Weekly market update – week ending 6 December, 2019

Investment markets and key developments over the past week

Share markets were mixed over the last week with falls in the US and Europe on trade war fears and mixed economic data, but Japanese shares rose on fiscal stimulus plans and Chinese shares rose too. The Australian share market fell back from record highs taking its lead from the declines in US shares and worries about global trade but with retailers particularly hard hit by ongoing signs of very weak consumer spending. Despite the decline in US and Eurozone shares, bond yields mostly rose including in Australia as did commodity prices with oil prices up on OPEC nearing a deal to cut production (although there looks to be little in the way of actual new production cuts). The Australian dollar rose as the US dollar fell.

The past week saw the usual argy bargy of conflicting comments and reports regarding US/China trade talks and trade wars generally. The week started off with President Trump putting tariffs on Brazilian and Argentinian steel and aluminium, the US threatening tariffs on $US2.4bn of imports from France, more reminders from the US side of the scheduled December 15 tariffs, Trump downplaying the urgency of a deal and Congress passing another human rights law in relation to China only to then see reports that progress is still being made on a deal and Trump saying the talks were “moving along well”. Putting this into some perspective. First, the mini tariffs on Brazil, Argentina, France, etc, are a way of appealing to Trump’s base and showing China he is still tough without doing much economic damage to the US economy. Second, they keep the pressure up on the Fed to ease more. Third, the proposed French tariffs are part of a wider dispute regarding the taxation of digital services that isn’t related to Trump’s trade wars. Finally, the pressure on China and Trump to cut a deal given their economic slowdowns and the US election next year remains immense. In particular, hiking tariffs on consumer goods 10 days before Christmas is not something Trump really wants to do. So our view remains that some sort of deal will be cut either ahead of December 15 or early next year and either way the tariff hike won’t proceed. But I have to concede Trump is Trump, China is playing hard ball and the risks are high.

What might a Phase 1 tariff deal involve? Increased Chinese purchase of US agriculture products; tighter Chinese IP protections; greater US access to the Chinese financial sector; cancellation of the December 15 tariff hike; the roll back of some US tariffs on China; and some commitment to Phase 2 talks.

The House of Representatives in the US is moving rapidly towards voting to impeach President Trump. This would be followed by a Senate trial in January. All of this could cause bouts of volatility, but it remains very unlikely that 20 Republican senators needed to get to the required 67 out of 100 senators will support removal from office. This is because public support for impeachment is only running around 48% and only 10% of Republican members support impeachment.

