Weekly market update – week ending 14 February, 2020

Investment markets and key developments over the past week

Share markets generally rose over the last week but gains were constrained by ongoing concerns about the coronavirus outbreak after China announced a large increase in new cases. Reflecting the generally positive global lead Australian shares managed to push back up to around their January record high with strong gains in financials, utilities, health and consumer discretionary stocks offsetting coronavirus related weakness in resources stocks. Bond yields were little changed but oil, metal and iron ore prices rose and the Australian dollar rose from its lowest level since 2009.

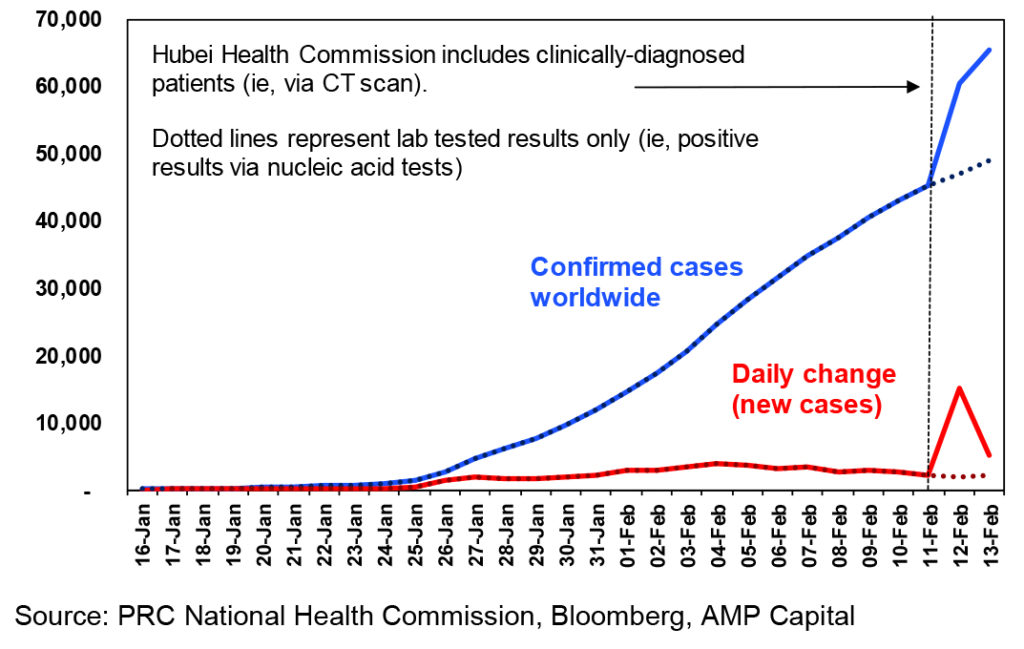

The number of confirmed coronavirus cases (now named Covid-19) in China spiked over the last week, after Hubei province added patients confirmed via clinical tests (CT imaging scans) but who have tested negative via lab tests (ie nucleic acid testing). There are issues with both testing methods – the lab tests are slower and can sometimes give false negative results whereas CT scans may just be revealing conventional pneumonia. It could be a case of China front loading some bad news after it replaced some top officials in Hubei and WHO has stuck to reporting only lab confirmed cases. On the basis of the latter there is still some evidence of a downtrend in the number of daily new cases. And this would likely also be the case if the clinically diagnosed cases are spread back over the last few weeks for which they relate to.

Of course, there is a lot of uncertainty around this and it may become clearer as WHO becomes more involved on the ground in China in the week ahead. More broadly though the picture is little changed: 99% of cases are still in China; 80% of these are in Hubei province; the transmission of cases outside China beyond the cruise ship in Japan remains low and the mortality rate is just over 2% and mainly relates to older people with pre-existing conditions.

The key to watch remains the number of daily new cases and the spread of cases outside China – although in terms of the former this is being made difficult at present by volatility in the number of cases, it’s worth noting that this is not unusual in the case of virus outbreaks. Although, there is much uncertainty our assessment remains that the most likely scenario with 75% probability is that the virus will be contained in the next month or so. But with many Chinese staying at home as confirmed by various indicators around transport congestion, coal consumption and property sales the hit to Chinese growth and the flow on to the global growth will be big this quarter. In fact, it’s conceivable that global growth will be zero in the March quarter. Rough estimates suggest that 30% of China’s population and 50% of its GDP is under lockdown and each week this remains the case will knock 1% off Chinese GDP and nearly 0.2% directly off global GDP. However, if the outbreak is contained in the next month or so as we expect then growth will bounce back in the June quarter and shares will largely look through it.

