Weekly market update – week ending 7 February, 2020

Investment markets and key developments over the past week

Global share markets rebounded over the last week on optimism the coronavirus outbreak will be contained and helped by solid earnings results. Australian shares benefitted initially from the global rebound but gains were reversed reflecting the greater exposure to China of the Australian economy and as the RBA appeared to be more hawkish on interest rates. Chinese shares fell but this was after being closed for more than a week due to the Lunar New Year holiday. Reflecting the rebound in share markets, bond yields rose as did metal prices and the Australian dollar. But oil and iron ore prices fell.

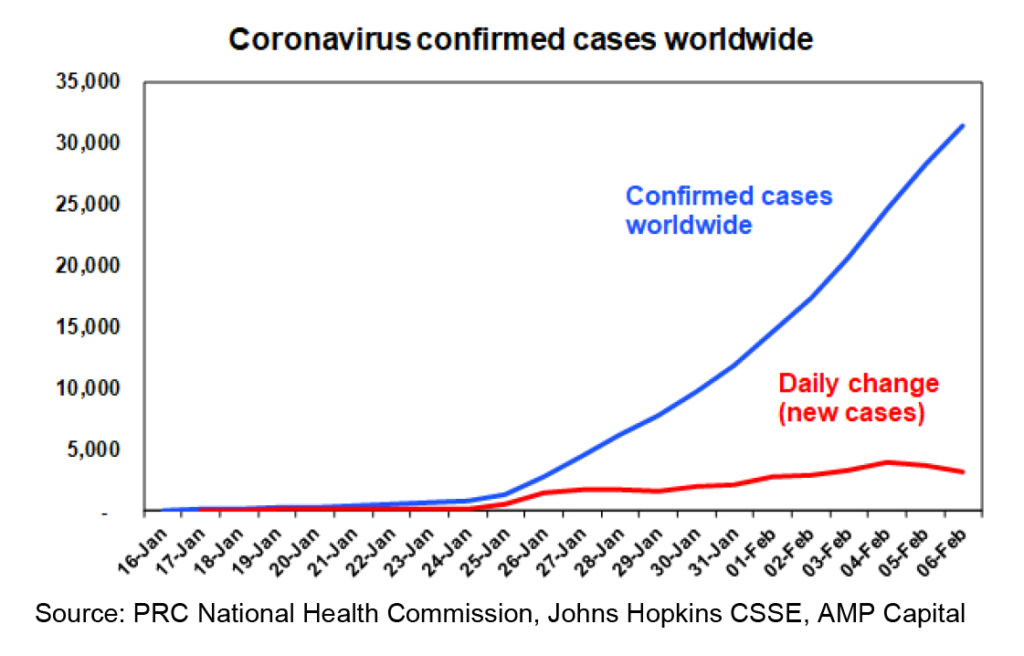

The number of coronavirus cases continued to ramp up over the last week, but there are some reasons for optimism that the outbreak will be contained within the next month or so. We looked at the issue and various scenarios around it here, but here are the key negatives and “positives”. First the negatives:

- The daily number of new cases is still trending up, although it has fallen in the last two days.