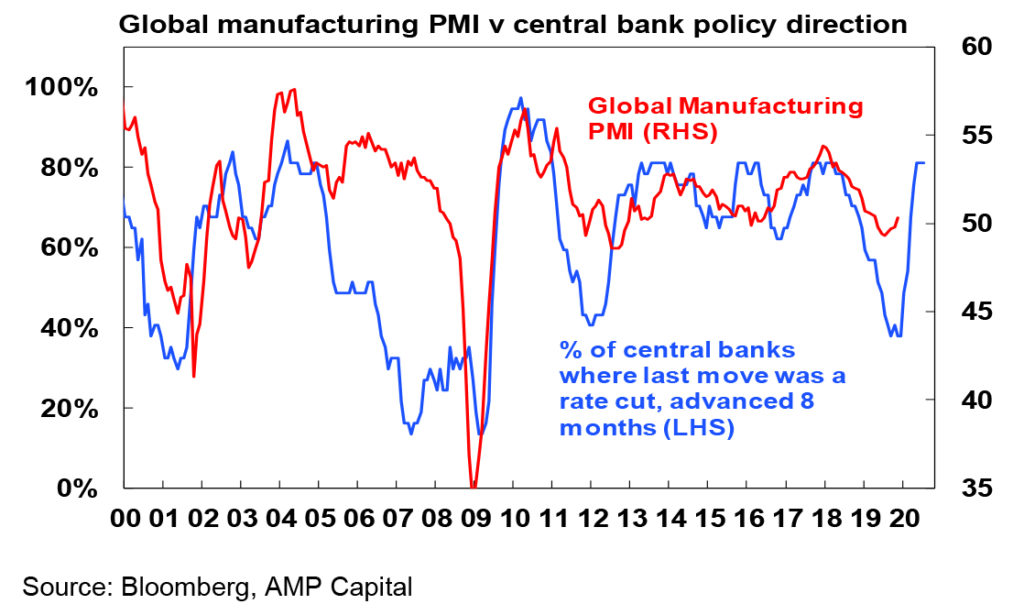

Business conditions PMIs continue to edge up globally. The global average manufacturing and services conditions PMIs moved up again in November, suggesting that the monetary easing seen this year is getting traction.

While the RBA left interest rates on hold at its December meeting, we retain our long-held view that the cash rate its on its way to 0.25% and that quantitative easing will follow. Its well known that interest rates impact the economy with “long and variable lags” and I have usually assumed this takes place over 6 to 12 months as it takes a while for rate cuts to boost confidence and convince people to spend more. So I can understand the RBA’s desire to continue to “monitor developments” for now. However, the flow of data over the last week was on balance poor and adds to the flow of poor data seen over the last month. Sure, the September quarter national accounts show that the economy is still growing but it continues to be far weaker than the RBA has been expecting, growth slowed in the September quarter from the June quarter and private final demand is continuing to go backwards. To get to the RBA’s 2.3% growth forecast for this year requires 0.8% quarterly growth in the current quarter which is looking very dubious, particularly with retail sales, car sales and the trade balance already off to a bad start in October. The more likely scenario is that growth this year will come in around 1.9%, which will mean another round of growth downgrades from the RBA. All of which suggests that the economy in the words of RBA Governor Lowe is still “moving away from, rather than towards, our goals of full employment and inflation.” Ideally more fiscal stimulus is needed soon – but the growth numbers were probably not weak enough to see a loosening of the fiscal purse strings in the mid-year budget review due around December 16. As such the pressure all falls back on the RBA. As a result we remain of the view that the RBA will cut the cash rate by 0.25% in each of February and March, which will take it to the RBA’s floor of 0.25% beyond which QE is likely, but probably not until around mid-year after the RBA gets to see whether there is any substantial fiscal easing in the May Budget.

