It’s time to include the fourth, and largest, pillar of retirement funding – home equity

Australia’s retirement income policy has been traditionally framed as having three pillars: superannuation, non-superannuation savings and the Age Pension. However, for many Australian baby boomers these three pillars provide inadequate resources to fund 25+ years of retirement. Household Capital explains why it’s now time to include the fourth, and largest, pillar of retirement funding – home equity.

Australians are experiencing a major societal transformation; the baby boomers are reaching retirement. Around 5.5 million people born between 1946 and 1964, will need long term funding. While we are living longer than ever, this presents a real conundrum – many of this cohort simply don’t have sufficient savings to fund a comfortable retirement for their projected lifespan.

Living longer, not necessarily better

The life expectancy of Australians in retirement has almost doubled in the last 150 years thanks to better lifestyles and medical breakthroughs. Since the introduction of compulsory superannuation in 1992, Australians at retirement have gained an extra decade of longevity – and an extra decade to fund.

Figure one shows the range of expected increases in longevity after retirement for Australian men and women based on current assumptions. It is estimated that retirees aged 65 now will live on average until 84 for men and 87 for women.

The blessing of longevity is a new and extended phase of life which will endure well past 90 for many people. The curse is that individuals need to plan for 25-30 years of retirement.

Super alone is not super enough

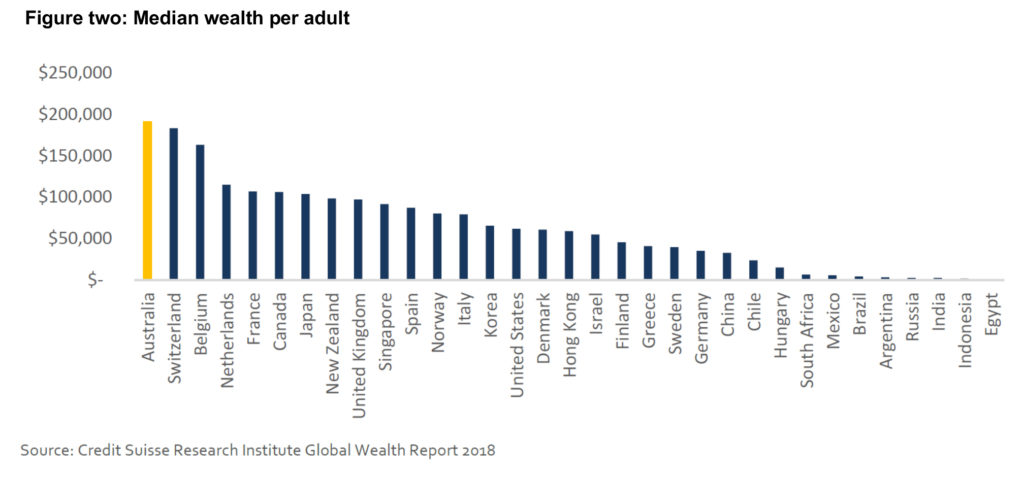

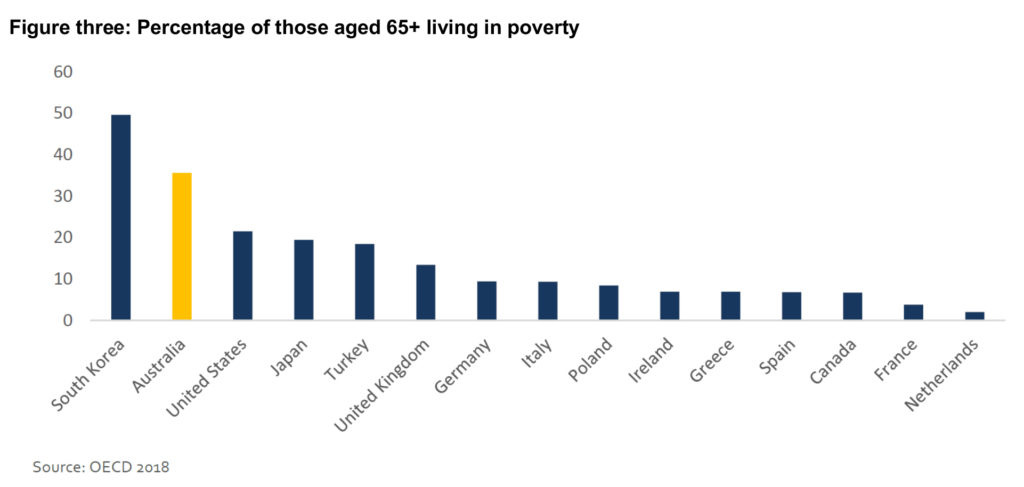

Despite high total median wealth (figure two), retired Australians experience high levels of relative poverty (figure three).

