Economic perspectives

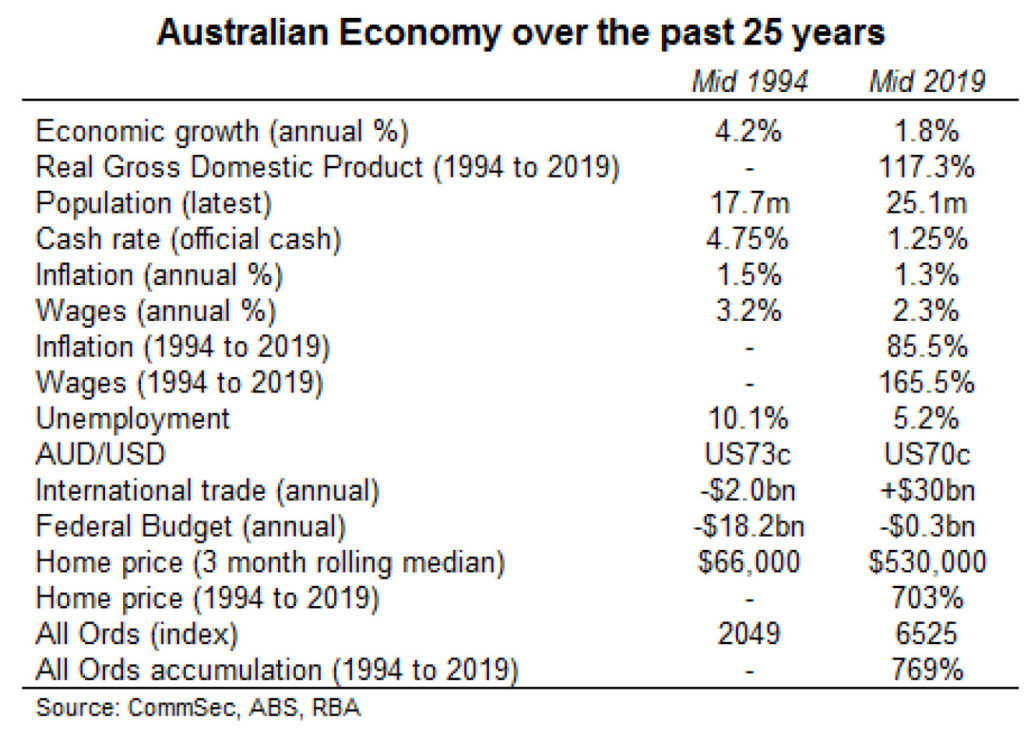

- Australia 25 years ago: Every generation believes they face tougher times than other generations. But the current economic times stack up surprisingly well compared with the past. We look back over the past 25 years.

- Recently, globalisation has caused inflation and wages to grow at far slower rates than in the past while interest rates are at record lows. The ‘new age’ may lead to slower growth of sharemarket returns.

Looking back at past economic times enables investors, businesses and consumers to get perspective when making financial decisions.

What does it all mean?

- Economies are constantly changing – just ask the Reserve Bank hierarchy. A year ago the Reserve Bank thought that the next move in interest rates would be up. But, encouraged by tame inflation, the Reserve Bank has just cut interest rates, concluding that the economy can grow faster and create more jobs.

Twenty-five years ago the situation was far different. The economy was accelerating, creating the risk of higher inflation. In August 1994 the Reserve Bank lifted the cash rate from 4.75 per cent to 5.50 per cent. By the end of the year the cash rate stood at 7.5 per cent. Inflation hit 5.1 per cent in the second half of 1995.

- While economies will always fluctuate in the short term, the more important issue is whether the standard of living is enhanced over time. Certainly the standard of living is much a much broader concept than merely focussing on changes in economic variables. But it is still an important part of the equation.

- Arguably those in their mid-40s and above – ‘Baby boomers’ and Generation X – have experienced a tremendous improvement in economic and financial circumstances over the past 25 years. Wages have soared in real terms, together with the value of assets like shares and homes. Inflation is low, unemployment is near decade lows and interest rates are the lowest since the mid-1960s. And the record economic expansion is in its 28th year.

- The improvement in economic fortunes have occurred under Labor and Coalition governments, and despite a raft of global challenges like the Asian Financial Crisis, Technology boom and bust and the Global Financial Crisis.

Higher wealth has led to changes in spending

- Arguably the extent of the improvement in economic circumstances has been almost unprecedented. Lack of consistent longer-term data prevents economists from declaring the improvement as the best ever.

