Weekly market update – week ending 26 July, 2019

Investment markets and key developments over the past week

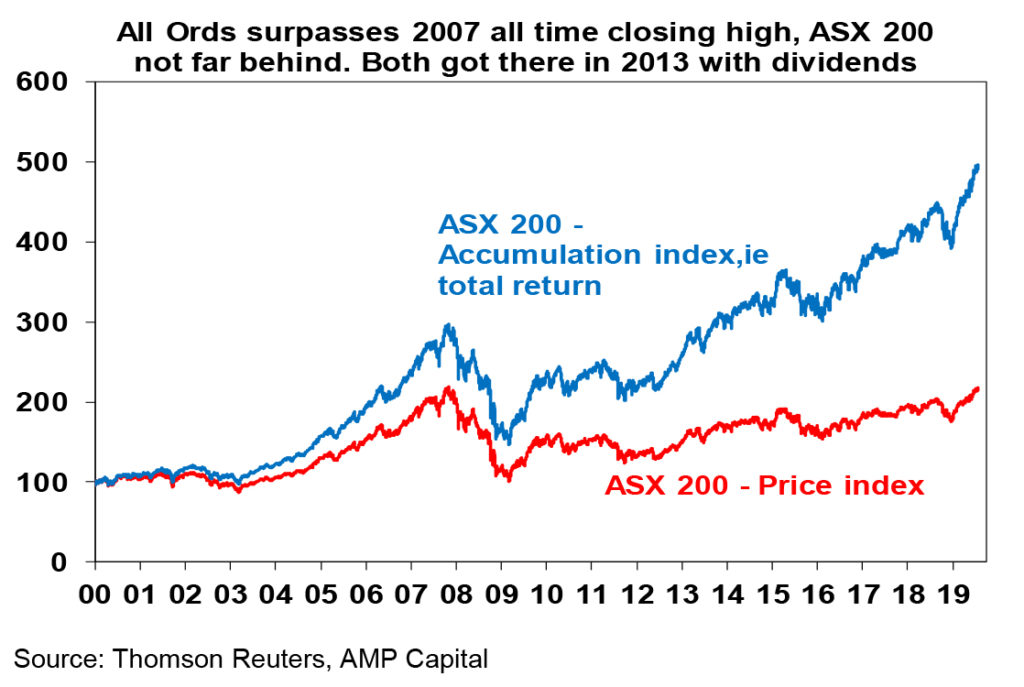

Share markets rose over the last week helped along by positive news on trade, a deal to resolve the US debt ceiling and reasonable US earnings. While Australian shares slipped on Friday, they rose through the week helped by the positive global lead with the All Ords finally surpassing its 2007 all-time high with strong gains in energy, consumer, industrial and financial shares. Bond yields fell further with the Australian ten-year bond yield falling to a new record low on RBA talk of lower for longer interest rates. While oil prices rose a bit as tensions with Iran continued, metal prices fell as did the iron ore price on the back of news that Vale will restart some production. Dovish RBA comments and a rising $US saw the $A fall.