To enjoy more good years of life in retirement, adequate resources are required. The Australian superannuation system was designed to supplement the pension with private, account-based savings from wage contributions. While the total superannuation savings required to fund an adequate lifestyle for baby boomers is contested, the introduction of superannuation contributions occurred only part-way through their careers at lower levels.

The 3% annual contribution in 1987, followed by the Superannuation Guarantee increasing to 9% by 2002, has led to a major shortfall in available assets to fund retirement. Baby boomers also missed out on the benefits of compounding returns over time.

As a result, the median household superannuation balance for retiring Australians currently sits around $200,000[1], estimated to support a ‘comfortable’ retirement income for only 10-15 years.

This inadequacy of superannuation savings to support a quality retirement lifestyle is a major challenge. Even more challenging is the prospect of relying solely on the Age Pension to fund retirement.

The age pension “fails to provide a decent standard living for approximately 1.5 million older Australians…some pensioners are taking drastic measures in order to make ends meet – they are turning off hot water in summer, blending food because they can’t afford a dentist and choosing between food and medication.”

Source: Per Capita 2016

For most Australians, the majority of their wealth is tied up in their home equity; in total, there is more than one trillion dollars in untapped home equity owned by Australian retirees[2].

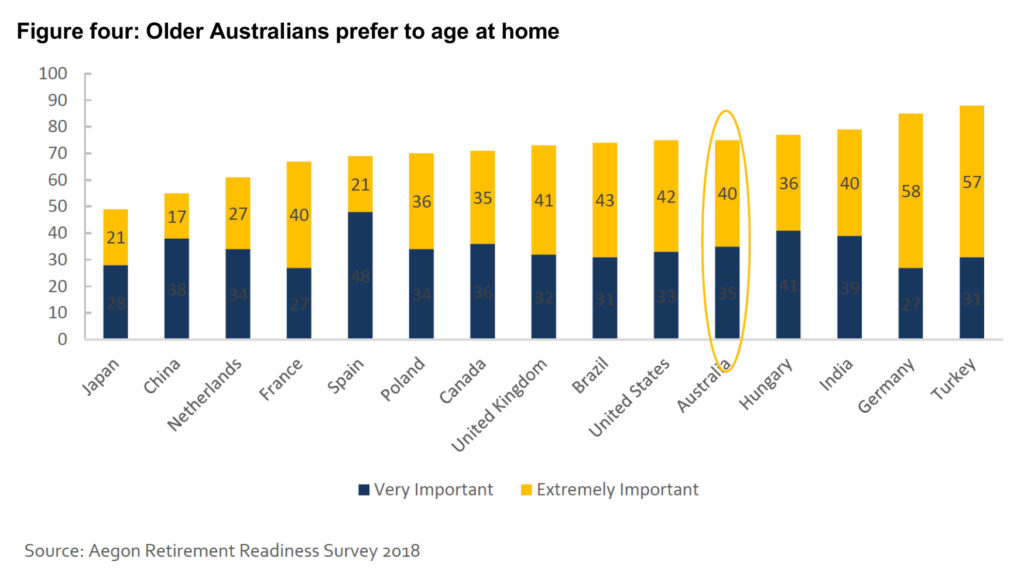

Long, healthy lives enable Australians to spend a greater part of their retirement living independently. Most retirees wish to stay in their own home as they age, as illustrated by figure four, and their untapped savings are a valuable resource that could be utilised to provide improved retirement funding.

Importantly, in-home poverty, forced downsizing or premature relocation to aged care may undermine the lifestyle and wellbeing of retirees and the economic burden of retirement. New approaches that can help Australians remain at home and meet the challenges of both longevity and retirement funding adequacy will play an important part of meeting the needs of many older Australians.

Home versus super

Figure five shows the total average superannuation versus home equity for Australian households during the course of work and retirement. Within 10 years of retirement, superannuation savings are largely depleted.

For Australian homeowners at retirement, the average household home equity is typically almost twice the value of superannuation. By the time retired cohorts have reached 75+ years of age, home equity savings have grown to over six times the value of superannuation.

On average, Australians’ superannuation lasts about 10-15 years after which many Australians in retirement can expect a further 10-15 years of underfunded or inadequate retirement supported by the Age Pension.

Assets, income and contingency funding

Many economists and superannuation executives continue to ask, “Why do retirees die with so much wealth left in super?” The simple answer is that accessible savings in superannuation are Australian retirees’ main way to manage both contingency funding and longevity risk. No-one can tell when they will die or the major expenses they may incur along the way. While retirees do draw down their super and retain a contingency buffer, they also die with far too much wealth tied up in their homes.

