State Street says Brexit uncertainty keeps UK growth below trend

What are the chances of a Second Brexit Referendum?

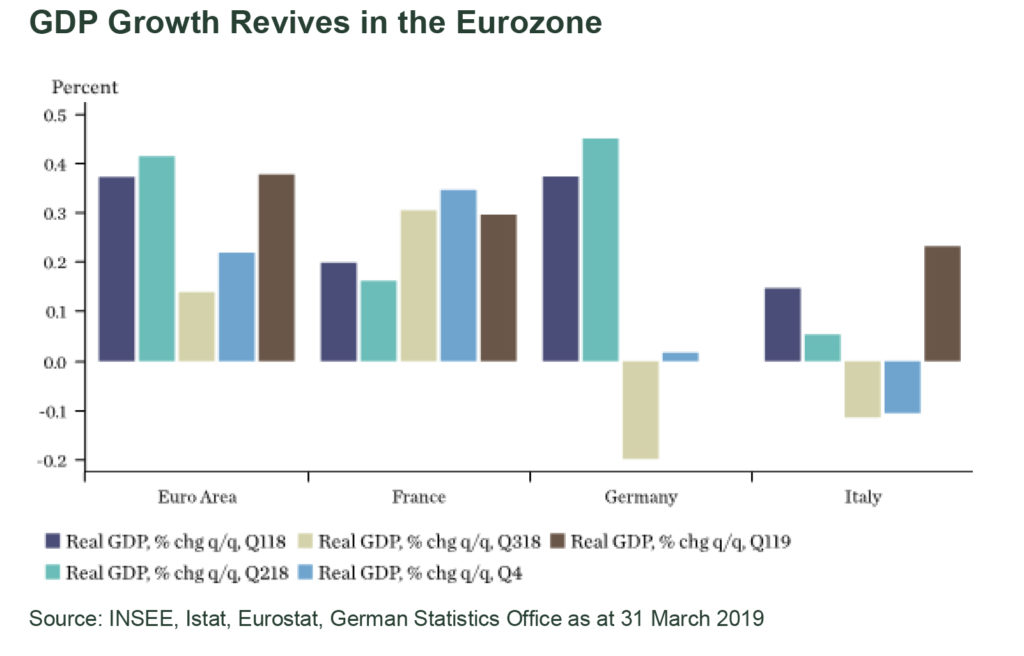

With trade deals stalling it’s easy to forget about Brexit. However, Europe needs careful consideration and due attention. While there are signs of Eurozone stabilisation, political uncertainty, especially around Brexit, persists.

If Mrs May’s Brexit deal/ a parliamentary consensus is agreed before European Parliament elections towards the end of May, the Bank of England may take the opportunity to hike rates earlier than expected given the loose fiscal policy recently announced and tighter labor market pushing up inflation. However, even with a deal on the table, we would expect the Bank to wait for growth to pick up, which could take time if political turmoil ensues. Conversely, a no deal in October 2019 (not our current thinking) could have significant negative impact on the growth outlook and would likely lead to a cut.

We have already seen last minute compromise efforts between the Labor and Conservative parties fail and an end-March Brexit did not happen. The EU granted the UK a flexible Brexit extension to 31st October 2019 (in between May’s end-June and Tusk’s 1 year starting points), with the UK able to leave on the 1st of any month following a Withdrawal Agreement ratification. However, the EU demanded the UK leave on 1st June if it does not participate in EU elections (23rd May).

Economically, the extension is good from the immediate perspective of no immediate cliff-edge; however growth will likely be hit by Brexit uncertainty and will stay below trend for longer. Politically, the extension will add fuel to the turmoil that exists and creates a higher probability of leadership and or government change in the foreseeable future. May looks to have averted the immediate risk of another internal coup as the 1922 Committee were looking to alter the current rules around a no confidence vote to oust her. However, they opted against and instead will likely press the Prime Minister to outline a timetable for her departure. She cannot be challenged as leader of her own party until December, which will further deepen the split within the conservative party. However, if no agreement is in place before the EU elections, it is likely she will have to resign.

Much will hinge on whether the UK participates in the EU Elections. The political cost to the Conservative party of doing so will be high with UKIP (leave) and TIG (remain) are likely to gain a considerable share of the vote. Labour also stands to lose out if their Brexit policy remains muddled. Therefore there is incentive for cross-party consensus between Labour and the Conservatives (e.g. EU principle agreement to a customs union). Labour would be very careful to try to future-proof this. After all, May has said she would resign, and Labour would be concerned a hard-line Brexiteer replacement would renege on any deal.

With May wanting to avoid European Parliamentary on 23rd May, we may see another series of indicative votes being drawn up or a more recent suggestion has been an attempt to write her Withdrawal Bill into law, with opponents able to add legislation through amendments, therefore standing a chance of passing. This would require Labour members voting for the bill. If she doesn’t put the bill to Parliament in the next couple of weeks, there’s no way the U.K. can leave before the EU poll.

So what are the chances of a Second Referendum? No politicians have come across as sufficiently supporting this and it would exacerbate social and political tensions although Labour is making a decision on whether to back a public vote on a deal. However, it could in fact be forced on the government in order to buy enough time to permit the EU to grant a further extension to the deadline, come October. A referendum would pose a risk of remain, which Brexiteers might find hard to accept, and of a no deal outcome, which many MPs might find hard to accept. The path forward is unclear and additionally clouded by the possibility of a general election!

With headlines crowded by the trade war between the US and China it’s easy to forget about everything going on in Europe but there is certainly plenty to keep an eye on.

Portfolio Positioning and Performance [1]

April saw global markets deliver positive returns continuing their positive start to the year with both local and global markets faring well. Global markets again posted positive returns as risky assets continued to benefit from a more sanguine environment with a more dovish US Federal Reserve and an improving view on global fundamentals providing support. In equity markets locally, we saw a positive month with the S&P/ASX 200 Index up 2.4% for the month of April and up 13.5% year to date. The US also posted positive returns in April with the market (MSCI US Net total return local) up 4.0% and up 18.3% year to date. Most major markets were positive in April with Europe (MSCI Europe Net total return local) and Japan (MSCI Japan Net total return local) up 4.1% and 2.0% respectively. Emerging markets (MSCI EM Index Net total return local) was also up with a 2.1% gain. Local based fixed income returns also saw positive returns again in April with Australian government bonds up for the month after negative yield moves in shorter tenors. Our investments in Emerging markets bonds was marginally positive for the month and is positive since the start of the year. Looking into our positioning across the portfolios for the month of April, on average, the Growth assets allocations have been approximately 65% for State Street Multi-Asset Builder Fund and 43% for State Street Multi-Asset Income Fund. Our exposure preferences in April were again an overweight in global equities relative to fixed income. Performance wise, with positive results seen across most risky assets, the funds delivered positive returns in April.

——–