Members of superannuation funds should be comparing more than pre-tax fund performance and looking at total after-tax returns.

Data from the Productivity Commission reveals there is a significant deficit in the after-tax management of superannuation member accounts[1].

Low-tax investors, such as retirees and some self-managed super funds, could earn more if they better considered their portfolios – and returns – on an after-tax basis, suggests leading income investor Plato Investment Management (Plato).

Most investment performance surveys don’t include franking credits, which makes the alpha generated by after-tax management largely invisible to investors, notes Peter Gardner, Senior Portfolio Manager at Plato.

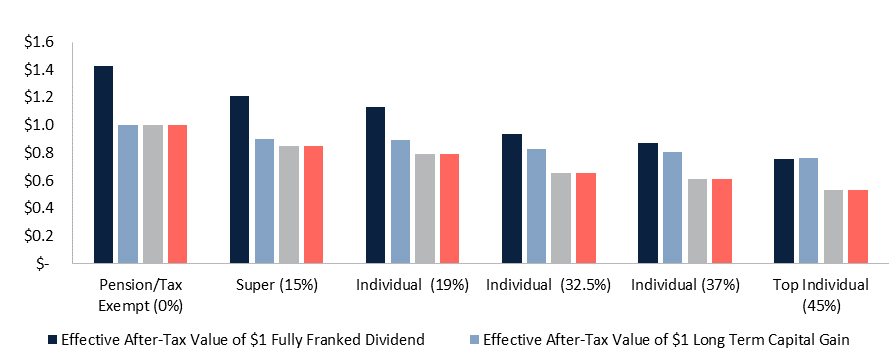

He said: “Fully franked dividends are currently the most valuable form of return for all Australian investors bar those investors on the very highest 45% tax rate, where the 50% CGT discount makes a long-term capital gain the most valuable.”

Dr Gardner said if investments were being managed in a commingled pool, then those assets will likely be managed on a before tax basis as it is not possible to optimise an after-tax outcome for multiple investor types at the same time. “This may leave after-tax alpha “on the table” for many investors.”

He suggested super and managed funds structure their affairs in better ways to make generation of after-tax alpha possible. This included segregating the assets of their accumulation and pension pools so that these assets can be managed separately.

As more Australians moved into retirement, the percentage of assets in pension phase would likely increase for most, if not all, large superannuation funds making the segregation of these assets more practical as well as being more important. “It is common for Australians to start actively engaging with their superannuation fund as they approach retirement so it is important that these superannuation funds can show that they specifically tailor their portfolios for pension phase investors,” he said.

The current after-tax value of one dollar of pre-tax income

Source: Plato

Dr Gardner also noted that off-market buy-backs highlighted the benefits of managing investments from an after-tax perspective of fund members. “Tax-effective buy-backs add value after-tax for tax-exempt investors, and usually, but not always, for low taxed investors (15%/19% tax rates).” Buy-backs added considerable after-tax value for tax-exempt investors in FY2019. Rio Tinto, BHP Billiton, Caltex and Woolworths all completed buy-backs in FY19, adding approximately 20% to total returns including franking credits for each share successfully tendered for investors on a zero tax-rate.

He cited how Plato managed the majority of its Funds Under Management on an after-tax basis “and in our Income/Tax-Exempt strategies, off-market buybacks added 1.2% in after-tax alpha in FY18/19”.

He suggested: “If super funds, fund members and low tax investors fail to account for franking on ordinary or special dividends, investors may be missing out on significant after-tax value. It could add over an additional one per cent return. Over the past financial year, however, the difference has blown out to a massive 3.6%, a huge difference to performance.

“We think Australian investors should be taking advantage of this potential after-tax alpha.”

———