Weekly market update – week ending 20 September, 2019

Investment markets and key developments over the past week

After several weeks of gains share markets were mixed over the last week as the attack on Saudi Arabian oil production provided a reminder of risks in the Middle East, global economic data was mixed and the Fed cut rates again. US and Eurozone shares were little changed, Japanese shares rose and Chinese shares fell not being helped by weak economic data. Australian shares saw good gains led by energy shares on the back of higher oil prices, taking the market back to just 1% below the all-time high seen in July. Bond yields mostly fell as the Saudi attack provided a reminder that the risks to the outlook remain significant. Oil prices rose but reversed much of the spike seen in early in the week. Metal and iron ore prices fell. The $A fell back below $US0.78 on the back of dovish RBA minutes and rising unemployment.

Rising unemployment and dovish RBA minutes point to an October rate cut. We were already expecting the next cut to come in October but two developments over the last week have seen the money market move the probability of a cut up from 22% a week ago to 84% now. First, the minutes from the last RBA board meeting were more dovish in dropping the requirement for an “accumulation of evidence” before another easing and noting that its liaison program showed that retailers are yet to benefit from the tax cuts and that the uptrend in wages growth looks to have stalled. Secondly, and more importantly, while jobs growth in August was strong the quality was poor with falling full time jobs and both unemployment and underemployment rose further which makes it very hard to see a pick-up in wages growth anytime soon. In fact, job vacancies and hiring plans point to slowing jobs growth ahead and hence even higher unemployment. All of which will be impossible for the RBA to ignore. As a result, we continue to see the next 0.25% cut coming in October followed by another cut in November, ultimately taking the cash rate down to 0.5%. Interestingly RBA Governor Lowe is scheduled to speak at a community dinner after October’s board meeting just as he did after the June and July meetings when rates were cut!