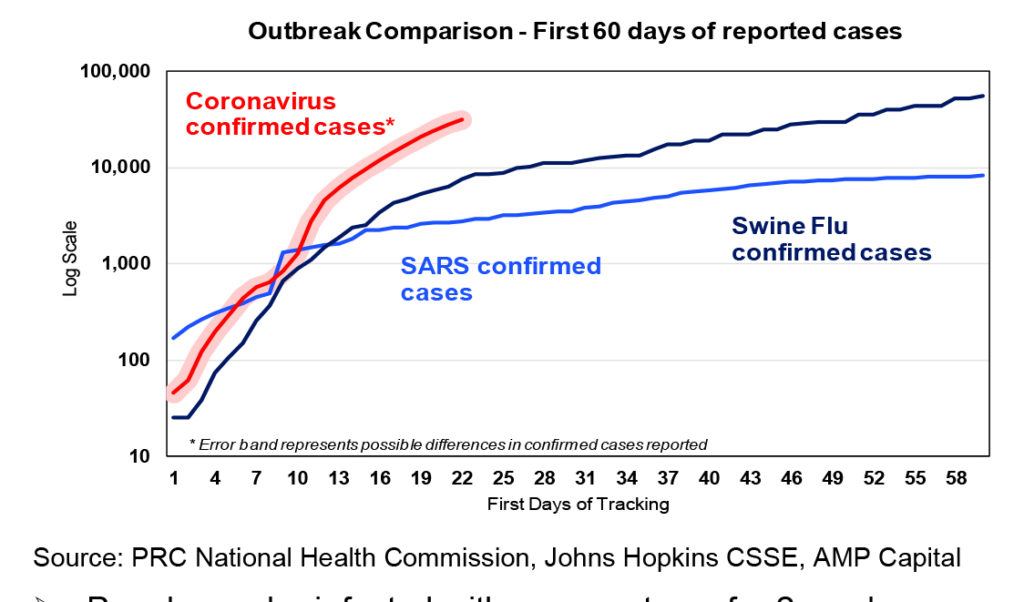

- There are more cases than with SARS and its rising faster.

- People can be infected with no symptoms for 2 weeks or so, making contagion easier.

But the following are also significant:

- It remains mainly confined to China with 99% of reported cases and 66% are in Hubei.

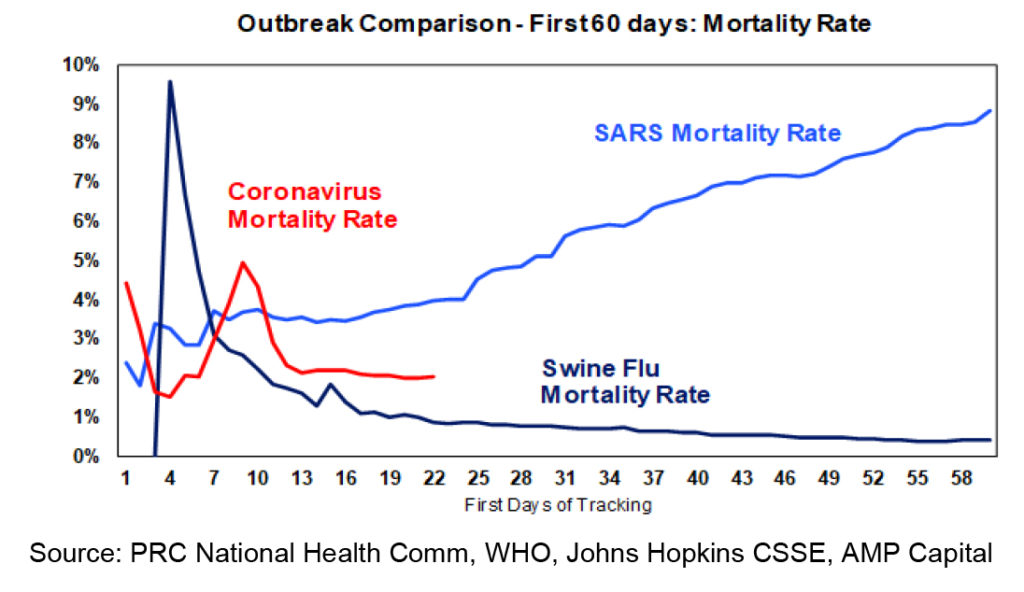

- The death rate is 2% & closer to swine flu than SARS, with 88% of those dying over 60 & 70% with prior conditions.

