Growing your advice practice

Whichever way you choose to grow your advice practice a robust plan is essential.

There is increasing commentary about the need for financial advice firms to grow in order to survive. This question of growth is starting to reappear post an elongated period of consternation and consolidation in our profession.

This article, sponsored by Insight Investment, will explore the two means traditionally used to grow financial advice practices – through acquisition and organically.

Acquisition

Acquisition – or inorganic growth – has been responsible for the creation of financial planning behemoths such as the big four bank, AMP and IOOF. A glance at any ‘top 100 dealer group survey’ published over the last decade will feature these groups in the top 20 and, more often, the top 10 when ranked by planner numbers.

In the post Royal Commission environment, most of these corporates have or are in the process of divesting or simply closing their financial planning businesses – some at a significant loss – creating a new series of M&A activity among the next tier of dealer groups.

The key benefits of inorganic growth are that it enables you to buy:

- market share – increase growth and profitability quickly

- talent – increase your talent pool through acquisition, particularly skillsets not already available in your team

- clients – you can target acquisition of groups that have the types of clients you want, to either grow a specific segment or diversify your client base.

The 2019 EY Global Capital Confidence Barometer found that companies, broadly, are responding to the pressure to grow or defend their market position against the challenges being posed through digital and technology through mergers and acquisition (M&A).

Interestingly, this year’s barometer found that company management is under increasing pressure to generate long term value that goes beyond just delivering returns for shareholders. There’s a greater focus on creating long-term value for customers, employees, and society as a whole. Arguably, the first of these metrics, long term value for customers, should be front and centre with any transaction between financial advice businesses. If anyone was in any doubt about the importance of a customer-centric view, last year’s Royal Commission put this to rest.

M&A activity in Australia was expected to increase over 2019 according to respondents to KPMG’s Evolving Deals Landscape 2018 survey. At a time where digital disruption is rife, there’s increased competition for clients and the regulatory environment continues to tighten, companies need to increase their capabilities and identify growth opportunities.

The KPMG survey showed that 40 percent of M&A activity is being driven by companies wanting to increase market share, and 38 percent through industry consolidation. KPMG identified a busy year this year for financial services; 48 percent of survey respondents expected an increase in M&A activity, hardly surprising given the big four banks and other vertically integrated businesses had indicated their collective exits from financial advice.

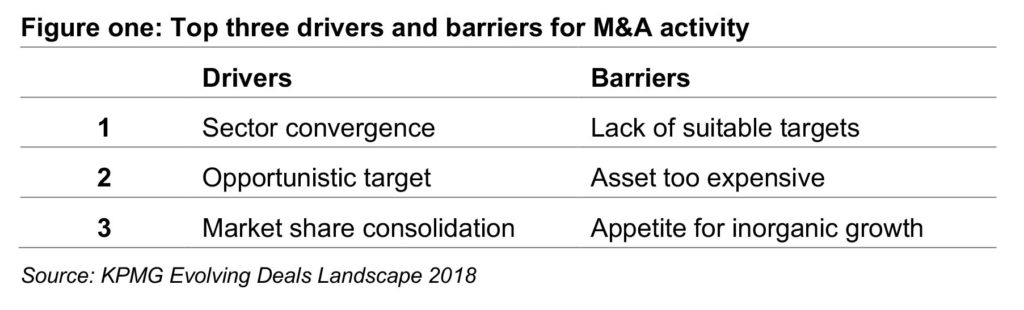

According to the KMPG survey there are drivers and barriers for M&A activity (figure one). Interestingly, a key barrier of increasing impact to M&A is legal and regulatory constraints. KPGM identified this increase as being driven by respondents in the financial services sector, with 52 percent identifying regulatory issues as a key barrier to M&A.

What makes a successful acquisition?

For an acquisition strategy to be successful, a clear strategy for value creation post deal is critical. Essential ingredients include cultural fit, the retention of key people and effective due diligence. While these are broad metrics, they’re as applicable to M&A activity between financial advice practices. After all, while acquisition can be an effective growth strategy for advice practices, it comes adorned with cautionary tales that have seen various dealer groups and financial planning firms come and go over the years.

The key issues for M&A within the financial advice sector are typically centred around the terms of acquisition (including price), cultural alignment issues that are often present when bringing two entities (and associated personalities) together, and effective deployment of current resourcing to the new combined entity. The transition from revenue to EBIT valuation models, potential lack of visibility of financials and further regulatory change can also add to the complexity of the acquisition strategy.

Organic growth

Finding the right business to buy, and at the right price, can be challenging. By the time you make sure the cultural fit is right, the numbers may not add up. The numbers may add up, but key talent may indicate their unwillingness to stay. Acquired clients may not feel loyalty to the new firm, particularly if the adviser with whom they have a relationship with departs. There are many moving parts, and each has the capacity to derail a plan that looks good on paper.

For those advice firms that are considering long-term growth, an organic growth strategy may prove to be lower risk and more sustainable. One way to do this is through a client segmentation strategy.

Much has been discussed about the growing inability of financial advice firms to service clients with simpler needs or smaller investment balances due to the rising operational and compliance costs associated with a highly regulated environment. In particular, the cost of managing investment portfolios (particularly bespoke portfolios) has from many reports become preclusive for financial advice firms and their clients.

As a result many firms have segmented their client base to reflect appropriate matching of their advice value proposition and particular segments of client needs. This has been a positive step for many firms, creating better alignment with clients and facilitating a more sustainable business model.

Client segmentation strategy

Conceptually, a client segmentation strategy concept is relatively straightforward. It aims to improve the efficiency and profitability of a financial advice business by matching the level of services provided to each client and their value to the firm.

