Economic and financial perspectives

- Record expansion: Australia’s record economic expansion is now in its 29th year. Interest rates have fallen to fresh record lows; wages are growing near 2.2 per cent; underlying inflation is around 1.6 per cent; the jobless rate is 5.3 per cent.

- Good year for shares: Total returns on Australian shares (All Ordinaries Accumulation index) have lifted by 24 per cent over 2019 (20-year average +9.5 per cent) to a smidgen below record highs.

The report is useful to assist investors to start planning for year 2020.

What does it all mean?

- Calendar year 2019 is almost complete and we are mid-way through the 2019/20 financial year so it is an opportune time to see how investments, financial markets and economies have been performing.

- Overall, the global economy has slowed over the past year, largely restrained by the US-China trade conflict – weighing on business investment and manufacturing activity. Central banks have cut interest rates to minimise recession risks at a time of low inflation and low unemployment. The US economy remains in excellent shape supported by resilient consumers and a solid job market. The Chinese economy has slowed in response to the trade dispute with the US and on-going deleveraging but authorities have been stimulating their economy, boosting demand for Aussie goods and services.

- The Australian economy is currently growing at a 1.7 per cent annual pace. Just like other major economies, growth slowed over the year. Uncertainty over the May 18 Federal Election result led to business investment caution. Consumer spending decelerated to due to tepid wage growth, falling property prices and increasing job insecurity. Arguably only home prices – especially in Sydney and Melbourne – have lifted in the post-election period. However the sharemarket hit record highs at the end of November, further boosting the “wealth effect”.

- The Reserve Bank re-assessed policy settings in late May in response to stubbornly low inflation and weak private sector demand. The Reserve Bank now believes that unemployment can fall to 4.5 per cent before igniting inflationary pressures. As a result the Reserve Bank cut the cash rate by 25 basis points in June, July and October. Inflation is expected to remain below 2 per cent in 2020 with unemployment near 5.25 per cent.

- Returns on shares have lifted by just over 24 per cent in in 2019 and growth of 7-11 per cent is expected in 2020. The Australian dollar should continue to support the record economic expansion, largely holding in the late 60s/early 70-cent range against the greenback.

What does the data show?

Interest rates

- The cash rate was reduced from 1.50 per cent to 0.75 per cent with 25 basis point rate cuts in June, July and October.

- The market-determined 90-day bank bill rate fell from highs near 2.04 per cent in January to record lows of 0.82 per cent and is ending the year near the lows. Yields on the long bond – 10-year government bond – fell from highs of 2.33 per cent in January to lows of 0.87 per cent in early October and is ending the year near 1.10 per cent.

Currencies

- The Aussie dollar has fallen around 3 per cent against the greenback over 2019. The Aussie started the year around US70 cents and is ending the year near US68 cents. The Aussie hit highs of US72.68 cents in late January while lows (also decade lows) of US67.08 cents were set in early October.

- We have calculated that the Aussie is ranked 85th strongest against the US dollar of 120 currencies tracked. The Syrian pound is up the most against the greenback (up 15.5 per cent) while Egypt, Russia, Israel and Thailand are all up around 6-10 per cent. The weakest currencies have been in Argentina (down almost 59 per cent), Zambia (down 30 per cent) and Haiti (down 20 per cent). Only 31 currencies have lifted against the greenback over the year. Notably the UK pound is up 3 per cent with Japan up 1.5 per cent.

- The Aussie has gradually trended lower for around three years. Over most of the period US policy interest rates were rising while the Aussie cash rate was left unchanged. Since August the Aussie dollar has generally held US67-69 cents with both the US and Australia cutting policy rates three times since June.

Commodities

- Commodity prices have been mixed over 2019. The Commodity Research Bureau futures index has risen by 6 per cent over the year, but the CommSec daily index is down by 2.5 per cent, broadly matching a 3 per cent fall in the Aussie dollar against the greenback.