Currently, retirees have no ability to transform the adequacy of their retirement resources to responsibly access their accumulated wealth throughout retirement. To do that, we need to consider ways to provide access to the largest pool of savings for most Australian retirees – their own home equity.

How can investors access home equity?

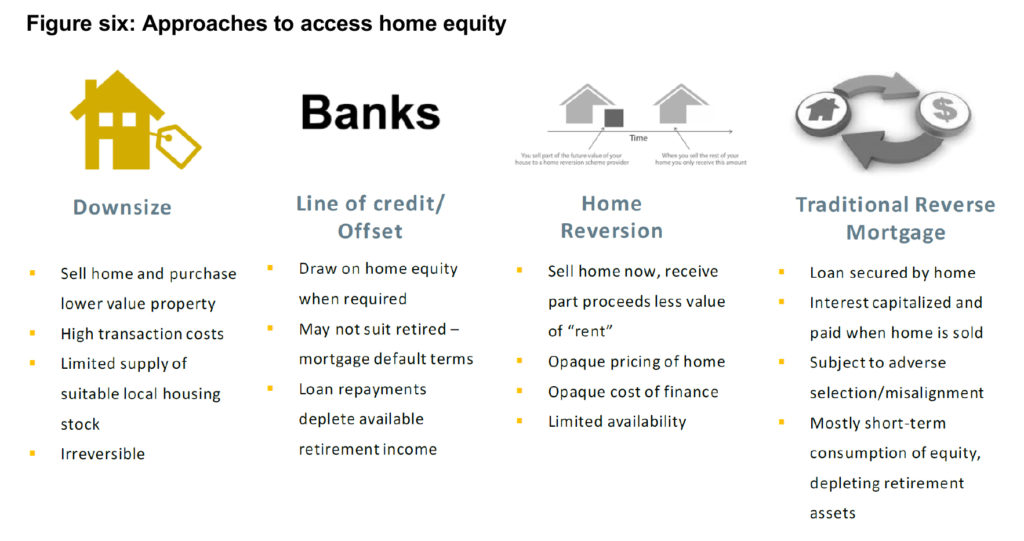

There are four main approaches used by retirees to access home equity, as shown in figure six. Each of these approaches has significant downside in terms of cost of access, security of tenure in the home or the ability to fund a long term retirement income.

Downsizing

Selling the family home, moving to a lower-priced property and using the differential to fund retirement is often suggested as a major opportunity to improve access to home equity. Several limitations to this approach should be noted.

Australian retirees are reluctant to downsize, identifying their current home as optimal for ageing in place. In many areas, there is limited available stock of lower-priced accommodation, meaning that retirees would need to leave their community and social support structures to capture meaningful proceeds from downsizing.

In many cases, legal and transaction costs, stamp duty and moving expenses erode the realised value of downsizing. Very importantly—despite recent downsizing concessions for retirees—tax and transfer systems result in assets released from home equity downsizing having a potentially adverse impact on assets and income tests for access to the age pension. Finally, downsizing is highly complex and disruptive.

“There is a general lack of affordable downsizing options for older Australians”

Source: Productivity Commission 2015

Currently, around 20% of Australian retirees downsize. The federal government has introduced incentives to facilitate downsizing by allowing $300,000 from the proceeds to be contributed to superannuation. Over time, the number of Australian retirees downsizing is not expected to increase to more than 30%; this leaves 70% who may need to access part of their home equity to adequately fund their retirement.

Home loan line of credit or offset facilities

Some working Australians nearing retirement establish or preserve a line of credit or offset facility against their home mortgage. In a recent example, we encountered Jim, a recently retired 72 year old who was relying on an offset facility. Three years ago Jim purchased a dual-accommodation unit to house himself and his dependent, mentally disabled adult son. At that time he was 69 years old and working as a self-employed small business operator. Jim recalled the extensive effort required to obtain a bank mortgage to purchase the unit and offset the majority of the loan. From the age of 72 to 80 Jim plans to live on the age pension and his superannuation, by which stage his super would run out. From the age of 80 to 90 he plans to draw down on the offset facility. Jim is unable to plan for himself or his son beyond this age, nor make plans for his son if he had to transition to aged care during that period.