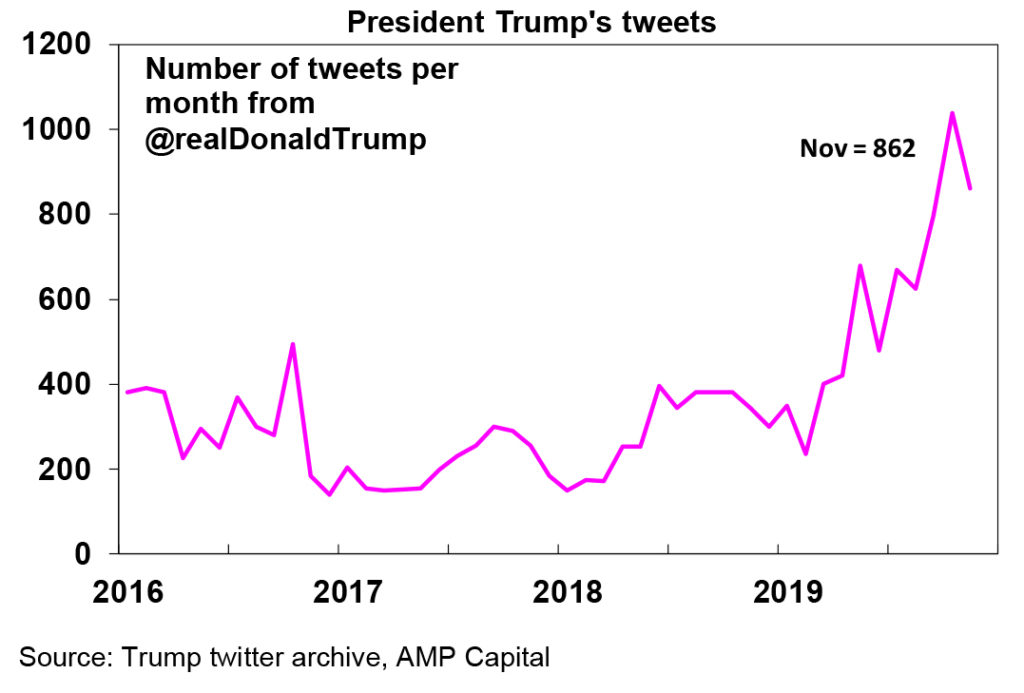

President Trump’s tweet count fell back last month to 862, down from a record 1039 in October, but its nearly 29 a day and well up from his norm of around 300 a month. If his tweets are a guide to his stress level, then it’s clearly still high. I am still trying to work out what he meant by his 9th August tweet: “We need a President who isn’t a laughing stock to the entire World. We need a truly great leader, a genius at strategy and winning. Respect!”

If you are into Taylor this is worth checking out.

Major global economic events and implications

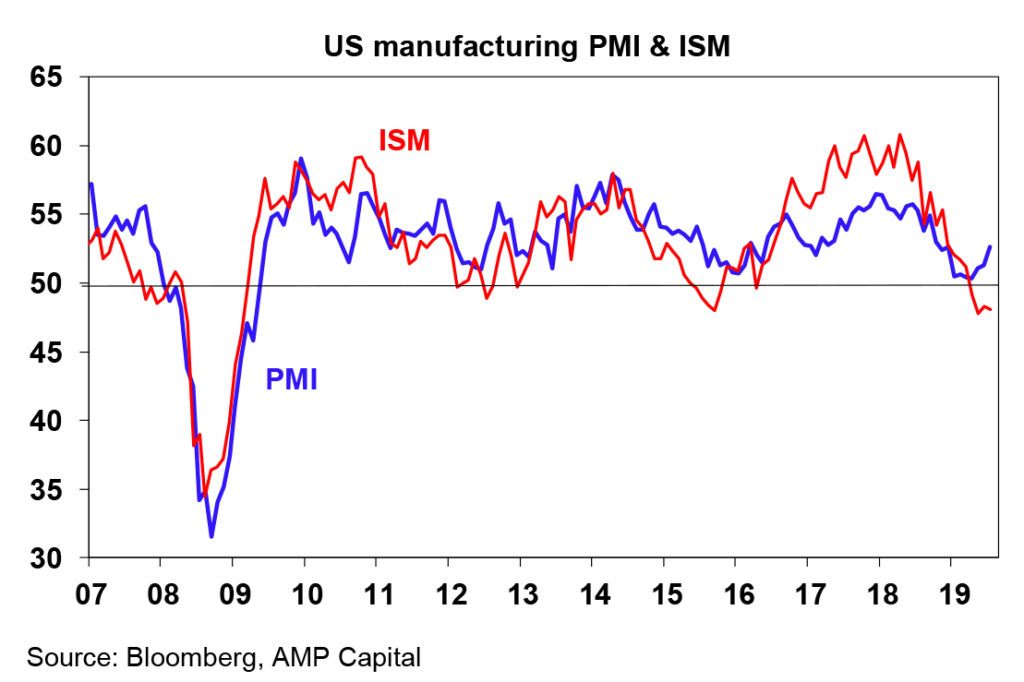

US economic data was mixed with the ISM business conditions indicators for November falling but the Markit PMIs getting revised to show bigger increases, construction spending falling in October, a weak private survey on November payrolls but continuing very low unemployment claims. The divergence between the manufacturing ISM and the Markit manufacturing PMI – which is based on broader survey and has tended to be more stable – is worth noting though with the latter now clearly pointing up.

