Investment markets and key developments over the past week

Share market rose solidly over the last week buoyed by a bunch of good news including the latest US/China trade war truce, the nomination of Christine Lagarde to head the ECB after Draghi and, in Australia, another rate cut and Parliamentary support for tax cuts. Bond yields continued to fall though on the back of soft economic data with Italian bond yields plunging as the dispute in Europe about Italy’s budget deficit receded for now. Commodity prices were mixed with oil and metals down but gold and iron ore up. The $A rose marginally despite a rise in the US dollar.

Shares up, bond yields down – which market is right? Maybe they both are. This occasionally happens around the “sweet spot” in the investment cycle. Basically, shares having fallen last year on growth fears are looking through short term growth uncertainties and focussing on lower for longer interest rates and bond yields making shares relatively cheaper and the likelihood that monetary and fiscal stimulus will ultimately boost economic growth. By contrast bonds are focussed on falling inflation and lower for longer short-term interest rates. So, there is logic behind both shares and bonds rallying at the same time.

The latest trade war truce between the US and China is good news, but it’s the minimum necessary to keep markets happy. Existing tariff hikes remain in place and uncertainty remains about future hikes. The uncertainty about what all this means for supply chains and investment has weighed heavily on business confidence and needs to be resolved quickly to avoid further damage and keep markets on side. The good news is that the economic damage and Trump’s desire to get re-elected next year (which he won’t be if the economic damage continues) provides a strong incentive to resolve the issue. So our base case remains that there will be a deal. But the risk is significant that it will end in failure again.

The nomination by EU leaders of Christine Lagarde to head the ECB (subject to majority EU parliament support) is good news. Lagarde is dovish and will likely continue the “whatever it takes” approach of Mario Draghi. It’s a negative for the Euro but positive for Eurozone growth and shares.

Good news in Australia too with another rate cut and tax cuts confirmed by Parliament. But will the rate cuts work and is it all going to be enough? The RBA remains upbeat on growth but cites a desire to see lower unemployment and underemployment. While it doesn’t admit it, the downturn in growth over the last year and emerging signs of an uptrend in unemployment have likely played a big role in its decision to cut rates. Rate cuts may not provide the same boost they did in times past, but this is not because they are low but rather because household debt ratios are much higher and Australians won’t be rushing out to take on even more debt and the banks are less inclined to provide it. But rate cuts will still help.

- First, they will help households with debt. They are not good for those relying on income from bank deposits but the total value of household debt at around $2.5 trillion swamps the total value of household bank deposits at around $1.1trn so for example a 0.2% reduction in mortgage rates and bank deposits (allowing for fixed rates, some banks not passing on the full cut and some deposit rates already at zero) would imply a net $2.8bn benefit to Australian households. And households with a mortgage have a much greater marginal propensity to consume changes in their “disposable” income than self-funded retirees.

- Second, rate cuts will mean a lower than otherwise Australian dollar and this in turn helps our exporters and companies that have to compete internationally. Yeah sure other countries may want lower currencies too – but that just reinforces the case to ease because if we weren’t easing it would mean a higher Australian dollar.

- Finally, rate cuts encourage investors to seek out higher returning assets than bank deposits. This boosts the share market and other growth assets which has a positive wealth effect on spending and makes more capital available for “risky” activities like investing and starting new businesses.

What sort of boost will the Australian Government’s tax cuts provide? Stages 2 and 3 of the tax cuts don’t kick off into 2022 and 2024 so are a bit academic in the short term but do at least provide confidence that bracket creep will be returned and that income tax payments will not continue to grow more quickly than household income. However, the stage 1 payment of a $1080 tax refund to those earning between $48,000 and $90,000 will be a welcome relief and the total $7.5bn payment being around 0.6% of household disposable income is equivalent to around two RBA rate cuts. Based on the GFC “stimulus payments” some of it will be spent and this will help consumer spending in the next few months with a spike likely in retail sales around September/October. However, the $7.5bn boost to households is much smaller than the $19bn in GFC stimulus payments (in fact it’s around one quarter the size in real terms) and is likely to only add around 0.2% to GDP over a year.