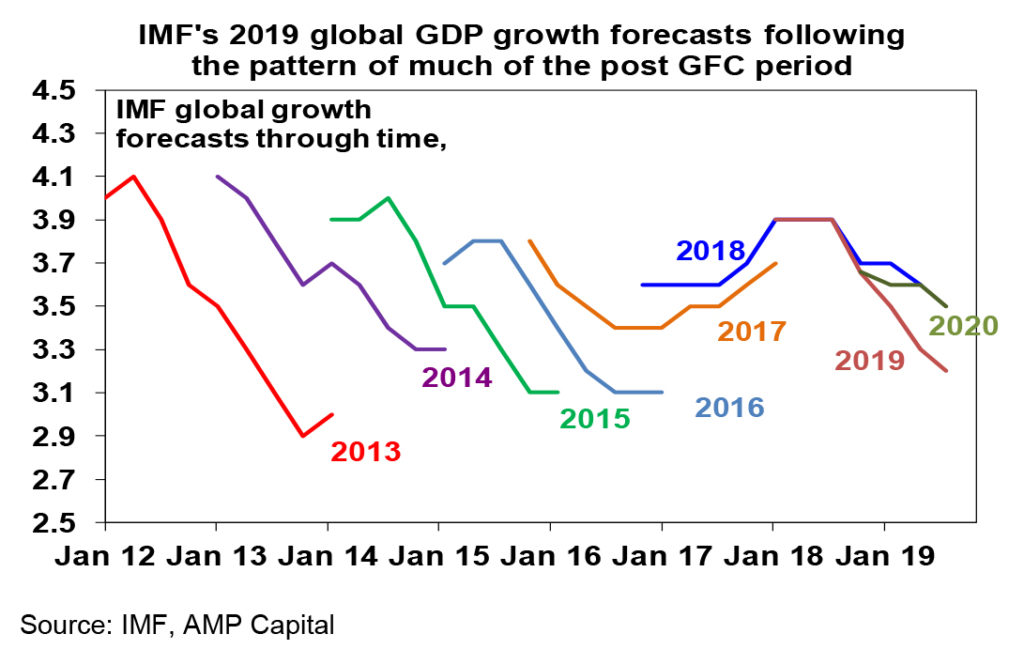

The past week saw ongoing softness in global business conditions PMIs for July and the IMF revise down its global growth forecasts again. IMF forecasts for the US were actually revised up, but due to downgrades for emerging markets the IMF revised down its global growth forecasts by 0.1% to 3.2% for 2019 & to 3.5% for 2020. However, the IMF is really just responding to the same risks that markets responded to last year, it’s following the same pattern of “initial optimism then revise down” seen for much of post GFC period and in any case 3% or so global growth is not that bad. And while global business conditions PMIs remain weak, they are still consistent with the slowdowns seen around 2012 and 2015-16 as opposed to something deeper. But they do need to bottom soon!

And on this front, there was some good news on four key fronts over the last week. First, the US/China trade talks are finally resuming with face to face meetings in China in the week ahead and both sides offering goodwill gestures (with the US loosening restrictions on Huawei and China possibly stepping up agriculture purchases from the US). This is important as Trump’s trade war has played a major role in depressing manufacturing confidence.

Second, the US debt ceiling looks to have been resolved relatively quickly (assuming the bi-partisan deal passes Congress). The weakening of the Tea Party, Trump being less concerned about debt and spending than many Democrats and no party wanting to be seen as a spoiler (after the lessons of 2011 and 2013) have made it easier this time. The key for the economy is that another debt ceiling debacle looks to have been avoided and the agreed increase in spending caps have removed a mini “fiscal cliff” that would have dragged on the economy next year. Of course, the details need to be agreed on spending to avoid another government shutdown in October.

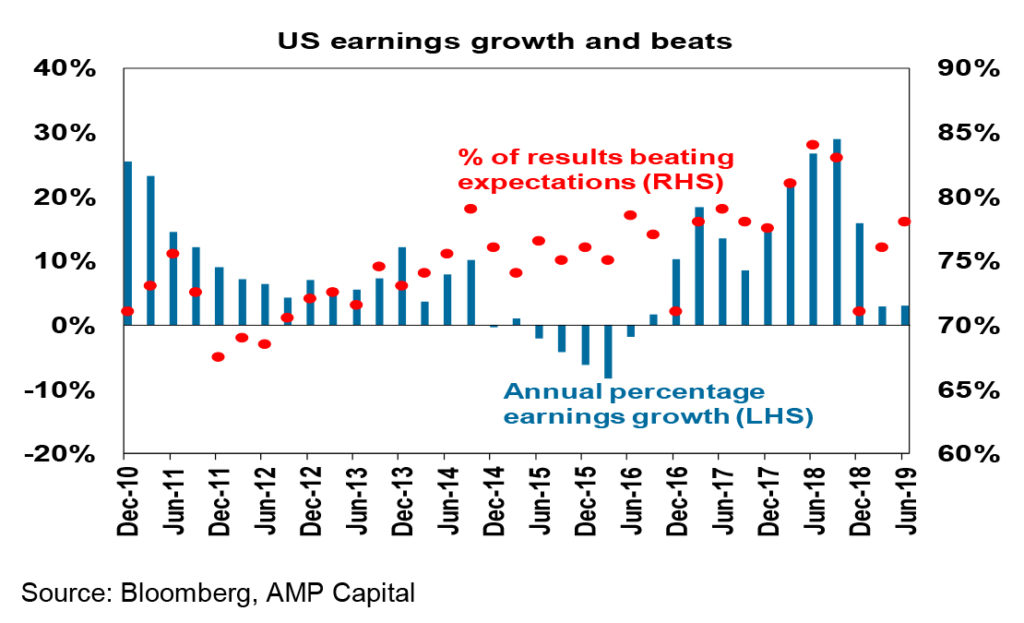

Thirdly, while earnings growth in the US has slowed, the much feared earnings recession hasn’t happened with June quarter earnings reports looking ok and earnings up around up 3% from a year ago.