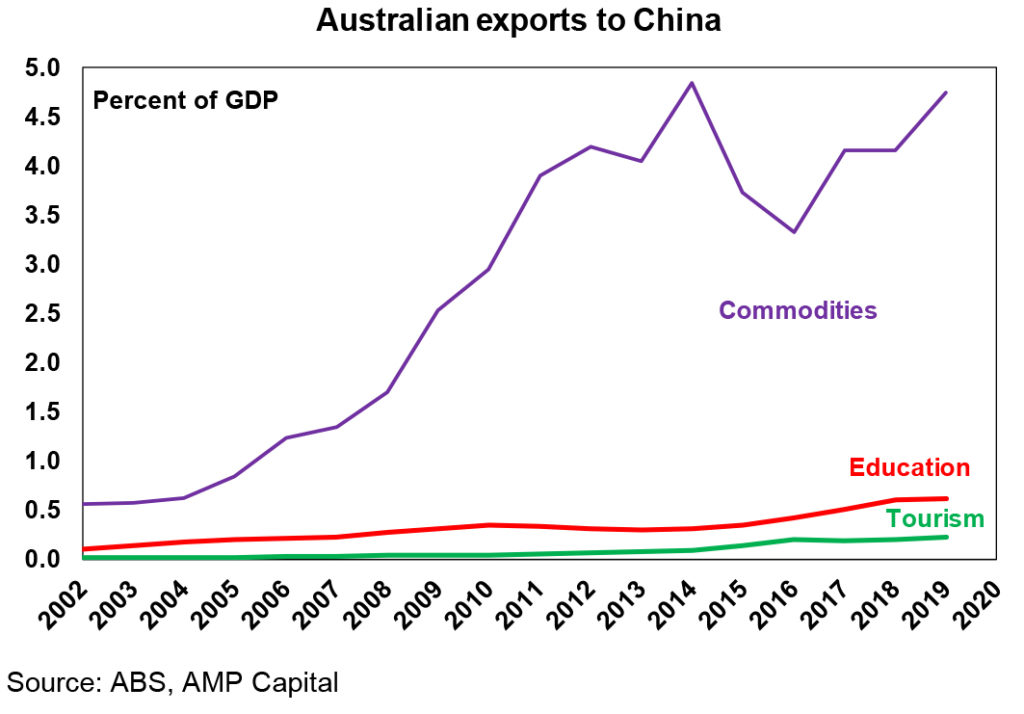

For Australia, our assessment remains that the combination of the drag from the bushfires and coronavirus will detract around 0.6% from March quarter GDP which will see the economy go backwards by around -0.1%. But growth should rebound in the June quarter as the rebuilding from the bushfires kicks in and if as we expect the Covid-19 outbreak is soon contained. The broader vulnerability of the Australian economy should the outbreak drag on though is highlighted by the following chart which shows that Chinese tourists account for 0.2% of Australia’s GDP, Chinese students account for 0.6% and commodity exports to China account for nearly 4.8%, all of which are well up from where they were at the time of the SARS outbreak back in 2003.

Does the strength of socialist Bernie Sanders so far in the Democrat primaries pose a threat to the US share market? Maybe, but this is unlikely for several reasons. First, he is benefitting from the decline of fellow far leftist Elizabeth Warren and the splintering of the centrist vote between Buttigieg, Klobuchar, Biden and (from Super Tuesday) Bloomberg. Second he may have “won” in New Hampshire by getting more votes than anyone else but it was only 26% of the vote and while the leftists are getting around 35% of the vote the centrists got 52% so if this continues there will be far more centrist delegates at the convention that far left delegates. Third, even in the unlikely event he gets the nomination, as an avowed socialist he is unlikely to win in the mid-west where it matters. Finally, as long as the US economy remains strong, the historical experience suggests Trump is likely to be re-elected. All of which is why the US share market has been non-fussed by the rise of Sanders.

All this virus stuff is a bit depressing, time for a great Taylor song.

Major global economic events and implications

US economic data was mostly good. Job openings fell but workers quitting for new jobs remained strong as do other labour market indicators and small business optimism remains strong with a rise in January. Core inflation was a bit stronger than expected in January but suggests that core private final consumption deflator inflation – the Fed’s preferred measure – is around 1.8% year on year, which is still just below target.