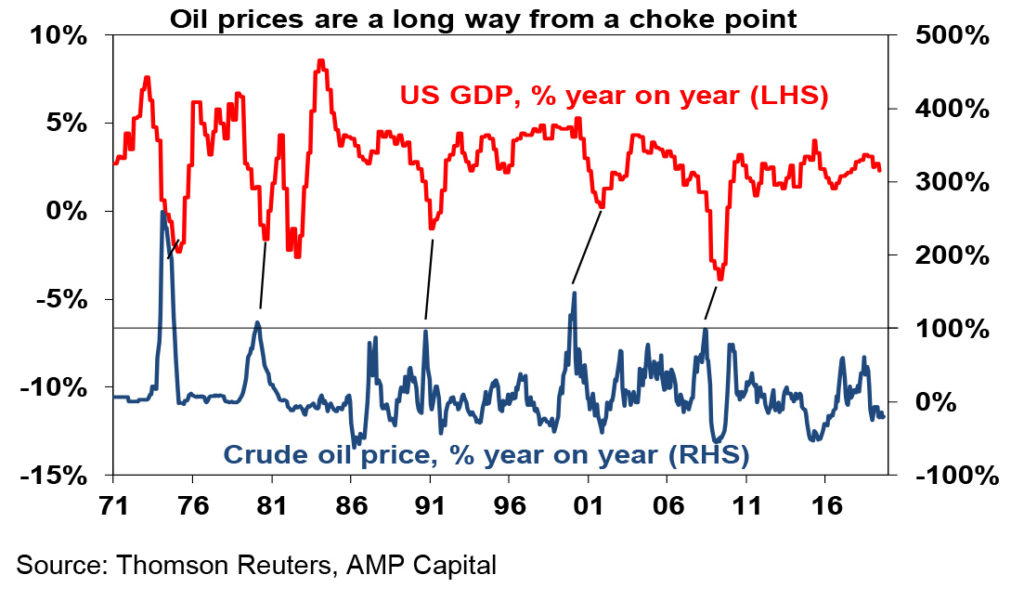

Oil was a big issue over the last week, but it quickly faded (at least for now). While oil prices spiked on news of the attack on Saudi Arabian oil production which impacted 6% of world oil supply they have settled back to be only up $3-4 a barrel from their pre attack levels as Saudi production looks to be returning to normal relatively quickly. To be a major problem for global and Australian economic growth, past experience suggests oil prices need to at least double. Right now, we are nowhere near that with oil prices down from year ago levels. See the next chart. Key to watch now will be whether there are more attacks and whether Saudi/US retaliation further escalates the conflict. Trump’s backdown from “locked and loaded” to “I don’t want war with anybody…we have a lot of options” is a positive sign. But there is a long way to go before this issue is resolved. For Australia, a doubling in world oil prices would take the average petrol price to around $1.95 a litre and that would knock nearly $20 a week off average household spending power and be a problem for the economy. But we are a long way from that. In fact, the $US3-4 a barrel rise in world oil prices over the last week would only justify a 3-4 cent a litre rise in petrol prices and then only with a lag as the more expensive fuel flows through. Average capital city petrol prices are up about a 1-2 cents from a week ago which just looks like noise.

Fed cuts rates by another 0.25%, more cuts likely. While the Fed remains optimistic its latest cut continues to take out insurance against the threat posed by the trade war and slower global growth to the US economy at time when inflation remains low. Given that the risk to the outlook – from trade and Iran tensions – won’t dissipate quickly we continue to see another Fed rate cut by year end. Meanwhile, Fed Chair Powell ruled out taking US rates negative should interest rates have to go back to zero. So, forget about negative rates in the US at least for the foreseeable future. The same likely applies in Australia.

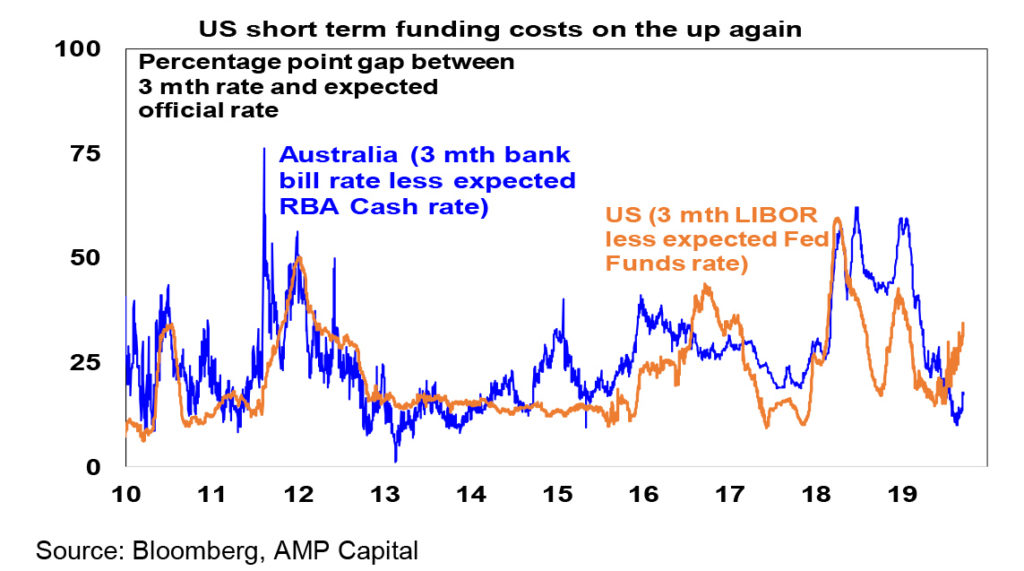

Liquidity stresses in the US money market unlikely to be a major problem. There has been a lot of talk about this over the last week, following spikes in the so-called repo rate. It likely reflects a combination of corporate tax payments, the bigger US budget deficit and the impact of quantitative tightening which has reduced bank reserves as opposed to the sort of counterparty confidence problems that caused big problems in the GFC. So Fed Chair Powell is probably right in saying “we are not worried” as the Fed addresses the problem by injecting funds into the money market (via repurchase agreements) and it looks at a longer term solution by allowing its balance sheet to grow (by injecting funds into the economy and buying bonds) over time to allow for growth in the economy. This is not really QE and is much smaller – but some might call it that. So far there is little evidence that the latest rise in US funding costs is having much impact in Australia – the gap between 3-month bank bill rates and the expected official cash rate has increased but is below normal levels.