Finally, the ECB formally signalled it was on track to join the global reflation effort. While ECB President Draghi’s comments lacked detail his comment that the outlook is getting “worse and worse” and the ECB’s statement that it is expecting rates “at present or lower levels” at least through to first half 2020 and that it is looking at ways to reinforce forward guidance on rates, design a tiered system for negative interest rates and options for another round of quantitative easing all leave it track for more policy stimulus in September, with a key component likely to be a new €30bn a month QE program.

Boris Johnson’s elevation to being the next UK PM was no surprise and ushers in Season 3 of the Brexit comedy. Johnson’s commitment to Brexit by October 31 with or without a free trade deal with the EU means that the risk of a no-deal Brexit has gone up as the EU is unlikely to revise the deal with former PM May much. But Parliament will likely continue to vote against a no-deal Brexit, meaning that the path is ahead is fraught for the UK with a constitutional crisis and new election and maybe (ideally) another Brexit referendum (where Britons would be better informed and could make a more useful decision). Remember that while this is a mess for the UK as roughly 46% of UK exports go to the EU and these are at risk in a no-deal Brexit, it’s only a drag for the EU as just 6% of EU exports go to the UK and it’s a side show for the global economy and markets (which ignored Johnson’s elevation).

Australian share market hits an all-time high after nearly 12 years – but can it be sustained? The All Ords index has surpassed its record 1 November 2007 closing high of 6853.6 and the ASX 200 is not far from doing the same. Basically, the Australian share market is looking through short term uncertainties around the economy and focussing on lower interest rates and bond yields making shares relatively cheap, the likelihood that policy stimulus will ultimately boost economic growth, high iron ore prices boosting mining companies and a positive global lead. While US shares made it back to their 2007 high in 2013 and global shares did so in 2014, Australian shares took longer because of much tighter monetary policy after the GFC, the high $A until recent years, the collapse in commodity prices and the fact that the 2007 high was a much higher high for Australian shares than it was for global shares thanks to the resources boom last decade. Of course, once dividends are allowed for, the Australian share market surpassed its 2007 record high in 2013.

Is it sustainable? Going through past bull market highs after a long period below can attract investors into the market so it could push on for a bit. But after such a huge run – the market is now up 20% year to date – its vulnerable to a short-term correction and the August earnings reporting season may result in some volatility. However, the combination of low bond yields which means that the share market is comparatively cheap, monetary easing by the RBA and other central banks and a likely pick up in global growth by year end and Australian growth next year point to even higher share prices on a six to 12 month horizon.

Major global economic events and implications

US economic data was a bit mixed with PMIs showing stronger services sector conditions but weaker manufacturing, a fall in existing home sales but stronger new home sales, rising underlying durable goods orders but soft house price growth. About 40% of US S&P 500 companies have reported June quarter results and they remain reasonably good with 78% beating on earnings, 59% beating on sales and earnings growth for the quarter looking like it will come in at around +3%yoy, which is up from expectations for a small fall a few weeks ago. Of course, this is well down from 27% earnings growth a year ago because growth has slowed and the tax cut boost has fallen out. But its not an earnings recession.

Eurozone business conditions PMIs fell in July as did the German IFO index and while bank lending continues to trend higher its only gradual all of which is consistent with the ECB moving towards further monetary easing.

Fortunately, Japan’s business conditions PMIs rose in July.

Australian economic events and implications

Australia data was softish with the CBA’s business conditions PMIs slipping in July and skilled job vacancies falling for the sixth month in a row in June pointing to softer jobs growth ahead. Meanwhile RBA Governor Lowe confirmed the RBA’s commitment to the 2-3% inflation target to be achieved “on average, over time”, reiterated the RBA’s easing bias and basically said a rate hike was a long way away and won’t be contemplated until the RBA is confident inflation is returning to “around the mid-point of the target range” (which is pretty strong forward guidance). Lowering the inflation target to say “1 point something” as some advocate makes no more sense than the calls to raise it to “4 point something” did just over a decade ago: changing the goal posts would weaken the credibility of inflation targeting, it would lock in permanently lower wages growth which is not good for wellbeing, it would reduce the room to cut interest rates as we would always be nearer the “zero bound” on interest rates and it would risk a slide into debilitating deflation each time there is a severe economic downturn. Our view remains that policy stimulus to date will help but won’t be sufficient to push unemployment below 4.5% as the RBA would like and so further monetary easing is likely after a brief pause with a cut to 0.75% in November and a cut to 0.5% in February next year likely.