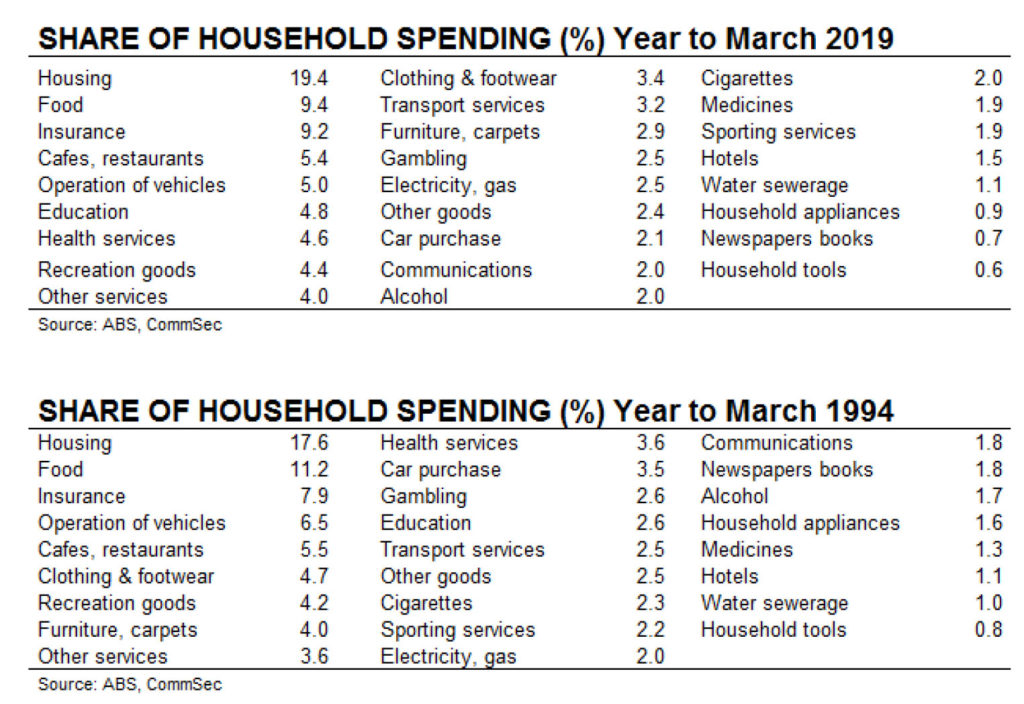

- But clearly the gains in real income and wealth have caused changes in how Aussies spend their money. Housing costs – paying the rent or the mortgage – now occupy a bigger share of household spending. Over time the relative cost (or affordability) of so-called essential items like food, clothing, cars and household goods has fallen, allowing Aussies to buy bigger and better homes.

- And importantly the rising value of homes has added to household wealth and incomes and allowed ‘Baby boomers’ and GenX to embrace more discretionary goods and services over time.

- Over the past 25 years, Aussies have increased their share of spending on housing, insurance, education, health, medicines and electricity/gas. But Aussie consumers have trimmed the share of spending devoted to food, clothing, furniture, household appliances and the purchase of cars and operation of cars.

- Lower tariffs, globalisation and technology have served to reduce the relative cost of goods such as cars, fridges, furniture and floor coverings. With extra disposable income, Aussies have chosen to upgrade homes, the schools their children attend and their elected doctors, hospitals and specialists. Higher prices have lifted the share of spending going to utilities. The ageing of the population has also lifted relative spending on health and insurance.

Income & wealth

- Over the past 25 years wages have risen by 165 per cent, well ahead of inflation, up just over 85 per cent. Over the same period, household income per capita (per person) has lifted by 181 per cent, ahead of per capita consumer spending, up 176 per cent. And wealth per capita has lifted by 326 per cent, not far from the greatest generational lift in wealth that occurred just over a year ago with a 370 per cent per capita lift in wealth.

- Over the past three years there has been a slowdown in income and wealth gains, arguably from an unsustainable pace. With globalisation serving to restrain inflation, wage growth has also eased. Consumers have drawn down on savings to adjust to the slower growth environment. On average household income grew at a 2.9 per cent annual rate over the past three years, behind a 3.9 per cent lift in spending.

- Also making it difficult for Aussie consumers, taxation has risen at a 5.7 per cent annual rate over the past three years. Tax now takes 14.7 per cent of household income – a near 13-year high – reflecting ‘bracket creep’ and tougher enforcement by tax authorities.

What are the implications for investors?

- Australia has one of the highest standard of living in the world. Income has outpaced inflation over time and wealth has soared. The lift in income and wealth have prompted many to upgrade their homes. People can afford more expensive and better quality homes because interest rates have fallen to record lows and a smaller proportion of household budgets now goes to ‘essentials’.

- Advertisements from 1994 highlight some of the gains made in affordability over time. Beer and meat are more affordable now than 25 years ago and chicken is one item that can be purchased at a cheaper price now than in 1994.

- The current generation of 20-30 year old Aussies are faced with more expensive homes but also enjoy the same smaller proportion of spending devoted to ‘essentials’ than in the past. But GenZ and Millennials also have different priorities, favouring travel, ‘experiences’ and smaller homes.

- The question being asked by many across the globe is whether we have entered a new era of lower inflation, lower interest rates and lower growth of both income and wealth. The faster that people adjust to a lower growth environment, the lower the risk of economic shock.

- Companies are having to adjust to the new realities of global competition and slower growth of sales and incomes. The risk is that some companies may over-react by cutting expenses too far (particularly wages and employment) rather than seeking to maintain or increase market share.

- Investors may also need to adjust to the new realities of slower growth of share prices and dividends. Over the past three years dividends have increased at a 1.5 per cent annual rate. From 2013-2016, annual growth of dividends averaged 3.7 per cent.