Overall, we are off the view that while the RBA’s rate cuts so far and this year’s tax cuts will help, they won’t be enough to get growth up to RBA forecasts for 2.75% this year and so unemployment will more likely drift up from here as opposed to fall as the RBA wants. More fiscal stimulus is likely to be required and this will be made possible by stronger than expected tax revenue on the back of the surging iron ore price and the government is talking about structural reforms to make it easier for business to invest and employ but this will take time to formulate and impact. So, it will fall back to the RBA in the short term and so after a pause we remain of the view that the RBA will cut to 0.75% in November and to 0.5% in February. After which it will call it quits on rate cuts and if necessary, look to some form of quantitative easing. Our base case though is that this won’t be necessary as ultimately the combination of rate cuts, fiscal stimulus, the lower $A, infrastructure spending, stronger mining investment and hopefully continuing solid export demand will see Australia avoid recession and growth pick up again sometime next year.

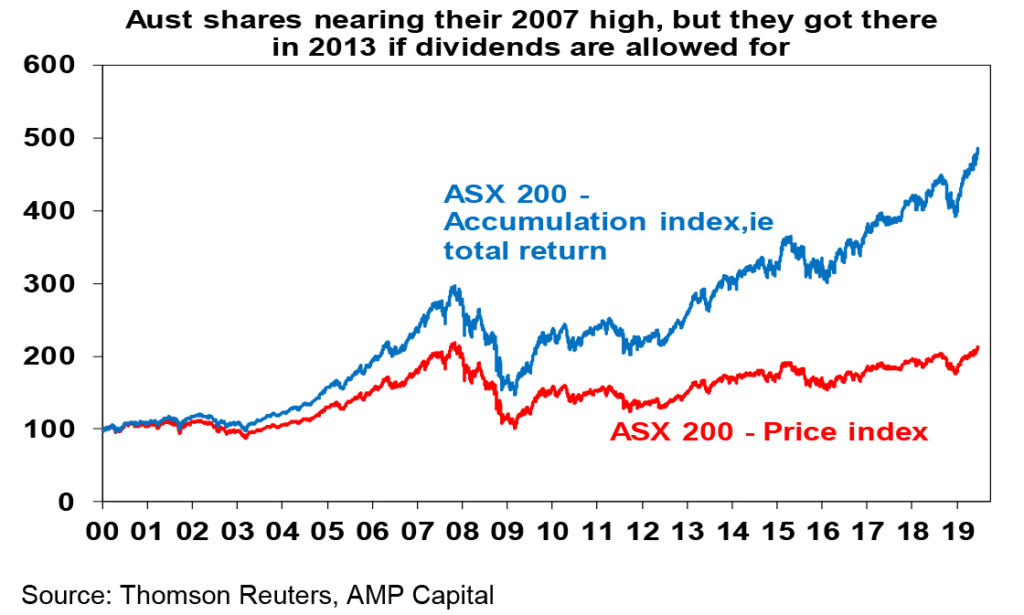

Meanwhile, the Australian share market as measured by the All Ords index is now just 0.3% below its resources boom high reached on 1 November 2007. Basically, the share market is looking through short term uncertainties around the economy and focussing on lower interest rates and bond yields making shares relatively cheaper and the likelihood that monetary and fiscal stimulus will ultimately boost economic growth. While US shares made it back to their 2007 high in 2013, Australian shares took longer because of much tighter monetary policy after the GFC, the high $A until recent years, the collapse in commodity prices and the fact that the 2007 high was a much higher high for Australian shares than it was for global shares. Of course, once dividends are allowed for, as they should be given the higher dividend yields paid by Australian companies, the Australian share market surpassed its 2007 record high, way back in 2013.