What to watch over the next week?

The next round of US/China trade negotiations in China and US/Iran tensions are important for markets in the week ahead. All eyes will also be on the Fed which is expected to cut interest rates by 0.25% taking the Fed Funds rate range to 2-2.25%. This will be the Fed’s first rate cut since December 2008 and follows nine 0.25% rate hikes between December 2015 and December last year. With underlying growth still solid and the jobs market tight this should be seen as the Fed taking out some insurance given various threats to growth including from the US/China trade war, tensions with Iran and slower global growth generally and a greater willingness by the Fed to take risks with higher inflation as opposed to deflation. Given that the Fed is taking out insurance rather than responding to a crisis a 0.25% cut is more likely than a 0.5% easing, but we expect it to signal that further easing is likely. So, we expect another 0.25% cut to come in September.

On the data front in the US, expect July jobs data on Friday to show a 160,000 rise in payrolls, unemployment falling back to 3.6% and wages growth edging back up to 3.2% year on year. In terms of other data expect to see solid growth in June personal spending, a rise in core private consumption deflator inflation to 1.7% year on year from 1.6%, a rise in consumer confidence and stronger pending home sales (all due Tuesday), June quarter employment cost growth (Wednesday) to edge up slightly to 2.9%yoy, the July manufacturing conditions ISM (Thursday) to rise to 52 and the trade deficit (Friday) to fall slightly. The US June quarter earnings reporting season will also continue.

Eurozone June quarter GDP growth due Wednesday is likely to have come in at around 0.2% quarter on quarter with annual growth at 1%yoy. Meanwhile, expect economic confidence (Tuesday) to soften a bit, unemployment to have remained at 7.5% in June and core CPI inflation (both Wednesday) to fall back to around 1%yoy.

The Bank of England (Thursday) is expected to leave monetary policy unchanged.

The Bank of Japan (Tuesday) is also expected to leave its ultra easy monetary policy unchanged. Meanwhile on the same day expect June labour market data to remain strong and industrial production to fall slightly.

Chinese PMIs for July to be released on Wednesday and Thursday are expected to show basically stable business conditions.

In Australia, the focus in the week ahead will be back to inflation with June quarter CPI data on Wednesday likely to show that inflation remains soft. A 10% rise in petrol prices is likely to drive a rebound in headline inflation to 0.5% quarter on quarter and 1.5% year on year. But underlying inflation is likely to remain subdued at 0.4%qoq or 1.4%yoy reflecting weak consumer demand, ongoing spare capacity and intense competition. In other data expect a further fall in dwelling approvals (Tuesday), continuing modest credit growth (Wednesday), a 0.1% rise in July CoreLogic house prices (Thursday) and a 0.3% rise in June retail sales (Friday) with June quarter real retail sales up 0.3%. June half earnings reports will start to flow but with only a couple of major companies reporting of which RIO (Thursday) is likely to see a strong result due to the high iron ore price. Consensus expectations are for low single digit growth mainly due to resources.

Outlook for investment markets

Share markets remain vulnerable to short term volatility and weakness on the back of uncertainty about trade, Middle East tensions and mixed economic data. But valuations are okay – particularly against low bond yields, global growth indicators are expected to improve and monetary and fiscal policy are becoming more supportive all of which should support decent gains for share markets over the next 6-12 months.

Low yields are likely to see low returns from bonds, but government bonds remain excellent portfolio diversifiers.

Unlisted commercial property and infrastructure are likely to see reasonable returns. Although retail property is weak, lower for longer bond yields will help underpin unlisted asset valuations.

The combination of the removal of uncertainty around negative gearing and the capital gains tax discount, rate cuts, support for first home buyers via the First Home Loan Deposit Scheme and the removal of the 7% mortgage rate test suggests national average capital city house prices are at or close to bottoming. Next year is likely to see broadly flat prices as lending standards remain tight, the supply of units continues to impact and rising unemployment acts as a constraint.

Cash and bank deposits are likely to provide poor returns as the RBA cuts the official cash rate to 0.5% by early next year.

The $A is likely to fall further to around $US0.65 this year as the RBA moves to cut rates by more than the Fed does. Excessive $A short positions, high iron ore prices and Fed easing will help provide some support though with occasional bounces and will likely prevent an $A crash.

By Shane Oliver