Several problems arise in the current use of lines of credit to fund long-term retirement. For most retirees, new mortgages with significant offset facilities are hard to establish at or near the point of retirement. Standard bank terms mean that retirement or other loss of income may be grounds for default, repossession and eviction, undermining the security of tenancy sought by the retiree. While an offset provides some form of contingency funding, the moment it is drawn down for regular income or an unexpected expense, interest payments on the loan start again. Rather than increase available retirement income, the interest expense of regular or “forward” mortgages depletes available income during retirement. Many banks are now transferring interest only loans to interest + principal, exacerbating the drain on available income.

In these ways a line of credit or offset approach to accessing home equity can put at risk both key retirement objectives of secure housing and reliable income. Few Australians appear to be taking this path – overall around 400,000 Australians over the age of 65 are currently repaying residential mortgage debt. This potentially reflects wider concerns about the ability of the traditional banking system to deal with the particular needs of income-poor, but asset rich, retirees.

Home reversion schemes

The third type of home equity access is home reversion, an approach which is less frequently used than traditional bank reverse mortgages. In some cases, the home is sold at a nominal market price and the purchase price is transferred in stages, over an agreed period, while the owners remain at home.

At its simplest, the purchaser’s staged payments are reduced by the deferred time value of money while the seller receives full or partial rent reduction of their own home. In other cases, a portion of the residential property is sold to the “lender”, discounted by the value of a “lifetime rental” on that portion of the property. Typically, retirees receive 25-40% of the value of the property, depending on their age and other factors. Once paid upfront, the lifetime rental may be partially reimbursed or extended depending on premature death or unexpected longevity.

There are several potential problems with this approach. Pricing the property in an off-market transaction may not be transparent and may work to reduce the value of the home realised by the retiree. While vendors claim a “no debt” approach, a time-value of money is still applied. Calculation of the “rental” and adjustments for unusual longevity events makes it difficult to apportion risk between parties and to communicate those costs and risks to the vendor. Home reversion schemes have, to date, applied a significantly higher cost of capital to access home equity.

Finally, the homeowner no longer owns 100 percent of their home; as a result, they don’t get to participate in any increase to the value of their property.

Traditional bank reverse mortgages

The majority of the current Australian (and international) market comprises standard lump sum reverse mortgages. Simply, the lender provides a lump sum of principal up front, secured against the residential property. Interest accrues to the lump sum and compounds during the term of the mortgage. ASIC’s 2018 review of the reverse mortgage sector found most providers historically focused on the borrower’s short-term objectives, with limited attention paid to future needs. This left many borrowers cash poor and asset depleted throughout the remainder of their lives.

There is no default risk as there are no repayments, and insurance costs for the dwelling are usually allocated to the owner. On relocation or death the mortgage is discharged, and the principal plus accrued interest is recovered. Loan-to-value ratios are usually set statutorily. In all jurisdictions, lenders are prevented from forcing owners from their dwellings or claiming more than the ultimate value of the secured property; this is known as the No Negative Equity Guarantee (NNEG). The lender takes on the risk that the compounded capital and interest increases above the equity value of the home security.

In Australia, reverse mortgages were provided by CBA (and BankWest), Westpac (and St George/Bank of Melbourne), and Macquarie Bank. Heartland Bank (NZ) provided reverse mortgages in Australia based on wholesale funding from CBA. In the past 12 months, CBA, Westpac and Macquarie have all announced their exit from the Australian reverse mortgage market.