Will Australian shares keep going once the 2007 high is surpassed? Going through past bull market highs after a long period below can attract investors into the market so it could push on for a bit. But after such a huge run – the market is up 19% year to date – it is getting vulnerable to a short-term correction. However, looking beyond the short term, the combination of low bond yields, easing central banks and a likely pick up in global growth in the second half and Australian growth next year point to even higher share prices on a 6-12 month horizon.

Major global economic events and implications

US economic data was messy. While the Markit business conditions PMIs were revised to show a slight rise in June they remain soft and the widely followed ISM business conditions indexes fell. Construction data fell in May, the trade deficit widened and jobs data was mixed.

Final Eurozone business conditions PMIs for June confirmed the stabilisation/mild rising trend that’s been in place this year, credit growth continues albeit at a modest 2.7% year on year and unemployment continued to edge down to 7.5%.

The Japanese Tankan survey of business conditions generally showed a further slowing and a softening in plans for growth in business investment.

Chinese business conditions were mixed with the official PMIs little changed but the Caixin PMIs down – but all seem to be just bouncing around in recent ranges without any clear signal.

Australian economic events and implications

Australian data was a mixed bag. Building approvals are continuing to trend down and point to ongoing weakness in housing construction, retail sales and car sales remain weak and point to a soft June quarter for consumer spending and now falling job vacancies are in line with other labour market indicators in warning of rising unemployment. Against this house price data for June adds to other indicators in suggesting they are at or close to the bottom and a new record trade surplus for May points to a positive contribution to growth from trade and to national income. Finally, the Melbourne Institute’s Inflation Gauge was weak in June and points to ongoing weak inflation. All of which suggests that growth is weak but not negative and inflation remains weak consistent with expectations for further RBA rate cuts later this year.

What to watch over the next week?

In the US, expect small business optimism to remain high and job openings to remain strong (both due Tuesday) and core CPI inflation for June (Thursday) to remain around 2% year on year. The minutes from the Fed’s last meeting and Fed Chair Powell’s Congressional testimony (both Wednesday) are likely to affirm a clear easing bias.

Chinese data for June is expected to show headline CPI inflation (Wednesday) remaining around 2.7% year on year but core inflation remaining weak. Trade data (Friday) is expected to see falls in both exports and imports. Credit data is also likely to be released.

In Australia, expect the NAB business survey (Tuesday) to show a fall in business confidence and continuing weak business conditions, consumer confidence (Wednesday) to remain subdued and housing finance commitments (Thursday) for May to show a bounce.

Outlook for investment markets

Share markets remain vulnerable to short term volatility and weakness on the back of uncertainty about trade, Middle East tensions and mixed economic data. But valuations are okay – particularly against low bond yields, global growth indicators are expected to improve into the second half if the trade issue is resolved and monetary and fiscal policy is likely to become more supportive all of which should support decent gains for share markets over the next 6-12 months.

Low yields are likely to see low returns from bonds, but government bonds remain excellent portfolio diversifiers.

Unlisted commercial property and infrastructure are likely to see reasonable returns. Although retail property is weak, lower for longer bond yields will help underpin unlisted asset valuations.

National average capital city house prices remain under pressure from tight credit, record supply and reduced foreign demand. However, the combination of rate cuts, support for first home buyers via the First Home Loan Deposit Scheme, the removal of the 7% mortgage rate test and the removal of the threat to negative gearing and the capital gains tax discount point to house prices bottoming out by year end. Next year is likely to see broadly flat prices as rising unemployment acts as a constraint.

Cash and bank deposits are likely to provide poor returns as the RBA cuts the official cash rate to 0.5% by early next year.

The $A is likely to fall further to around $US0.65 this year as the RBA moves to cut rates by more than the Fed does. Excessive $A short positions, high iron ore prices and Fed easing will help provide some support though with occasional bounces and will likely prevent an $A crash.

By Shane Oliver