The U.S. Federal Reserve (Fed) has cut its policy rate for the first time in more than a decade, marking just the fourth time over the past 20 years that the Fed has pivoted from raising to lowering rates.

Boston – based Craig P. Russ, Co-Director of Floating-Rate Loans and Christopher Remington, Institutional Portfolio Manager at Eaton Vance say: “As the corporate loan market in which we invest “floats” – meaning that loan coupons adjust with short-term rates, which are driven in no small part by Fed policymaking – there’s a perception that Fed cuts would be negative for this important asset class. But we believe that stigma is misplaced.

“Let’s turn to the facts. The cut appears to be a pre-emptive “insurance” policy to stave off potential slowing for an economy on decidedly solid footing but facing some growing risks, such as ongoing trade uncertainty and cooling business investment. Given that rates are already very low, the Fed could be saving its “bullets,” maintaining room to cut down the road should economic conditions take an actual turn for the worse.

“If the senior loan asset class has been relegated to a place where it only makes sense for investors when rates are rising, we believe investors should consider rethinking that position. Loans have a place in portfolios through time, over all periods – even when short-term rates are falling.”

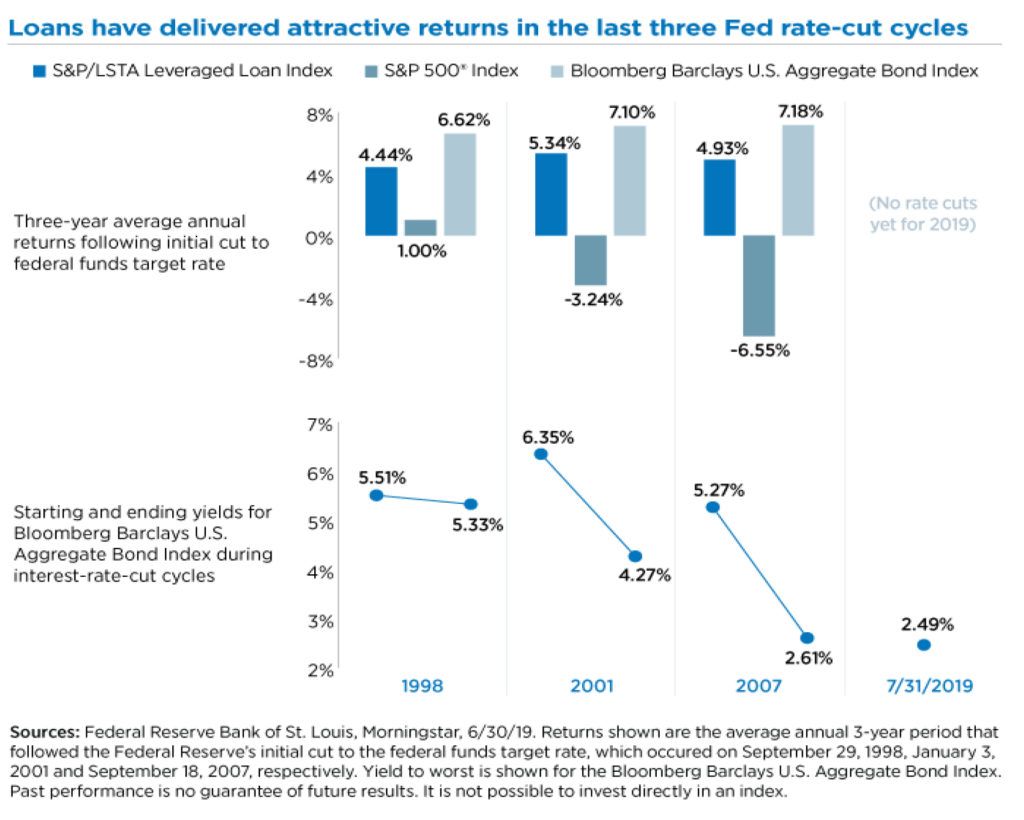

They add: Whatever the future path of short-term rates, it can be instructive to look at how floating-rate corporate loans have performed during the three Fed rate-cut cycles since the inception of the loan market’s S&P/LSTA Leveraged Loan Index in 1997. Never has the Fed cut rates just once and stopped, though each cycle has varied in its own way. Prolonged and deep cuts were made as serious recession risks unfolded in 2001 and 2007, while modest and short-lived adjustments were made in 1998 (as in 1995, before the inception of the loan index).

Because the cycle of Fed easing and tightening often takes a year or two to play out, we assess the three-year forward period measured from the time of the Fed’s initial rate cut. The exhibit compares the annualized returns of loans with those of stocks and bonds – proxied by the S&P 500 Index for stocks and the Bloomberg Barclays U.S. Aggregate Bond Index for bonds. The three-year period helps to eliminate noise and capture a more complete picture of the relative investor experience across these asset classes through the cycle.

Key points from recent rate cycles

- In the U.S. loans have consistently outperformed equities, as the economic contractions the Fed cuts were aimed at easing weighed on stock market returns, whereas the senior/secured character of loans and their income-oriented performance skew provided key ballast.

- Bonds were the clear winner, but we should consider this within the context of the decades-long “bull run” for fixed income, with long-term rates falling across all three periods. Given the flatness of today’s yield curve and a low starting yield of just 2% or so across all maturities, our view is that today’s bond math simply cannot deliver the returns of the past.

- Including an allocation to loans could have improved the experience of a typical 60% stocks/40% bonds investor in both absolute and risk-adjusted return terms. Loans have exhibited a fraction of equity volatility through time, blending well with stocks, while their floating coupon structure pairs well with the embedded duration in fixed income.

General observations about floating-rate loans

- Rate cuts are “credit positive.” The flip side of lower yields for investors is lower coupon payments for borrowers. With interest coverage in the loan market already at or near all-time highs, monetary easing makes the debt even easier to service. More broadly, cuts tend to be stimulative for the economy, which is good for corporate profitability, and supportive of capital market asset prices.

- Starting yield is one of the most reliable pre-determinants of future returns. A typical loan fund yields +/- 5% today1, while bond yields in much of the developed world are negative or close to zero. Loan yields are close to parity with high-yield bonds – by definition a riskier market – and loans actually out-yield US dollar-denominated emerging market sovereigns and corporates.

- Retail loan fund investors in U.S. now command less than 10% of loan market assets outstanding (down from a high of almost 25% in early 2014) – consolidated to a more organic, core base of holders after nine months of redemptions while loans produced solid returns. In the U.S, institutions from pension funds to insurance companies now account for more than 90% of the loan investor base because they continue to find the yield and risk/return characteristics of this asset class worthy.