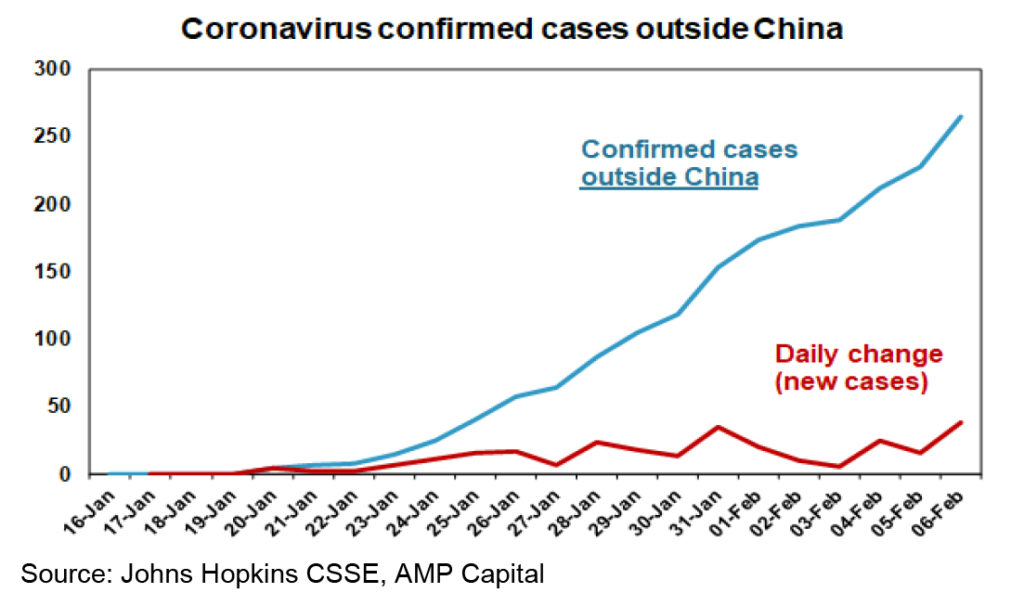

- New cases outside China look more contained.

Taken together this provides some confidence that the coronavirus outbreak will be contained within a month or so. However, it will still have a severe impact on growth in the current quarter as people stay at home in China and travel stops even if for a few weeks. We are assuming a 2-3% hit to March quarter GDP growth in China but it could be worse than this. The Australian economy is likely to at least see a 0.2-0.3% of GDP hit from reduced tourist, education & resources earnings which taken together with the bushfire impact of around 0.3% will likely see GDP contract this quarter. If the virus is contained relatively quickly then growth should start to recover from the June quarter. Two big uncertainties at present are around the reliability of the coronavirus case number data and whether there will be a mutation making it more virulent. And the spread of cases on a cruise ship off Japan will only reinforce people’s desire to stay at home.

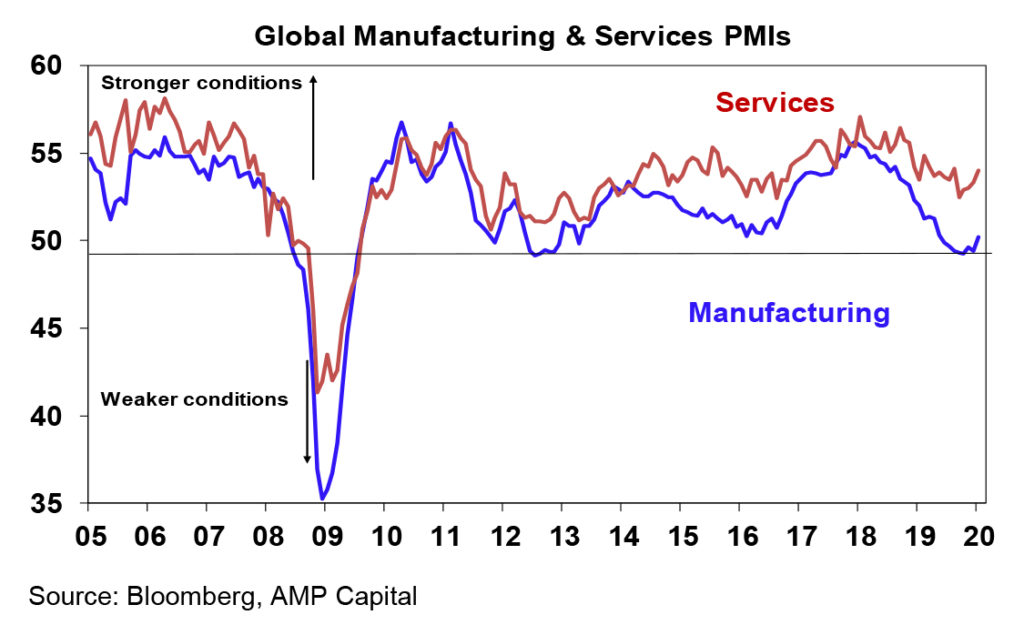

Global economy on the mend – at least before the coronavirus outbreak. This is evident in a further lift in business conditions PMIs for January. So assuming the coronavirus outbreak is contained relatively quickly, global growth should pick up this year after a short term disruption.