Reverse mortgages – the overseas experience

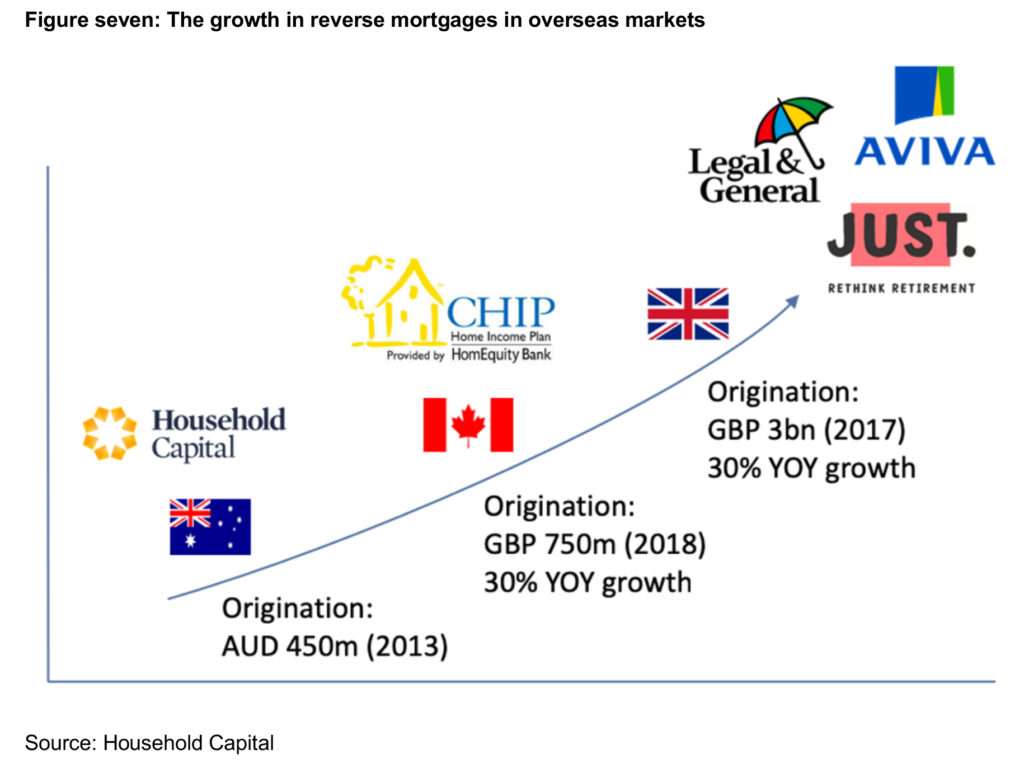

Canada and the United Kingdom have a similar demographic composition to Australia; an ageing workforce with a large baby boomer cohort entering retirement. Residential property values have improved over time in these markets and many individuals approaching retirement are asset rich, cash poor, with home equity significantly outweighing the value of retirement savings.

As illustrated in figure seven, there has been significant growth in reverse mortgages used to fund long-term retirement income streams in these markets; the reverse mortgage markets in both Canada and UK have experienced 30 percent growth, year on year. This growth rate is expected to continue as retirees continue to access the lifetime savings accumulated in their homes to supplement retirement savings and government pensions, to provide a more comfortable retirement.

The Australian experience

Traditional bank reverse mortgages were generally unaligned with the long-term housing and funding needs of Australian retirees, and therefore failed to provide genuine retirement funding adequacy and certainty. There are several reasons why traditional bank reverse mortgage products failed to meet the widespread needs of Australian retirees, including:

- Adverse selection – seen as a form of ‘last resort’ financing for many older Australians, historical access of home equity was often for inappropriate purposes for potentially distressed borrowers. These circumstances provide a recipe for dissatisfaction with the situation, the product and the provider.

- Misaligned distribution – while financial advice was often recommended, access to home equity in Australia was never directly linked to long-term retirement planning or financial advice.

- Short term consumption of equity – according to an ASIC review of reverse mortgage lending in 2018, the application process historically focused primarily on the borrower’s short-term objectives, with limited attention paid to future needs. This left many borrowers cash poor and asset depleted throughout the remainder of their lives.

- Lack of intergenerational transfers – traditional reverse mortgages failed to provide a structured mechanism to satisfy the long-term retirement income needs of a borrower and enable the responsible transfer of home equity to subsequent generations at a time they incur major lifetime expenses.

The future of home equity

Why home equity?

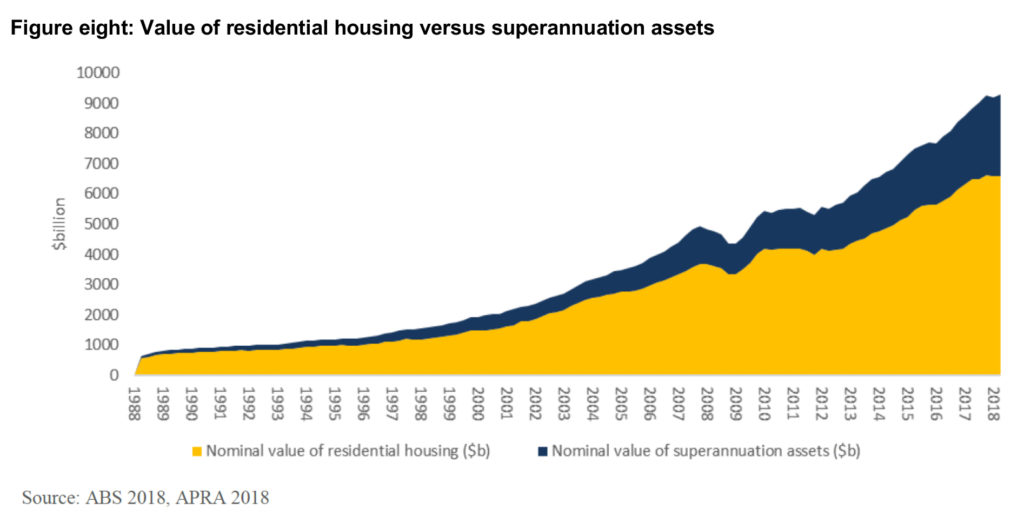

Australian retirees—individually and as a cohort—are already disproportionately exposed to residential property. Throughout the expansion of the Australian superannuation system since 1988, residential property has been a vastly larger national asset class (figure eight).