The refocusing on fiscal stimulus has clearly spread from the US with Japan announcing plans for roughly a 1% of GDP fiscal stimulus (once new measures are allowed for) which should go some way to offsetting the impact of the October sales tax rate hike from 8% to 10%. The latter drove a sharp decline in household spending in October.

China’s Caixin business conditions PMIs showed a further improvement in November, consistent with the message from the official PMIs in suggesting that the Chinese economy may be stabilising or picking up. More monthly readings will be needed to confirm this though.

Australian economic events and implications

Australian economic data over the past week was weak. Sure there was some good news: the economy is still growing; the current account recorded its second quarterly surplus; house prices are continuing to rise suggesting that rate cuts are “helping”; and the household savings rate is up sharply thanks largely to tax cuts providing scope for future spending. However, unfortunately the negatives dominated with September quarter GDP growth coming in weaker than expected at just 0.4% quarter on quarter and slowing from the June quarter; private spending going backwards; building approvals down sharply pointing to ongoing weakness in housing construction; ANZ job ads continuing to slide pointing to a further slowing in employment; retail sales and car sales starting the current quarter on a soft note; and the trade surplus falling sharply in October suggesting lessening support to the economy from the terms of trade and net exports.

Sure retail sales may see a November boost from Black Friday and Cyber Monday sales (whatever they are) but such hoopla likely just swaps spending around between months – with last year seeing a solid November then payback in December.

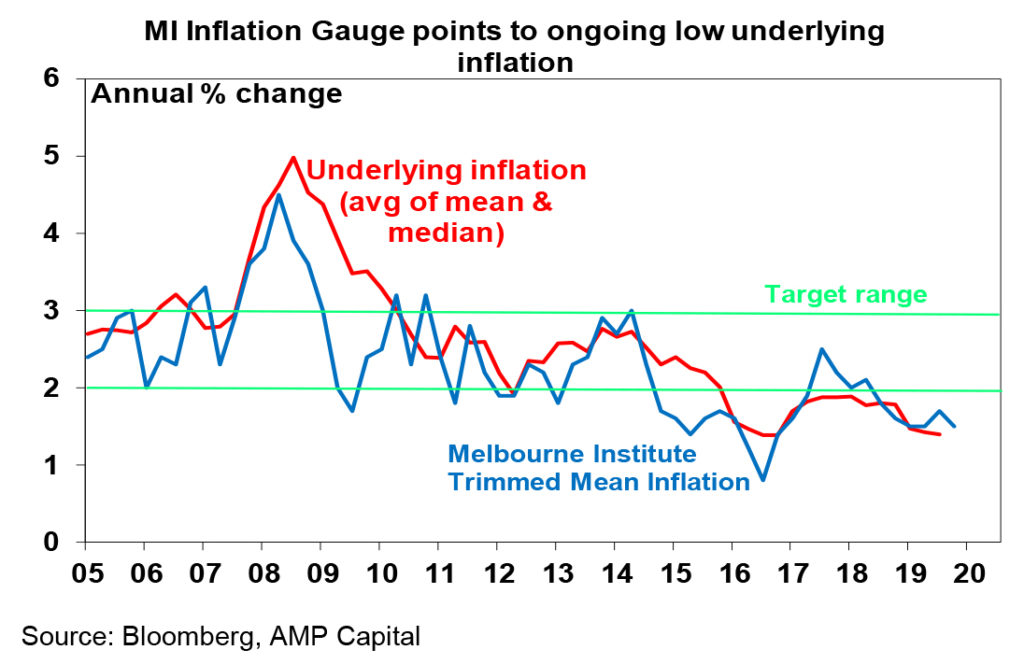

What’s more the Melbourne Institute’s Inflation Gauge remained soft in November despite higher petrol prices and the drought, suggesting inflation remains well below target.