Major global economic events and implications

US data was actually pretty good. While the leading index was flat in August and manufacturing conditions were soft in the New York region, they were solid in the Philadelphia Fed survey, industrial production rose strongly in August, existing home sales are rising, builder conditions are strong and housing starts rose to their highest since 2007 in August suggesting that the housing recovery is back on track.

The Bank of England left monetary policy unchanged but was dovish, with a lot riding on which way Brexit goes.

Similarly, the Bank of Japan made no changes to monetary policy but looks to be setting itself up for an easing next month after flagging increasing concern that it may lose momentum towards achieving its 2% inflation target. Core inflation remained weak at just 0.6%yoy August.

Chinese retail sales, industrial production and investment all surprisingly slowed in August. The slowdown likely reflects a combination of domestic factors flowing from the credit tightening a while back and the trade war. All of which suggests increasing pressure on China to de-escalate the trade war and to provide more policy stimulus – with another minor interest rate cut in the last week.

Australian economic events and implications

News that the Federal Budget was near balance last financial year – with help from underspending on the NDIS, stronger than expected employment and a higher iron ore price – while not surprising is good news in that it confirms that the starting point for this year’s budget is a bit stronger than previously projected providing some scope for providing additional fiscal stimulus while at the same time continuing progress towards a surplus. That said, the NDIS underspend is unlikely to be sustained, employment growth is likely to slow and iron ore prices have started to fall, so taken together with some likely fiscal easing the news on the budget won’t be all smooth sailing going forward.

Continuing population growth of 1.6% over the year to the March quarter indicates that population growth is an ongoing source of demand in Australia which helps economic growth and helps guard against a conventional recession. That said, its per capita growth that ultimately counts and its been negative lately so getting per capita growth and hence productivity growth back up is critical.

What to watch over the next week?

Business conditions PMIs for September to be released on Monday in major countries will likely be the main focus in the week ahead given that there has been some sign of a stabilisation in recent months.

US business conditions PMIs (Monday) are likely to show some improvement at the composite level, but with services up and manufacturing down slightly. In other data expect to see continued modest growth in house prices and a slight fall in consumer confidence (Tuesday), gains in new and pending homes sales (Wednesday and Thursday) and a modest rise in underlying durable goods orders, solid personal spending and a slight lift in core personal consumption deflator inflation to 1.8% year on year for August (all due Friday).

Eurozone business conditions PMIs (Monday) will be watched for continuing signs of stabilisation.

In Australia, a speech by the RBA’s Lowe on Tuesday titled “An Economic Update” may provide clues regarding an imminent rate cut. Job vacancies data will also be released.

Outlook for investment markets

Share markets remain at risk of volatility in the months ahead given unresolved issues around trade and Iran and mixed economic data as we are still in a seasonally weak part of the year for shares. But valuations are okay – particularly against still low bond yields, global growth indicators are expected to improve by next year and monetary and fiscal policy are becoming more supportive all of which should support decent gains for share markets on a 6-12 month horizon.

Low yields are likely to see low returns from bonds once their yields bottom out, but government bonds remain excellent portfolio diversifiers.

Unlisted commercial property and infrastructure are likely to see reasonable returns. Although retail property is weak, lower for longer bond yields will help underpin unlisted asset valuations.

The election outcome, rate cuts, tax cuts and the removal of the 7% mortgage rate test are leading to a rise in national average capital city home prices driven by Sydney and Melbourne. But beyond an initial bounce, home price gains are likely to be constrained through next year as lending standards remain tight, the record supply of units continues to impact and rising unemployment acts as a constraint.

Cash and bank deposits are likely to provide poor returns as the RBA cuts the official cash rate to 0.5% by early next year.

The $A is likely to fall further to around $US0.65 as the RBA cuts rates further. Excessive $A short positions, still high iron ore prices and Fed easing will provide some support though with occasional bounces and will likely prevent an $A crash.

By Shane Oliver