- At one end of the spectrum, thermal coal has fallen by 35 per cent with liquefied natural gas (LNG) down by 38 per cent. At the other end of the spectrum, beef prices have soared by around 50 per cent, iron ore has gained 22 per cent, crude oil has lifted 29 per cent and gold has gained 14 per cent.

- Base metal prices have fallen up to 11 per cent with zinc down the most but nickel has risen by 25 per cent.

- Rice has risen 5 per cent with sugar up 9 per cent but cotton has lost 9 per cent and wool has lost 19 per cent.

Sharemarket

- The Australian sharemarket started 2019 with the All Ordinaries at 5,709.4 and the ASX200 at 5,646.4. The All Ords currently stands at 6,813.5 points (up 19.3 per cent) with the ASX200 is at 6,707.0 (up 18.8 per cent).

- The ASX200 hit record highs of 6,845.1 in late July but promptly retreated to near 6,400 in mid-August. The ASX 200 hit new record highs in late November as optimism grew on a US-China trade deal.

- We estimate that Australia is 21st of 72 global bourses. So far 56 bourses have recorded gains in 2019. The best performer has been hyperinflation-affected Zimbabwe but Greece, Russia and Romania have lifted more than 35 per cent. New Zealand has lifted around 30 per cent. The US Dow Jones has lifted by around 20 per cent.

- The worst performers have been Lebanon, West Africa and Nigeria. African and Asian sharemarkets have generally underperformed.

Investment returns

- Total returns on Australian shares (All Ordinaries Accumulation index) have so far lifted by 24 per cent over 2019, hitting record highs in late November. Returns on shares are set for the best result in a decade. Returns on dwellings have risen by 4.1 per cent to date in 2019 while returns on government bonds have lifted by 8.6 per cent.

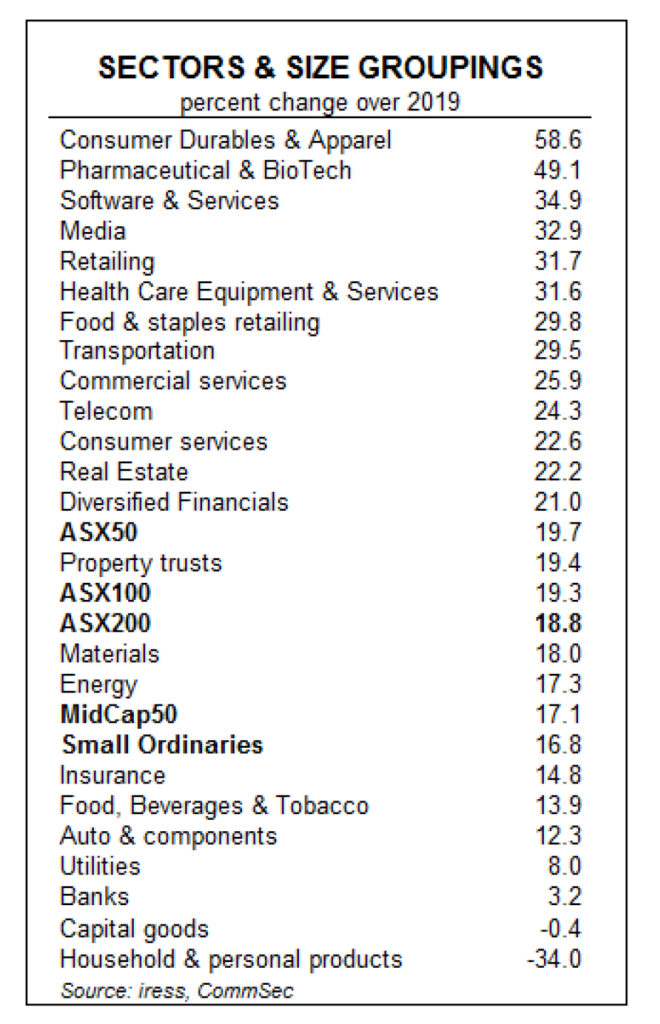

Sectors and size groupings

- Of the 22 identified industry sub-sectors, only two have recorded declines so far in 2019 – Household & personal products (down 34 per cent) and Capital goods (down 0.4 per cent).