What to watch over the next week?

The big focus in the week ahead will be whether the scheduled December 15 15% tariff on roughly $US155bn of Chinese consumer goods imports into the US precedes or is cancelled as a result of a Phase 1 trade deal or postponed as talks continue. For the reasons noted earlier our view is that it will be averted.

The Fed meets Wednesday and is not expected to change interest rates (with the money market putting the probability of a move at zero) given that recent US economic data has been reasonable and consistent with the Fed’s outlook and some of the risks to the outlook have diminished. The dot plot is expected to show no change in rates for the year ahead and then one rate hike in each of 2021 and 2022. However, Fed Chair Powell is expected to reiterate that the Fed remains data dependent and that he will not raise rates without a significant and persistent move up in inflation. So the Fed is likely to be seen as dovish. On the data front in the US, expect core CPI inflation for November (Wednesday) to have remained at 2.3% year on year and retail sales (Friday) to show a solid gain.

In the Eurozone, the ECB is not expected to make any changes to monetary policy given the big easing announced in September but new ECB President Lagarde will be watched closely to see what her biases are going forward.

Japanese September quarter GDP growth (Monday) is expected to be revised up slightly from 0.1%qoq to 0.2%qoq and the latest Tankan business survey to be released Friday will likely show a softening in conditions.

Polls suggest that the Conservatives will win the UK election on Thursday, which will mean that PM Johnson’s Brexit deal with the EU will be signed and the UK will have a soft exit from the EU (ie leave but retain current trading arrangements) by January 31 and then enter into negotiations for a free trade deal. These could still end in a hard exit if no free trade agreement is reached, but the threat of economic disruption will likely work against that particularly given that the UK will be officially out of the EU anyway. If Labor wins there will probably be another Brexit referendum and markets will fret about the far-left policies of Labor although these may be softened by the influence of other parties if Labor requires a coalition to govern.

Chinese CPI inflation for November (Tuesday) is likely to slow slightly from 3.8%yoy given a recent fall in pork prices and underlying inflation will likely remain weak.

In Australia, business conditions according to the NAB business survey for October (Tuesday) and consumer confidence (Wednesday) according to the Westpac/MI survey for November are likely to be soft. ABS house price data for the September quarter is likely to confirm the bounce back in dwelling prices that has been long ago reported by private sector surveys with a 2% rise. A speech by RBA Governor Lowe at the Australian Payments Network summit on Tuesday will be watched for any clues on rates.

Outlook for investment markets

Share markets remain at risk of further short-term volatility given issues around trade, impeachment noise and mixed economic data. But we are now entering a period of positive seasonality with the Santa Claus rally often seen from mid December. More fundamentally shares remain cheap against low bond yields, global growth is expected to improve through next year and monetary policy is easy all of which should support decent gains for shares on a 6-12 month horizon.

Low yields are likely to see low returns from bonds once their yields bottom out if they haven’t already, but government bonds remain excellent portfolio diversifiers.

Unlisted commercial property and infrastructure are likely to see reasonable returns. Although retail property is weak, low for longer bond yields will help underpin unlisted asset valuations.

The election outcome, rate cuts, tax cuts and the removal of the 7% mortgage rate test are driving a rebound in national average capital city home prices led by Sydney and Melbourne. But beyond an initial bounce which could run into first half next year, home price gains are likely to be constrained through this latest upcycle as lending standards remain tight and rising unemployment acts as a constraint. The risk though is that the recent surge in prices goes on for longer as property price gains in Australia have a habit of feeding on themselves.

Cash and bank deposits are likely to provide poor returns as the RBA cuts the official cash rate to 0.25% by early next year.

Our base case remains that the $A still has more downside to around $US0.65 as the RBA eases further. However, with the US dollar looking like it may have peaked and given excessive $A short positions there is a risk that we may have already seen the bottom (at $US0.6671 early in October).

By Shane Oliver