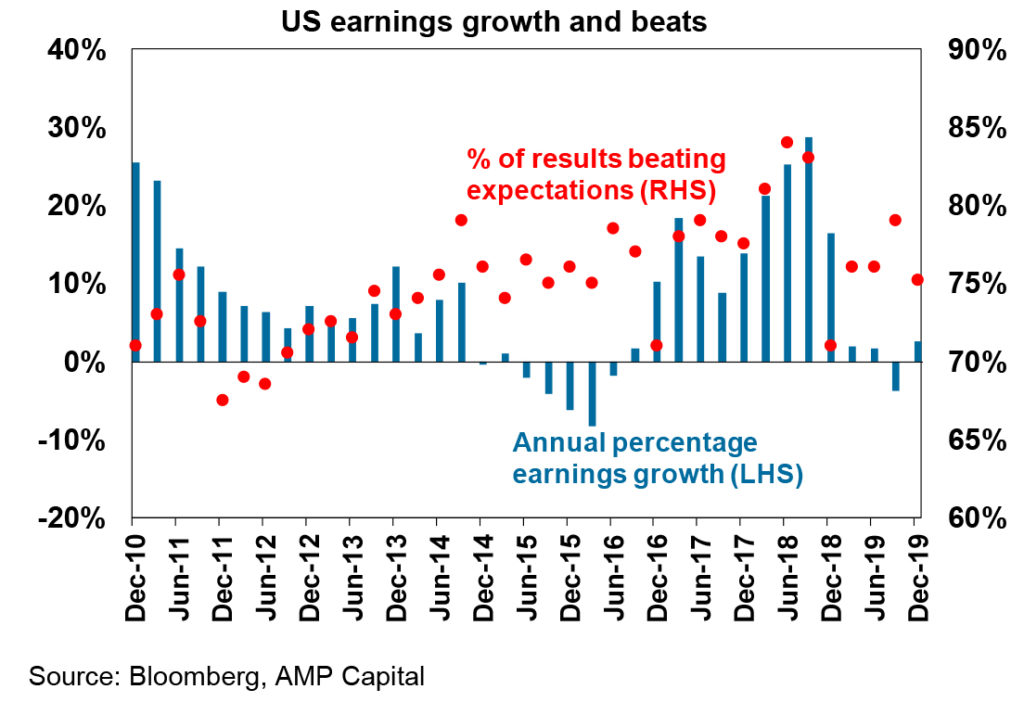

US earnings results have been good. Around 80% of US S&P 500 companies have reported December quarter results with 75% beating on earnings (which is in line with the long-term average) by an average of 5% and 67% beating on sales. Earnings growth looks like its up about 2.5% year on year, compared to expectations a few weeks ago for a 2% decline. Market expectations for 10% earnings growth this year look a bit too high, but its likely to be around 5-7% which is still reasonable.

Chinese consumer price inflation rose further to 5.4% year on year in January but it was all due to food prices with core inflation weak at 1.5%yoy and producer price inflation of zero. There is no constraint on further PBOC easing here.

Australian economic events and implications

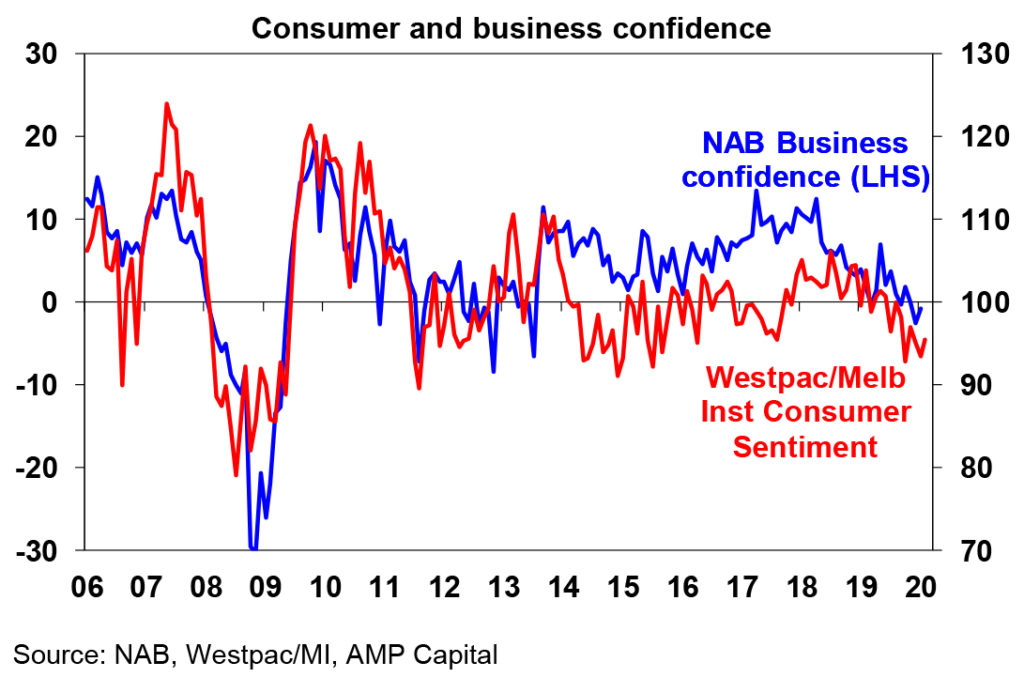

Australian business confidence as measured by the NAB survey in January and consumer confidence as measured by the Westpac/MI consumer survey for February both rose slightly. This is a bit better than we had expected given the bad news around the bushfires and Covid-19, but the gains were small and they are really just stable at a low level consistent with soft investment and consumer spending in the near term.

