should the relationship breakdown.

By making a BFA, the parties contract out the right they would otherwise have to ask a Court to make financial orders.

If clients do not have a BFA, they can still make one post separation with the assistance of their solicitor.

If the parties cannot agree or do not wish to make a BFA, financial orders (relating to property, maintenance and/or child support) will need to be made by a Court and the parties’ respective lawyers.

Insurance

Following separation, insurance needs are likely to change. For example:

- In a previously dual income family, in the event of not being able to work due to illness or accident, the client will no longer be able to rely on their spouse or partner’s income, making Income Protection a more critical cover.

- The level of lump sum cover such as life insurance may need to be adjusted based on the change in asset, debt and income levels.

A comprehensive insurance review to ensure it remains appropriate for the client’s new position and update of beneficiaries is important.

Estate planning

Separation alone will not cause a Will to be invalid even if the client has bequeathed all assets to their now former spouse or partner. The effect of divorce on a Will varies depending on the state in which the client resides.

Therefore, separation should be a key trigger for a client to review their estate plan to ensure that it continues to reflect their needs and intentions. A will and Power of Attorney both need to be addressed, as well non estate assets such as superannuation, a family trust and any joint assets. The client may wish to update their affairs to remove their former spouse or partner as a life insurance and superannuation beneficiary, revoke any gifts to them in their Will and appoint another person as their attorney and/or executor of their estate.

A financial adviser can work with their client to update their estate plan in conjunction with a lawyer or estate planning specialist.

Assets and investments

The client needs to take stock of the couple’s financial position and combined list of assets, income and liabilities. This information is important for the lawyers in finalising the property settlement.

A financial adviser can assist with ensuring the valuations are correct and support the client in understanding which assets may be suitable to retain in meeting their revised financial and lifestyle objectives.

One point to note is if the couple have a property in joint names and it is to be transferred to each other (for example, under the BFA), a name can usually be removed from the title without having to pay stamp duty.

Following the separation of assets, it may be timely for the client to review their assets and underlying investment mix. Their appetite for risk and investment timeframe may have changed in light of their post separation position and adjustments may be required.

Superannuation

The superannuation splitting law treats superannuation (super) as a different type of property. Most[2] separating couples are able to value their super (using information obtained from their super fund(s)) and split a super payment or, sometimes, a super interest to create a new interest or entitlement for the non-member spouse or partner. Super interests which exceed $5,000 or pay a non-commutable pension or annuity of at least $2,000 per annum are able to be split. Splitting is not mandatory and the couple could instead retain their own super interests and offset the division of other property of the relationship.

Splitting super to a former spouse or partner does not mean it can be withdrawn and paid out as cash. The super remains subject to preservation laws and the benefits split to the former spouse or partner cannot be accessed until that individual meets a condition of release (for example, permanent retirement after reaching preservation age of 56 or turning age 65).

Options for splitting super

A couple can make a superannuation agreement or obtain a court order to split a super payment or a super interest.

A superannuation agreement may be a stand alone document or form part of a BFA. Both parties must instruct their lawyer to sign a certificate, stating that independent legal advice about the agreement has been given.

In the absence of an agreement, a court order can be obtained to split super from the Family Court or Federal Court of Australia. Court orders can be either consent orders (the parties agree on the terms and it is registered by the court) or contested (the terms of the order are determined by the court).

The superannuation agreement or court order must outline how super is to be split. Splitting a super payment to the former spouse or partner could be done by specifying a fixed dollar amount, a method for calculating an amount, or a percentage of a payment.

If a client has a defined benefit fund, it can be more complex and the division of the super may be deferred until such time as the benefit becomes payable and can be crystallised (usually at retirement) by placing a payment flag on the account.

A super split may be subject to tax implications as well as administrative fees for the transfer. It is important that the client seek independent legal and financial advice before entering into any agreement to split super.

Meeting future income needs

The financial and legal implications of separation or divorce can lead to several obstacles that the client needs to overcome. The same income from before the separation or divorce is now paying for two households and two sets of bills and expenses. Thus, lifestyle or spending adjustments may be necessary.

A client who has been a stay at home parent might have to re-enter the workforce or one working part time may need to consider an increase in hours to provide additional cash-flow to meet future ongoing expenditure.

In addition, a financial adviser may be able to help the client with meeting their income needs in their post settlement financial position:

- Budgeting and debt repayment strategies can be re-addressed and priorities reassessed.

- A client over age 55 could consider commencing a Transition to Retirement (TTR) pension from their super if they need more income.

- Centrelink benefits can be explored. If there are dependant children involved, benefits such as Family Tax Benefits may be available. Older clients who are not working may consider eligibility for NewStart Allowance or Age Pension.

- When there are children involved, one member of a separated couple may need to pay the other Child Support. The level of child support depends on a number of factors, including the adjusted taxable income of each party, how much time the children spend with each parent, and the age and number of children. It can be dealt with in a BFA.

- Spousal maintenance may be payable and application for this can be made via the Family or Federal court. Under the Family Law Act 1975, a person has a responsibility to financially assist their former spouse or partner, if that person cannot meet their own reasonable expenses from their personal income or assets. This obligation can continue after separation and divorce and the level of support depends on what the other party can afford to pay. It can be dealt with in a BFA.

Rebuilding financial savings

Separation can have significant implications on a client’s cash-flow and financial position. Initially, the client may need to defer their previous long-term savings objectives for more immediate short-term strategies which address their current situation.

However, it is important to also review the client’s longer term financial goals and retirement plan. Retirement timeframes, saving and super contribution strategies and retirement income objectives may need to be adjusted. Sound financial advice can assist the client in establishing and working towards these new goals.

———-

[1] ABS, Marriages and Divorces, Australia, 2017

[2] De facto couples in Western Australia cannot split their super, instead, super is considered a financial resource to be taken into account when assessing the overall division of assets of the couple.