On other matters global: President Trump’s acquittal from impeachment was no surprise to anyone; moderate Democrat presidential candidate Pete Buttigieg’s strong showing in the stuffed up Iowa caucus is probably a bit of a relief for markets given the anxiety tax and spend socialist Bernie Sanders may cause; China’s move to halve tariffs on $US75bn of imports from the US is a positive goodwill move further lessening trade war risks for this year.

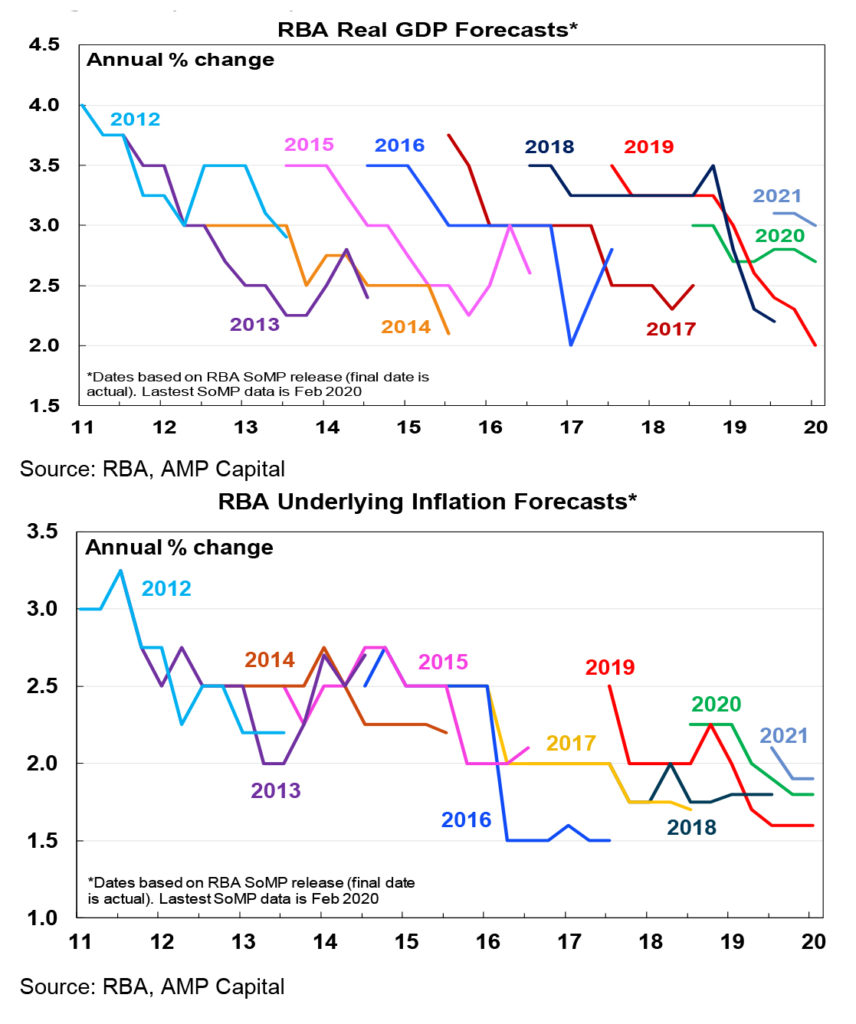

RBA upbeat and more hawkish. After better than expected jobs data for December and as expected inflation for the December quarter it wasn’t surprising to see the RBA leave rates on hold following its February board meeting. What was surprising though was its relative optimism in continuing to expect growth to rebound to 2.75% this year and its perceived higher hurdle to cutting interest rates further.

- While the bushfires and coronavirus mainly pose a short term threat to growth a full recovery will likely take longer than the RBA is assuming and they come at a time when confidence was already fragile. So we continue to see growth through this year as being closer to 2% as opposed to the RBA’s 2.75%.

- The RBA’s hurdle to cutting rates now looks to be “if the unemployment rate were to be moving materially in the wrong direction [ie up] and there was no further progress being made towards the inflation target”. But what about the huge pool of underemployed and the RBA’s own estimate that NAIRU or full employment is now around 4.5% which is well below the current level of 5.1%? And we haven’t been making progress towards the inflation target for years now.