Meanwhile, housing finance rose again in December led by owner occupiers and is now up 20% from its mid year low providing further confirmation of the upswing in the property market. Of course, this is yet to really boost the housing credit data which relates to the stock of debt because new lending is being offset by the rapid paydown of existing debt, but it likely will start to in the months ahead.

It’s early days in the December half profit reporting season as only about a quarter of major companies have reported but results so far have been a bit mixed. 61% of companies have seen their profits rise from a year ago but this is below the long term norm of 65%, half of the results so far have surprised on the downside which compares to a norm of just 26%, and only 52% of companies have raised their dividends which is well down from the 77% of companies raising their dividends back in August 2018.

![]()

What to watch over the next week?

News on the Covid-19 outbreak will no doubt continue to dominate over the week ahead as investors attempt to assess whether it is being contained or not.

February business conditions PMIs to be released Friday for the US, Eurozone and Japan will also be watched closely in terms of gauging the outbreak’s economic impact. Up until January, global business conditions PMIs had been recovering nicely from last year’s lows.

In the US, housing related indicators are likely to show continued strength with the latest plunge in mortgage rates providing more help for the sector. Expect home builders’ conditions (Tuesday) to remain strong, housing starts (Wednesday) to pull back a bit but after a big rise in December and permits to build new homes to rise. Manufacturing conditions indexes for the New York and Philadelphia regions will also be released and may provide additional guidance as to the economic impact of the Covid-19 outbreak. The minutes from the Fed’s last meeting are likely to indicate that the Fed remains positive on the outlook for the US economy but aware of the risk posed by Covid-19.

Japanese December quarter GDP (Monday) is likely to show a sharp 1% contraction reflecting the impact of the sales tax hike in October. December industrial production data (also due Monday) is likely to show a rebound though after a period of post sales tax related weakness.

In Australia, wages growth (Wednesday) is likely to have remained weak in the December quarter with a 0.5% quarter on quarter gain leaving wages growth stuck at just 2.2% year on year. Jobs data for January (Thursday) is likely to show a slowdown after the stronger than expected gain seen in December – we expect jobs growth of just 15,000 and the unemployment rate to rise back to 5.2%. Meanwhile, the minutes from the RBA’s last board meeting will likely show that it remains prepared to ease again if needed but for the February meeting was happy to remain on hold given the long and variable lags from last year’s easing, somewhat better economic data for the end of last year and given the costs of further easing.

The Australian December half earnings reporting season will see its busiest week ahead with around 100 major companies due to report including QBE and Brambles (Monday), BHP, Cochlear and Coles (Tuesday), Wesfarmers, Tabcorp, Fortescue and Crown (Wednesday) and Seven, Lendlease and Boral (Thursday). Earnings growth is expected to be running around 2-3% led by tech, telco, gaming, health care and consumer staple stocks, with resources earnings up around 3.5% but banks lagging with just 1% earnings growth. Key things to watch for are a fall in dividends and company comments around the bushfires and coronavirus.

Outlook for investment markets

Improving global growth and still easy monetary conditions should drive reasonable investment returns through 2020, providing the coronavirus is contained in the next month or so. But returns are likely to be more modest than the double-digit gains of 2019 as the starting point of higher valuations for shares and geopolitical risks are likely to constrain gains and create some volatility:

- Shares are at risk of a further short-term volatility, particularly with uncertainty around the coronavirus remaining high both in terms of the outbreak’s duration and its economic impact even if it’s soon contained.

- But for the year as a whole global shares are expected to see total returns around 9.5% helped by better growth and easy monetary policy.

- Cyclical, non-US and emerging market shares are likely to outperform, particularly if the US dollar declines and trade threat recedes as we expect.

- Australian shares are likely to do okay this year but with total returns also constrained to around 9% given sub-par economic & profit growth.

- Low starting point yields and a slight rise in yields through the year are likely to result in low returns from bonds.

- Unlisted commercial property and infrastructure are likely to continue benefitting from the search for yield but the decline in retail property values will still weigh on property returns.

- National capital city house prices are expected to see continued strong gains in the months ahead on the back of pent up demand, rate cuts and the fear of missing out. However, poor affordability, the weak economy and still tight lending standards are expected to see the pace of gains slow leaving property prices up 10% for the year as a whole. The coronavirus outbreak could be a bit of a short-term dampener though, particularly in terms of keeping Chinese buyers away.

- Cash & bank deposits are likely to provide very poor returns, with the RBA expected to cut the cash rate to 0.25%.

- The $A is likely to fall to around $US0.65 as the RBA eases further but then drift up a bit as global growth improves to end 2020 little changed.

By Shane Oliver