For many baby boomers at or in retirement, the majority of their lifetime savings are held in a single residential property. Indeed, residential property remains the most significant store of wealth for Australian households, despite the introduction of superannuation.

For the past 20 years – and in many cases since baby boomers bought their first homes – Australian residential property has provided strong returns with no greater volatility than other investment asset classes.

Recently, most major residential property markets have experienced a major cyclical correction, putting residential property baselines in place. New approaches for widespread access to home equity are timely – the equity of both lenders and the large cohort of baby boomers approaching retirement will be protected in the long term; as valuations increase, so will access to equity. With the family home being a major store of household wealth, now is the time for innovative, responsible and sustainable access to home equity.

Regulatory and policy environment

Retirement housing must be viewed alongside retirement income in a fluid policy environment that addresses housing, access to home equity, superannuation and longevity. The National Consumer Credit Protection Act (2012) provides the foundation for access to home equity in Australia. It stipulates clear consumer protections and market parameters at both the beginning and end of all loans. These protections include:

- Prospective loan-to value ratios (LVR): At 55 years, borrowers can obtain 15% of their home value, increasing 1% for every year of age—i.e. 25% LVR at age 65. LVRs above this are presumed to be unsuitable for the borrower.

- No negative equity guarantee: Borrowers cannot owe more than 100% of the market value of their home when it is sold. Lenders cannot claim against the borrower or estate any amount in excess of the value of the home.

- Certainty of occupancy: Australian reverse mortgages are ‘non-recourse’ – in other words, borrowers cannot be evicted or foreclosed based on longevity, property prices or the value of the loan.

- Responsible lending: Credit providers must enquire about the possible future requirements and objectives of the customer including the ability to live in the home without hardship, future aged care needs and future bequests.

- Consumer disclosures: Credit providers must give borrowers projections of future home equity concordant with the ASIC MoneySmart calculator, an information statement, occupancy protection information and provide annual statement and servicing.

- Enforcement and discharge: Loan default provisions are limited in circumstances of serious contractual breach and must be notified via direct personal communication.

Since the introduction of the National Consumer Credit Protection Act (2012), several other policy reviews have shaped opportunities to improve retirement housing and incomes. These include:

- Australian Financial System Inquiry (Murray) 2014 which recommended that the compulsory superannuation system transition to deliver comprehensive income products for retirement (CIPR). Increased total available funding for retirement by adding home equity may then be optimised by use of a CIPR to deliver more reliable, long-term retirement incomes.

- Productivity Commission: Housing Decisions of Older Australians 2015 which made the key link between policies for housing and home equity, and noted the lack of innovation and growth in the provision of home equity access in Australia.

- APRA regulatory capital 2017, from which APRA increased the capital risk-weighting of reverse mortgages from 50% to 100%, making them less profitable for banks to provide and retain on their balance sheets.

- Pension Loans Scheme 2018 (PLS), expanded to provide broader access for retirees; it enables those on a full or part Age Pension to use home equity to receive up to 150% in addition to their pension entitlements.

- ASIC Review of Reverse Mortgages 2018, which both highlighted the clear need for access to home equity and also found a dysfunctional market. Since then, the market ASIC reviewed has largely evaporated – during the course of the review and its publication, all four of the existing major bank lenders have withdrawn from the reverse mortgage market.

The overall conclusion from a review of reverse mortgage policy and legislation is that the foundations of responsible, long-term access to home equity to fund retirement are now in place to support the innovation necessary to meet the widespread needs of Australian retirees.

The fourth pillar of retirement funding

Facilitating access to home equity to fund long-term retirement needs represents an opportunity to meet a major unmet community need and provide a sustainable fiscal stimulus to enhance economic growth.

Household Capital identifies a range of responsible retirement funding needs which may be met with access to home equity. Two guiding principles govern this approach. First, long-term retirement funding needs are largely met by the transfer of home equity to appreciating assets which can meet those funding needs over time. Second, credit is constrained for short-term consumption of home equity or deployment to depreciating assets.

When it comes to home equity, innovation is required across three broad areas:

- Integration of home equity with the retirement income system

- The psychology and experience of retirees relative to their retirement incomes and their homes

- New ways to finance long-term reverse mortgages.