In our view, with growth likely to be weaker than the RBA expects, unemployment is likely to drift up a bit, underemployment is likely to remain very high and wages growth and inflation are likely to remain lower for longer. All of which will result in little progress towards the RBA’s full employment or inflation goals. In fact, the RBA’s latest forecasts imply little such progress anyway. And Governor Lowe’s comment in his Parliamentary testimony that “we would have to have interest rates 3 or 4 percentage points lower than we are now” to get inflation back to target over the next two years further questions whether the RBA’s inflation objective will be achieved at all, because the longer we stay below target the more sub-target inflation will become entrenched. So something will have to give. Either the RBA relaxes it goals which will weaken their credibility, the Government will have to provide more fiscal stimulus which would be the optimal outcome but is not assured at present or the RBA will have to undertake more monetary easing. The latter would entail taking the cash rate to the RBA’s suggested floor of 0.25% and then doing quantitative easing. So, we continue to see further rate cuts in the months ahead with a high chance that quantitative easing will be required, despite Governor Lowe saying that “it is not on our agenda at the moment.”

Out of interest, RBA growth and inflation forecasts (along with consensus forecasts) have proved chronically too optimistic over the last decade now. The pattern has been: forecast better growth and higher inflation in the year ahead, only to push it out into the next year when it doesn’t eventuate. For global forecasters its been a similar pattern. One day we will get an upside surprise, but for now its still hard to see.

Major global economic events and implications

US economic data was mostly good. Construction data was a bit weaker than expected and the trade deficit rose, the ISM manufacturing conditions index rebounded into positive territory in January, the non-manufacturing ISM conditions index rose and remains solid and jobs data was strong.

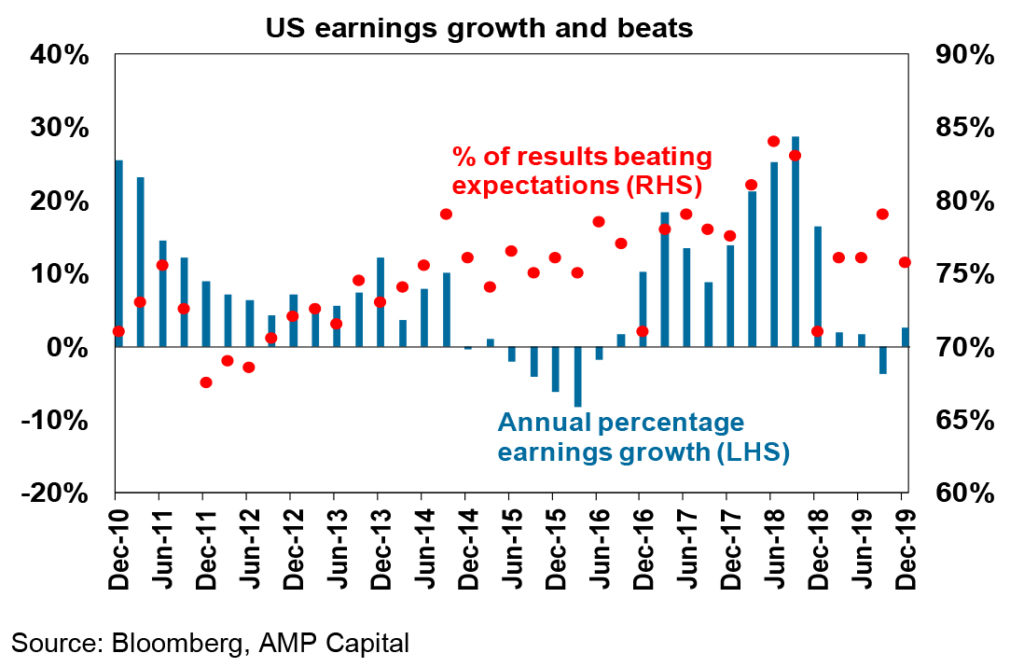

US earnings results have generally been good. 63% of US S&P 500 companies have reported so far with 76% beating on earnings (which is just above the long term average) by an average of 5% and 66% beating on sales. Earnings growth looks like its up about 2.5% year on year, compared to market expectations a few weeks ago for a 2% decline. Market expectations for 10% earnings growth this year look a bit too high but its likely to be around 5-7% which is still reasonable.

Eurozone business conditions PMIs were revised up in January and are continuing to recover from last year’s lows.