- Leading the gains has been Consumer durables & apparel (up 58.6 per cent) from Pharmaceuticals & biotech (up 49.1 per cent) and Software & services (up 34.9 per cent).

- Of the size categories, the ASX50 has outperformed (up over 19.7 per cent) from the ASX100 (up 19.3 per cent) and MidCap50 (up 17.1 per cent) and the Small Ordinaries (up 16.8 per cent).

What are the implications for investors?

- Returns on shares are near record highs. In fact sharemarket returns have only fallen once in the past 10 years. So an investor that has employed a diversified strategy across asset classes would be well pleased with the performance over recent years.

- The outlook for the sharemarket remains positive. The Reserve Bank will maintain its stimulatory monetary policy settings over 2020. The Reserve Bank has scope to cut rates another two times before considering ‘unconventional’ policies like buying government bonds from the private sector.

- But the Reserve Bank stresses that it can’t do it all.

- Certainly Federal and State governments are active in advancing new infrastructure projects. And with budgets broadly balanced or in modest surplus, there is scope for even more fiscal stimulus to be applied.

- And the Federal Government is believed to be considering bringing forward tax cuts with an announcement in the May 2020 Budget.

- Over the coming year, infrastructure building and net exports will add to economic growth. The Reserve Bank hopes that the stimulatory policy settings will lead to stronger household spending as well. Weaker home building will be the main factor weighing on growth in the first half of the year. But mining investment is finally set to make a positive contribution to growth after 6 years.

- Last year we noted: “The Australian ASX 200 share index is expected to rebound by 10-12 per cent in 2019 after a decline of around 6-8 per cent in 2018. Including dividends, total returns are tipped to lift by 14-17 per cent in 2019. While above-normal growth of total return on equities is expected, this must be seen in the context of the below-normal performance in the latter part of 2018.”

- The forecasts actually are proving too conservative – although there is still three weeks of 2019 to go.

- Over the coming year CommSec expects the All Ordinaries index to be near 6,900-7,200 points in June 2020 and 7,100-7,400 points in December 2020 supported by the “search for yield”. But increased focus on earnings, bank dividends and business profitability could present risks to our outlook.

- Housing markets across the nation are continuing to rebalance to reflect the increase in supply (new home construction). Government grants and rate cuts will ensure that first home buyers remain active. Investors have also returned, and while sharemarkets currently have more attractive investment returns, home prices are tipped to lift over the coming year.

- Over 2019/2020, national home prices may post gains of around 6-9 per cent. Since the Federal Election there have been signs of stabilisation of Sydney and Melbourne home markets with prices up sharply on stronger buyer demand and supply constraints.

- The low inflation/low interest rate environment is entrenched, meaning that lower nominal investment returns are also here to stay. So investors will need to remain flexible and alert to the returns achieved across sharemarket sectors and across asset classes to ensure that their savings are keeping pace with the cost of living.

- The ‘triple L’ theme (low unemployment, low inflation, and low interest rates) will also dominate global markets over the coming year. Central banks still favour rate cuts over rate hikes despite unemployment at or near multi-decade lows in many advanced nations.

- The Aussie dollar is expected to largely trade in the late 60s/early 70s against the US dollar over most of the coming year. But interest rate differentials between the US and Australia and the US-China trade discussions are the two factors that could move the Aussie out of the tight range. And the potential deployment of unconventional monetary policy by the Reserve Bank – most likely government bond purchases – presents the biggest downside risk to the Aussie dollar should current stimulus fail to lift growth.

- At the time of writing, financial markets were waiting on the next instalment of US-China trade talks. Successful completion of the talks should lead to a major upgrade in prospects for the global economy. If agreement remains elusive, expect stimulatory monetary policies to remain in place in China as well as advanced global economies.

- Of course another significant risk to financial markets in 2020 is the US Presidential election due in November.