Home equity should form part of long-term retirement planning; it should be integrated within the Australian financial advice and superannuation sectors to make it widely available to support retirement funding.

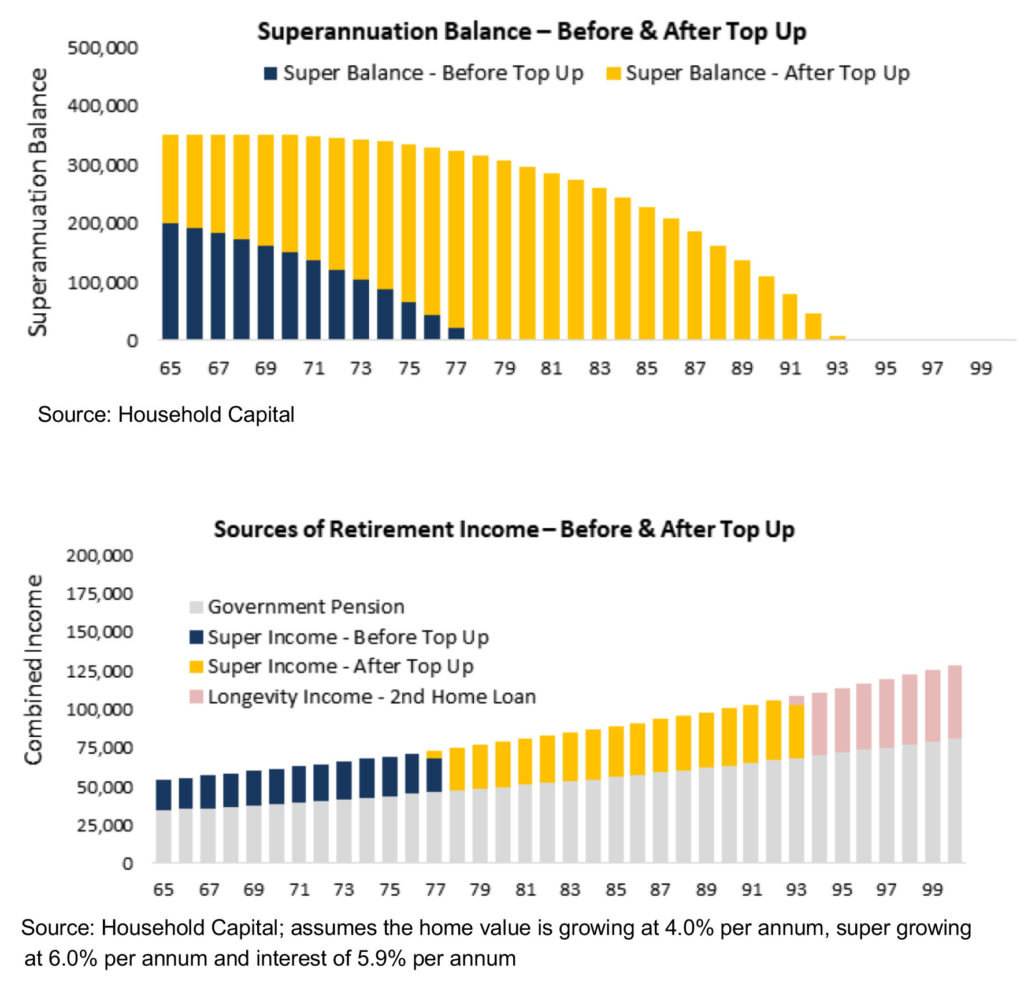

Case study one: Super top-up – transferring home equity to an accessible, appreciating

Maree and David retired at 65, with a combined superannuation balance of $200,000. Their adviser did some modelling which showed their super would provide an income of $20,000 per year, indexed at 2.5% per annum, for 13 years.

Even with their Age Pension entitlement, they’re concerned they won’t be able to have the retirement lifestyle they’d envisaged and, once their super is exhausted, will be solely reliant on the Age Pension.

Their adviser recommended using a portion of the couple’s home equity to top up their super. Maree and Lachlan used $150,000 of home equity to top up their super; this provides an income of $20,000 per annum, indexed at 2.5% per annum, for 29 years and they retain their entitlement to the Age Pension.

At the time superannuation is exhausted in 29 years, the home has 60-70% of the equity remaining, enough to draw additional funds for ongoing living expenses or to use as a bond for entering aged care.