China’s Caixin business conditions PMIs fell in January, possibly reflecting coronavirus impacts but they remain up on last year’s lows. China’s central bank announced a further policy easing to help offset the negative impact of the coronavirus outbreak on the economy.

Australian economic events and implications

The run of Australian economic data was on the positive side over the last week with house prices up solidly again in January, building approvals fell just 0.2% in December but this followed an 11% gain in November and they are up slightly on a year ago, job ads rose in January and the trade surplus remained high in December. Against this the AIG’s services and manufacturing PMIs fell further in January and retail sales fell in December after Black Friday sales pulled forward spending.

For the December quarter, trade and a 0.5% rise in real retail sales look like supporting GDP growth. However, the March quarter is likely to see the economy go backwards with trade likely to detract from growth as the coronavirus outbreak hits tourist, resources and education export earnings and as the bushfires impact retail sales and economic activity generally.

House prices are expected to continue to rise this year helped by strong underlying demand, a lack of supply and low interest rates taking Sydney and Melbourne prices to new record highs in the months ahead. However, monthly gains are expected to slow from the rapid pace seen through the second half of last year as the soft economy impacts, pent up demand is exhausted, and APRA possibly tightens lending standards again. Average prices are expected to rise by around 10% this year with gains broadening beyond Sydney and Melbourne. An uncertainty though is the extent to which the coronavirus impacts Chinese property demand.

What to watch over the next week?

News on coronavirus will likely continue to dominate over the week ahead as markets attempt to assess whether it is being contained or not and its impact on global growth.

In the US, expect to see January core CPI inflation (Wednesday) remain around 2.3% year on year and January retail sales growth (Friday) to remain solid at around 0.3% month on month. Data on small business optimism, job openings and industrial production will also be released and December quarter earnings results will continue to flow.

Chinese data for January is expected to show CPI inflation (Monday) rising to around 5% but core inflation remaining weak around 1.5% and growth in money supply and credit remaining strong.

In Australia, expect a further rise in housing finance commitments for December (Tuesday) but the NAB business survey for January (also Tuesday) is likely to show some deterioration in conditions and confidence reflecting the bushfires and coronavirus fears. RBA Governor Lowe will participate in a panel discussion on Thursday but its hard to see how he could say much that is new after the RBA commentary overload seen over the past week.

The Australian December half earnings reporting season will ramp up with 46 major companies due to report including JB HiFi and GPT (Monday), Suncorp and Transurban (Tuesday), CSL and CBA (Wednesday) and Telstra, IAG, AMP and Woodside (Thursday). Earnings growth is expected to be running around 2-3% led by tech, telco, gaming, health care and consumer staple stocks, with resources earnings up around 3.5% but banks lagging with just 1% earnings growth. Key themes are expected to be a fall in dividends and company comments around the bushfires and coronavirus.

Outlook for investment markets

Improving global growth and still easy monetary conditions should drive reasonable investment returns through 2020, providing the coronavirus is soon contained. But returns are likely to be more modest than the double-digit gains of 2019 as the starting point of higher valuations for shares and geopolitical risks are likely to constrain gains and create some volatility:

- Shares are still at risk of a short-term correction or consolidation, particularly with uncertainty around the coronavirus remaining high.

- But for the year as a whole global shares are expected to see total returns around 9.5% helped by better growth and easy monetary policy.

- Cyclical, non-US and emerging market shares are likely to outperform, particularly if the US dollar declines and trade threat recedes as we expect.

- Australian shares are likely to do okay this year but with total returns also constrained to around 9% given sub-par economic & profit growth.

- Low starting point yields and a slight rise in yields through the year are likely to result in low returns from bonds.

- Unlisted commercial property and infrastructure are likely to continue benefitting from the search for yield but the decline in retail property values will still weigh on property returns.

- National capital city house prices are expected to see continued strong gains into early 2020 on the back of pent up demand, rate cuts and the fear of missing out. However, poor affordability, the weak economy and still tight lending standards are expected to see the pace of gains slow leaving property prices up 10% for the year as a whole.

- Cash & bank deposits are likely to provide very poor returns, with the RBA expected to cut the cash rate to 0.25%.

- The $A is likely to fall to around $US0.65 as the RBA eases further but then drift up a bit as global growth improves to end 2020 little changed.

By Shane Oliver