Traditionally, clients have been segmented as A, B, C (and so on), with A clients being the high net worth, high touch clients and those at the lower end being the basic, low end clients with few assets and basic needs. It’s important, however, to ensure that all clients receive advice that is compliant, in line with client objectives and meets the best interests test.

On top of providing a compliant level of advice, you can then define the services provided for each segment. By starting with the absolute must do requirements for each client, you can add service levels to the higher touch clients.

If for example, your segments were A, B and C, you can define the basic service provided to each, adding more services for top-tier clients or differentiating between each based on service delivery. For example, a financial planning practice may charge A and B clients a regular monthly or quarterly fee (and provide the services to justify it) but simply charge C clients on an hourly basis as services are required.

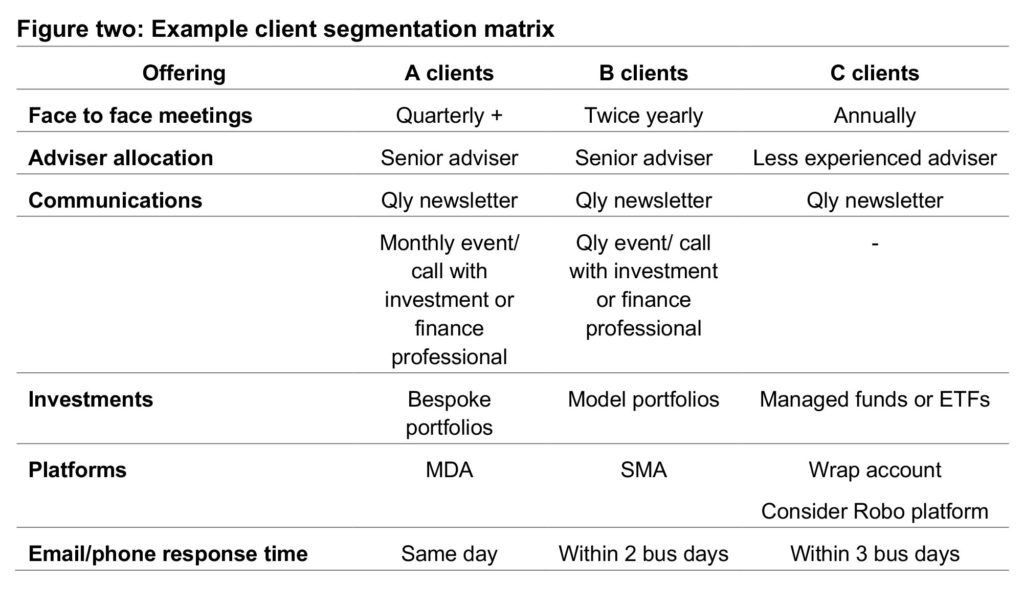

It’s a good idea to develop a client segment matrix (figure two). Consider what value add you and your team can provide to clients. For example, you may provide a quarterly newsletter to all clients, but provide additional opportunities for A and B clients to meet with or hear from a range of finance professions – investment managers, research analysts, brokers or tax specialists.

Building a pipeline of ‘potential’ segment clients in a controlled manner may create a lower cost alternative to acquiring clients that meet the segment criteria ‘on paper’ or waiting until these clients meet the target segment profile at some point in the future. The financial advice relationship is built on trust, which in most cases develops over a period of time.

This organic approach allows time to build trust and may present the adviser with profitable and loyal clients over time, as long as the cost to serve this pipeline segment is managed efficiently. And remember; clients don’t necessarily remain in their segments, they may move up over time as they accumulate assets, receive inheritances, progress in their careers or grow their businesses.

If you choose to segment your clients and then grow specific segments, it is imperative to manage the cost to serve. One element of this is portfolio governance and implementation. In-house or bespoke portfolios are likely to be uneconomic for clients with smaller balances, so a solution is required that is reasonably priced, but provides sufficient diversification within a robust governance and implementation framework in order to minimise agency risk.

Organic growth holds inherently less risk than acquisition and has historically been present in many financial planning firms by way of fee structures based on percentage of assets (allowing investment portfolio growth to provide revenue uplift over time) and all important client referrals. However the move to fee for service pricing models has changed the nature of business growth.

Strong financial planning firms continue to attract client referrals and as is supported by various academic studies, referred clients are more profitable and exhibit greater loyalty[1]. However when assessing potential client suitability, are financial planning firms compelled to accept only those referrals that meet their preferred segment attributes currently? What if a referred prospective client has strong potential to meet the criteria at some point in the not so distant future? Can this be managed without diluting the benefits of the segmented client model?

The answer may lie in the relative risk and expense of organic growth versus acquisition. This requires an assessment of cost per client via acquisition versus the cost of serving a ‘potential’ segment client. For example, assuming a client with $500,000 in superannuation, with insurances, mortgage and ongoing budget coaching program generates $6,000 in revenue per year. Assuming a multiple of 2.5 times, the cost of client acquisition is $15,000 without allowing for associated financing of acquisition[2].

Whichever way you choose to grow your advice practice – by acquisition or through organic growth – a robust plan and a sound understanding of costs to service your newly acquired (and existing) clients is essential to ensure the ongoing success and profitability of your practice.

———-

[1] Do referral programs increase profits? Faculty Wharton Case Study Vol. 5, No 1, 2013; Philipp Schmidt, Bernd Skiera and Christophe Van den Bulte

[2] Example only, assumptions made are not an actual case, a forecast or a guide to client pricing models

![]()