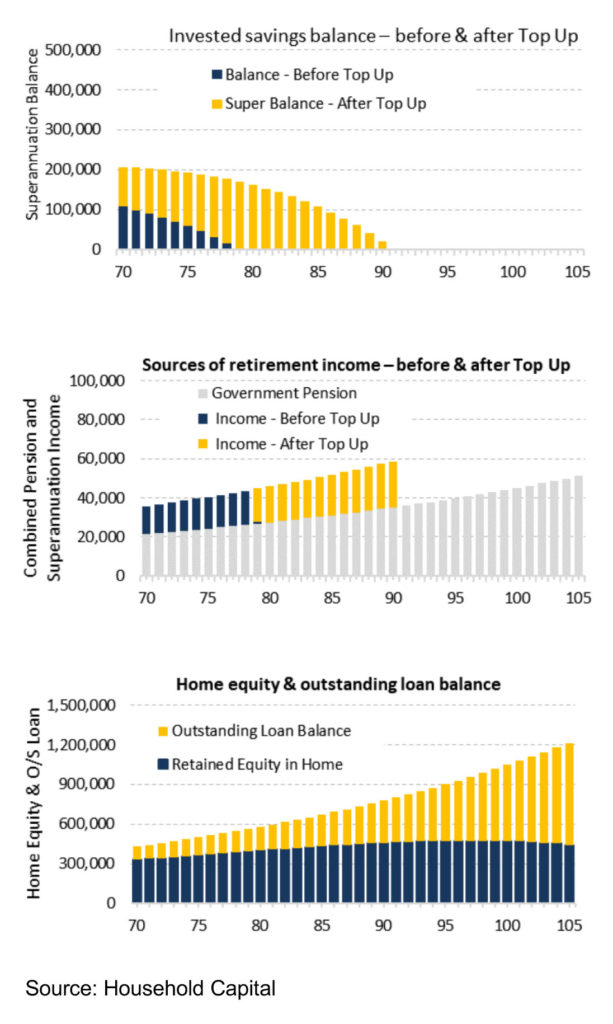

Case study two: replenish invested savings

George is 70 years old and retired some years ago. He has an income strategy that includes the Age Pension and an investment account. He has $107,000 in savings and owns his own home, which is worth $430,000. George and his adviser are concerned that his current expenditure will exhaust his savings in less than 10 years.

He is faced with the prospect of significantly curbing his spending or accessing the wealth in his home through downsizing. Neither option is palatable to him; he enjoys his lifestyle and he has no desire to leave his home or community.

As an alternative, his adviser recommends transferring a portion of his home equity, to transfer this wealth into investments to extend his income stream. By transferring $100,00 into an investment, he can extend his income of $15,000 per annum to age 90. At this time, with modest house price growth (3 percent), George still has 60 percent of his home equity remaining.

Clear benefits can be found in an approach that includes the responsible use of home equity. Existing financial services infrastructure is used. It is the most efficient way to ensure long-term planning for retirement funding. Home equity can be deployed in appreciating assets managed by the distribution partner to generate long-term retirement income.

The psychology of baby boomers, their homes and retirement is complex. Just as there is no “average” baby boomer, there is wide heterogeneity in attitudes, retirement needs and experience in using debt to both invest and consume.

By restructuring responsible access to home equity, retirees receive multiple benefits:

- Access to savings: where the majority of lifetime savings are in the home, these are now available to improve retirement funding.

- Improved retirement funding: where the Age Pension and superannuation are inadequate, home equity can improve retirement funding.

- More reliable retirement income: for some retirees, income may be volatile relative to the performance of superannuation. Home equity can smooth income and capital supply.

- Asset diversification: as superannuation is depleted, retirees’ assets become increasingly concentrated in a single residential property. Transfer to superannuation can diversify assets.

- Long term financial advice: higher super balances during retirement can qualify for long-term financial advice and the benefits that come from holistic management of household savings.

- Sequencing risk management: responsible, long-term access to home equity adds a second, independent, largely uncorrelated source of income should super assets decline periodically.

Traditionally, Australia’s retirement income policy has been framed as having three pillars: superannuation, non-superannuation savings and the age pension. However, for many Australian baby boomers these three pillars provide inadequate resources to fund longevity.

Now is the time to include the fourth, and largest, pillar of retirement funding: home equity. By drawing on multiple sources of income, Australian retirees can achieve funding adequacy throughout the full course of 25+ years of retirement. To do this, however, retirees must be able to responsibly and cost-effectively access home equity savings to generate retirement income.

By drawing on multiple sources of income, Australian retirees can achieve funding adequacy throughout the full course of their retirement. However, to achieve this, retirees must be able to responsibly and cost-effectively access home equity savings to generate retirement income.

———-